| Table 1 | |||||||||

| Macroeconomic Projection 2019 2029 (Stochastic Mean) | |||||||||

| Real Annual Growth Rates (2010 Constant Dollars) | |||||||||

| Quarter | GDP | Y | r | NX | C | I | M1 | G | |

|---|---|---|---|---|---|---|---|---|---|

| 2019-04 | 1.86% | 1.68% | 1.71 | -5.45% | 2.44% | -2.13% | 3.34% | 2.69% | |

| 2020-01 | 0.74% | 0.77% | 1.67 | -1.97% | 2.34% | -6.60% | 3.80% | 2.34% | |

| 2020-02 | 0.27% | -0.04% | 1.56 | -9.45% | 1.34% | -6.87% | 3.66% | 1.53% | |

| 2020-03 | -0.33% | -0.81% | 1.66 | -13.16% | 0.69% | -8.91% | 3.00% | 1.50% | |

| 2020-04 | -0.62% | -1.04% | 1.63 | -9.33% | 0.41% | -9.32% | 3.00% | 1.50% | |

| 2021-01 | -0.61% | -1.09% | 1.66 | -10.97% | 0.15% | -8.85% | 3.12% | 1.50% | |

| 2021-02 | -0.60% | -1.04% | 1.61 | -9.74% | -0.03% | -8.00% | 3.25% | 1.50% | |

| 2021-03 | -0.38% | -0.71% | 1.53 | -8.43% | -0.14% | -5.55% | 3.37% | 1.50% | |

| 2021-04 | 0.16% | -0.17% | 1.42 | -7.90% | -0.13% | -2.23% | 3.50% | 1.50% | |

| 2022-01 | 0.74% | 0.49% | 1.41 | -5.32% | -0.01% | 1.66% | 3.50% | 1.50% | |

| 2022-02 | 1.14% | 1.04% | 1.30 | -1.89% | 0.15% | 4.59% | 3.12% | 1.50% | |

| 2022-03 | 1.54% | 1.52% | 1.33 | 1.32% | 0.38% | 6.75% | 2.75% | 1.50% | |

| 2022-04 | 1.75% | 1.89% | 1.40 | 4.62% | 0.62% | 8.04% | 2.37% | 1.50% | |

| 2023-01 | 2.01% | 2.16% | 1.53 | 7.13% | 0.87% | 8.66% | 2.00% | 1.50% | |

| 2023-02 | 2.00% | 2.29% | 1.59 | 8.62% | 1.11% | 8.32% | 2.00% | 1.50% | |

| 2023-03 | 1.95% | 2.24% | 1.61 | 9.40% | 1.30% | 7.05% | 2.00% | 1.50% | |

| 2023-04 | 1.81% | 2.10% | 1.67 | 8.59% | 1.44% | 5.50% | 2.00% | 1.50% | |

| 2024-01 | 1.64% | 1.86% | 1.73 | 6.83% | 1.51% | 3.70% | 2.00% | 1.50% | |

| 2024-02 | 1.44% | 1.56% | 1.85 | 5.57% | 1.50% | 1.91% | 2.00% | 1.50% | |

| 2024-03 | 1.09% | 1.26% | 1.93 | 3.32% | 1.47% | 0.13% | 2.00% | 1.50% | |

| 2024-04 | 0.97% | 0.98% | 2.03 | 1.70% | 1.39% | -1.21% | 2.00% | 1.50% | |

| 2025-01 | 0.82% | 0.82% | 2.11 | 0.22% | 1.29% | -1.82% | 2.00% | 1.50% | |

| 2025-02 | 0.76% | 0.70% | 2.12 | -1.86% | 1.20% | -2.19% | 2.00% | 1.50% | |

| 2025-03 | 0.88% | 0.69% | 2.21 | -2.14% | 1.10% | -1.83% | 2.00% | 1.50% | |

| 2025-04 | 0.88% | 0.73% | 2.26 | -2.24% | 1.04% | -1.34% | 2.00% | 1.50% | |

| 2026-01 | 1.02% | 0.83% | 2.33 | -2.85% | 1.00% | -0.59% | 2.00% | 1.50% | |

| 2026-02 | 1.16% | 0.99% | 2.43 | -2.01% | 0.99% | 0.40% | 2.00% | 1.50% | |

| 2026-03 | 1.23% | 1.13% | 2.42 | -0.62% | 1.03% | 1.15% | 2.00% | 1.50% | |

| 2026-04 | 1.35% | 1.31% | 2.47 | 0.14% | 1.05% | 2.22% | 2.00% | 1.50% | |

| Notes: | |||||||||

| GDP = Gross domestic product; Y = Absorption = C + I + G; r = Federal Funds Rate; | |||||||||

| NX = Net exports of goods and services = Exports - Imports; π = Consumer price index base year 2012; | |||||||||

| C = Personal consumption expenditures; I = Gross private domestic investment; | |||||||||

| M1 = Money Supply = Currency + Demand Deposits + Other Checkable Deposits + Travelers Checks; | |||||||||

| G = Government consumption expenditures and gross investment | |||||||||

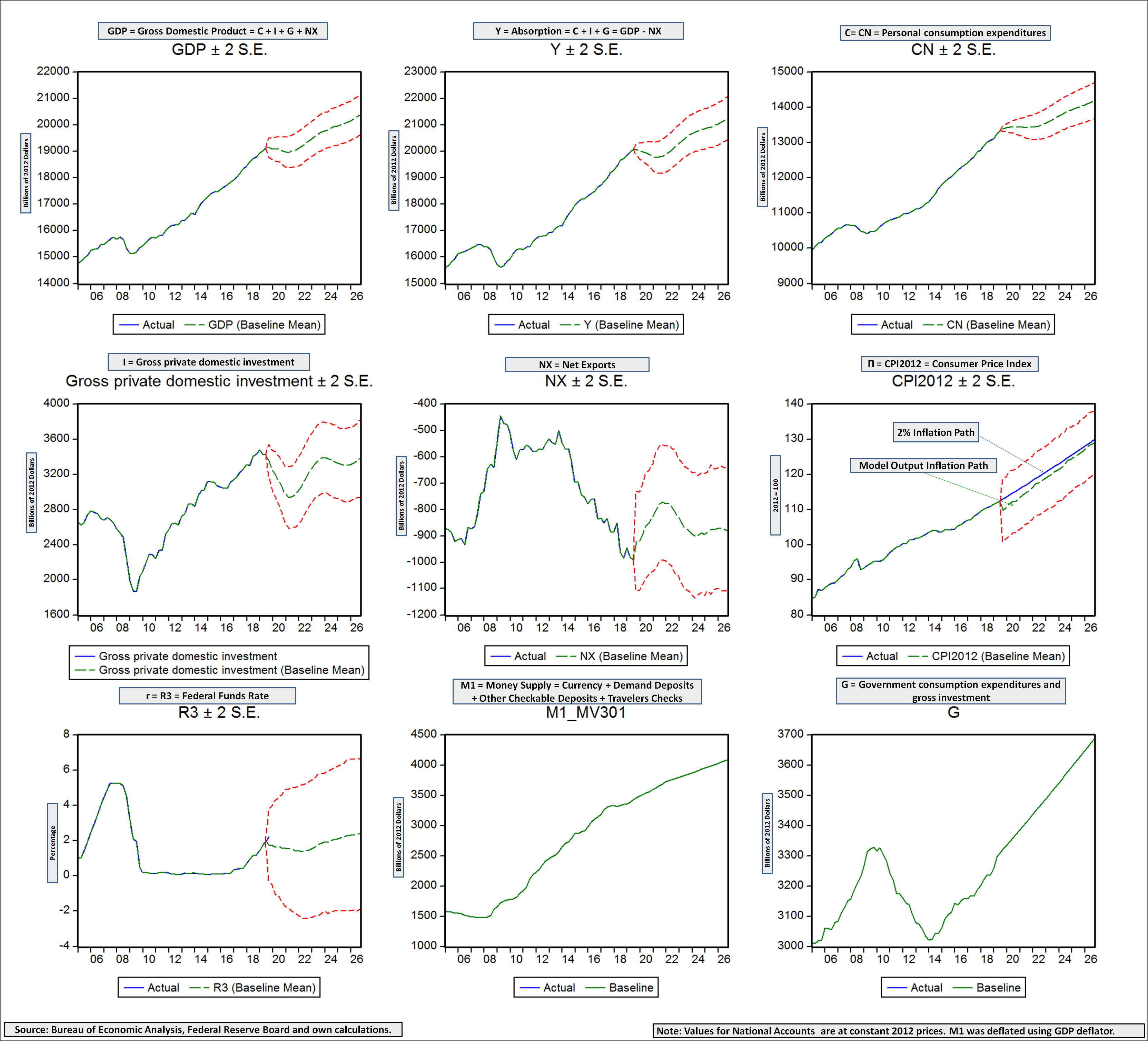

Quarterly Macroeconomic Forecast 2019-2026

December 24, 2019

Although the third quarter of 2019 economic data still does not show compelling evidence of a downturn a more thorough analysis suggests that the U.S. economy may be heading to a recession starting in 2020. It could prolong itself for more than one year. The fourth quarter of 2019 will probably already show the evidence of the slowdown. The rise in the federal funds rate will have delivered its effect on softening internal demand with a corresponding result on the consumer price index. Inflation on the fourth quarter of 2019 will have been controlled at the necessary cost of reduced economic growth which will be short and mild if things turn out fine.

The amount of public and private debt in the economy requires special prudence on any changes. The wrong measure might bring about havoc. This may possibly be a nice soft landing after a decade of intensive monetary stimuli or additional difficulties depending on the measures adopted.

The Federal Reserve implemented an expansionary monetary policy rendering an average annual increase in the real money supply (M1) of close to 9% between the first quarters of 2008 and 2018 that allowed the economy to survive. The M1 expansion diminished to an annual real rate of 2.2% between the third quarter of 2018 and the same quarter of 2019.

Additionally, an occasional Government shutdown may help in restricting inflationary pressure. However, there is a significant challenge concerning how to reestablish an adequate blend between fiscal and monetary policy. Fiscal policy has turned less valuable and useful due to the continuous shrinkage of the Federal Government as a component of the economy. A larger public sector could provide more flexibility when economic stimuli were considered desirable due to the availability of more and stronger fiscal tools.

The Federal Reserve definitely would be grateful to be able to count on someone else for economic policy. It is as good to share the credit during the good times as it is the blame during the bad times, like throughout the 2009-2008 financial crises.

With the FED continuing the adjustment process leading to a 3% expansion in M1 between the fourth quarter of 2019 and the same quarter of 2020 and Government consumption expenditures and gross investment growing at an annual rate of 1.5%, a simultaneous equation macroeconomic model solved stochastically on a 95% confidence interval (5% error level) suggests that a contraction of GDP will start in the third quarter of 2020. Keeping fiscal policy and allowing M1 to grow at an annual real rate of 3.5% between the first quarter of 2021 and the same quarter of 2022 then would allow the economy to start growing again on the third quarter of 2021. The recession would have lasted over a year and it would have not been overwhelming.

A future cautious monetary policy targeting an annual real growth in M1 of 2% without a change in fiscal policy would lead to a slow growing (around 2% per year) but stable economy, without significant inflationary pressures, other things being equal.

{kind=link}