| Table 1 | |||||||||

| Macroeconomic Projection 2019:04 - 2026:04 (Stochastic Mean) | |||||||||

| Real Annual Growth Rates for each Quarter (2012 Chained Rates) | |||||||||

| Year | GDP | Y = CN + I + G | CN = Consumption | I = Investment | X = Exports | M = Imports | r = Interest Rate | Money | G = Government |

|---|---|---|---|---|---|---|---|---|---|

| 2019 | 0.41% | 0.21% | 0.59% | -2.31% | 1.55% | 0.15% | 2.66 | 1.89% | 2.22% |

| 2020 | -0.47% | -0.21% | 0.19% | -2.69% | -1.08% | 0.45% | 2.74 | 2.00% | 1.50% |

| 2021 | 0.03% | 0.09% | 0.12% | -1.02% | -0.53% | 0.05% | 2.83 | 2.00% | 1.50% |

| 2022 | 1.18% | 1.07% | 0.68% | 2.12% | 2.55% | 1.53% | 2.33 | 2.00% | 1.50% |

| 2023 | 2.06% | 2.09% | 1.43% | 4.76% | 2.07% | 2.42% | 1.93 | 2.00% | 1.50% |

| 2024 | 2.26% | 2.51% | 2.06% | 4.71% | 2.23% | 3.68% | 1.61 | 2.00% | 1.50% |

| 2025 | 2.26% | 2.46% | 2.34% | 3.50% | 2.35% | 3.50% | 1.38 | 2.00% | 1.50% |

| 2026 | 2.09% | 2.19% | 2.28% | 2.34% | 2.39% | 2.84% | 1.07 | 2.00% | 1.50% |

| 2027 | 1.85% | 1.90% | 2.08% | 1.59% | 2.19% | 2.58% | 0.80 | 2.00% | 1.50% |

| 2028 | 1.74% | 1.68% | 1.90% | 1.11% | 2.62% | 2.12% | 0.46 | 2.00% | 1.50% |

| 2029 | 1.63% | 1.71% | 1.82% | 1.49% | 2.13% | 2.41% | 0.23 | 2.00% | 1.50% |

| Notes: | |||||||||

| GDP is the sum of gross value added by all resident producers in the economy plus any product taxes and minus any subsidies not included in the value of the products. It is calculated without making deductions for depreciation of fabricated assets or for depletion and degradation of natural resources. Data are in constant local currency. | |||||||||

| Y = Absorption is the sum of Consumption, Investment and Government Expenditures. | |||||||||

| CN = Household final consumption expenditure (formerly private consumption) is the market value of all goods and services, including durable products (such as cars, washing machines, and home computers), purchased by households. It excludes purchases of dwellings but includes imputed rent for owner-occupied dwellings. It also includes payments and fees to governments to obtain permits and licenses. Here, household consumption expenditure includes the expenditures of nonprofit institutions serving households, even when reported separately by the country. Data are in constant local currency. | |||||||||

| I = Gross capital formation (formerly gross domestic investment) consists of outlays on additions to the fixed assets of the economy plus net changes in the level of inventories. Fixed assets include land improvements (fences, ditches, drains, and so on); plant, machinery, and equipment purchases; and the construction of roads,railways, and the like, including schools, offices, hospitals, private residential dwellings, and commercial and industrial buildings. Inventories are stocks of goods held by firms to meet temporary or unexpected fluctuations in production or sales, and work in progress; According to the 1993 SNA, net acquisitions of valuables are also considered capital formation. Data are in constant local currency. | |||||||||

| r = Lending rate is the bank rate that usually meets the short- and medium-term financing needs of the private sector. This rate is normally differentiated according to creditworthiness of borrowers and objectives of financing. The terms and conditions attached to these rates differ by country, however, limiting their comparability. | |||||||||

| X = Exports as a capacity to import equals the current price value of exports of goods and services deflated by the import price index. Data are in constant local currency. | |||||||||

| M = Imports of goods and services represent the value of all goods and other market services received from the rest of the world. They include the value of merchandise, freight, insurance, transport, travel, royalties, license fees, and other services, such as communication, construction, financial, information, business, personal, and government services. They exclude compensation of employees and investment income (formerly called factor services) | |||||||||

| Money = Broad money (IFS line 35L..ZK) is the sum of currency outside banks; demand deposits other than those of the central government; the time, savings, and foreign currency deposits of resident sectors other than the central government; bank and travelers checks; and other securities such as certificates of deposit and commercial paper. | |||||||||

| G = General government final consumption expenditure (formerly general government consumption) includes all government current expenditures for purchases of goods and services (including compensation of employees). It also includes most expenditures on national defense and security, but excludes government military expenditures that are part of government capital formation. Data are in constant local currency. | |||||||||

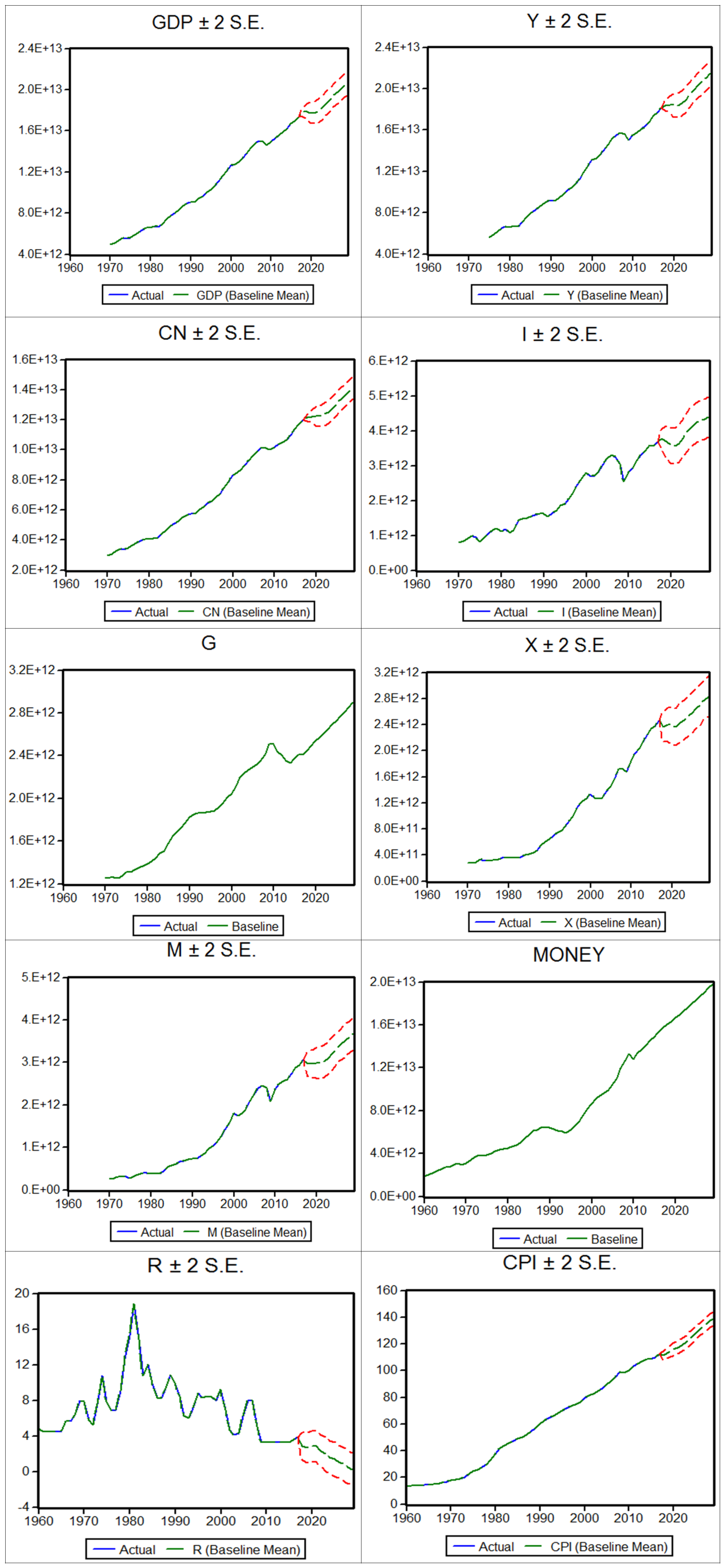

Annual Macroeconomic Forecast 2019 - 2029

January 1, 2020

The results of the quarterly model powered with data from the Bureau of Economic Analysis (www.bea.org) and the Federal Reserve Board (www.federalreserve.gov) are to a great extent confirmed by an annual simultaneous equation model using historical data from the World Bank (www.worldbank.org) which differs from the quarterly model on the interest rate, monetary aggregates and base year used. While in the quarterly model the monetary aggregate was M1 this model uses the broad money supply, the interest rate is not the federal funds rate but the commercial lending rate and the base year used to adjust the data to constant dollars is 2010 instead of 2012. There is even a more important caveat regarding the data. The data obtained from the World Bank as of today has been updated until 2018 since it is annual and in some cases only until 2017. Thus the quarterly model probably provides a better sense of the actual current situation since it has historical data through the third quarter of 2019.

Nonetheless it still gives a good sense of where the economy is going, given the historical data and the model equations. It also suggests the possibility of a GDP contraction starting in 2020 and continuing through 2021. The policy parameters are similar to the ones used in the quarterly model although not strictly comparable since the money supply variable is different. However, it is assumed that that the broad money supply will grow at a real rate of 2% per year between 2020 and 2029. In the case of government expenditures the assumption is also kept at a growth rate of 1.5% per year.

The Gross Domestic Product contraction suggested by the model would be mild. In effect, the economy would have been cooled without a severe trauma.

{kind=link}