| Table 1 | |||||||||

| Macroeconomic Projection 2020 2025 (Stochastic Mean) | |||||||||

| Annualized Quarterly Rates (2010 Constant Dollars) | |||||||||

| Percentages | |||||||||

| Quarter | GDP | Y | C | I | G | NX | FFR | M1 | |

|---|---|---|---|---|---|---|---|---|---|

| 2020-02 | 1.20 | 0.85 | 0.87 | -5.80 | 7.70 | 26.31 | 1.62 | 2.50 | |

| 2020-03 | 1.72 | 0.79 | 0.86 | -6.18 | 7.56 | 15.52 | 1.52 | 2.50 | |

| 2020-04 | 2.23 | 1.22 | 1.00 | -4.22 | 7.42 | 58.97 | 1.50 | 2.50 | |

| 2021-01 | 1.43 | 1.34 | 1.00 | -3.55 | 7.28 | 187.82 | 1.52 | 2.50 | |

| 2021-02 | 2.91 | 2.45 | 1.19 | -3.05 | 12.55 | 10.07 | 1.54 | 2.50 | |

| 2021-03 | 1.87 | 1.21 | 1.27 | -1.10 | 3.00 | 1.87 | 1.59 | 2.50 | |

| 2021-04 | 1.90 | 1.16 | 1.19 | -1.10 | 3.00 | 3.22 | 1.68 | 2.50 | |

| 2022-01 | 1.24 | 1.12 | 1.21 | -1.49 | 3.00 | 33.88 | 1.71 | 2.50 | |

| 2022-02 | 2.23 | 0.99 | 1.18 | -2.22 | 3.00 | 8.16 | 1.72 | 2.50 | |

| 2022-03 | 1.45 | 0.99 | 1.17 | -2.21 | 3.00 | -4.13 | 1.72 | 2.51 | |

| 2022-04 | 1.44 | 0.84 | 1.12 | -3.06 | 3.00 | 1.90 | 1.71 | 2.50 | |

| 2023-01 | 1.03 | 0.85 | 1.04 | -2.67 | 3.00 | 11.46 | 1.67 | 2.50 | |

| 2023-02 | 1.83 | 0.88 | 1.02 | -2.38 | 3.00 | 5.21 | 1.62 | 2.50 | |

| 2023-03 | 1.11 | 0.88 | 1.08 | -2.72 | 3.00 | 1.15 | 1.58 | 2.50 | |

| 2023-04 | 1.68 | 0.91 | 1.08 | -2.55 | 3.00 | -16.41 | 1.56 | 2.50 | |

| 2024-01 | 1.03 | 0.86 | 0.96 | -2.42 | 3.00 | 11.09 | 1.53 | 2.50 | |

| 2024-02 | 1.36 | 0.91 | 0.98 | -2.18 | 3.00 | 0.19 | 1.50 | 2.49 | |

| 2024-03 | 1.46 | 1.02 | 0.99 | -1.51 | 3.00 | -5.11 | 1.48 | 2.50 | |

| 2024-04 | 1.64 | 0.99 | 0.94 | -1.49 | 3.00 | 5.11 | 1.46 | 2.51 | |

| 2025-01 | 1.20 | 1.06 | 1.00 | -1.33 | 3.00 | -2.08 | 1.47 | 2.50 | |

| Notes: | |||||||||

| GDP = Gross domestic product; Y = Absorption = C + I + G; FFR = Federal Funds Rate; | |||||||||

| NX = Net exports of goods and services = Exports - Imports; π = Consumer price index base year 2012; | |||||||||

| C = Personal consumption expenditures; I = Gross private domestic investment; | |||||||||

| M1 = Money Supply = Currency + Demand Deposits + Other Checkable Deposits + Travelers Checks; | |||||||||

| G = Government consumption expenditures and gross investment | |||||||||

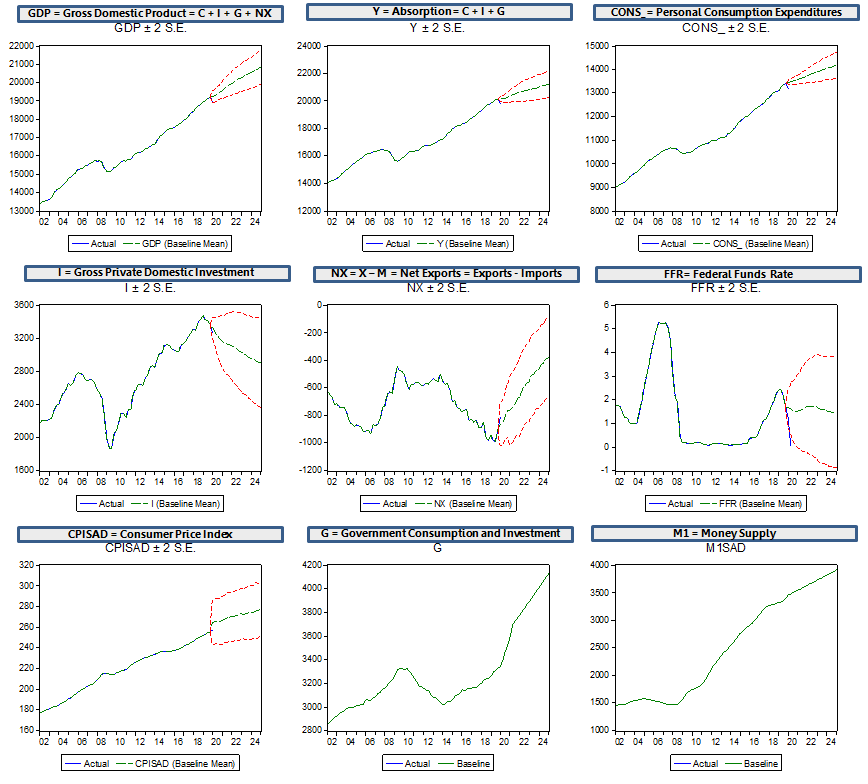

Quarterly Macroeconomic Forecast 2020:02-2025:01

The Impending Recession is Gone

June 3, 2020

In December of 2019 our Macroeconomic Model was used to forecast the next several quarters of the major macroeconomic (national) accounts. It was argued that there was a large probability that a downturn of GDP growth would be observed over several quarters starting on the third one of 2020.

What happened? First, COVID 19 rendered any previous forecast obsolete. The impact of the virus was severe on employment and on the economy in general, on the first quarter of 2020. Indeed, there was a contraction of GDP of 5% on an annual basis. In a sense the disease anticipated the economic woes foreseen at that time. Second, the response to the economic problems generated thereby was timely and adequate. The stimulus package swiftly approved and placed in motion has rendered its intended purpose. The large decreases in employment and personal income observed in the first quarter are now history or even pre-history, in other words they are gone.

Indeed, personal income increased 10.5% in April of 2020. Disposable income both in current and constant dollars showed even a bigger increase, 12.9% and 13.4% respectively when compared to March of 2020. Although personal consumption showed a decrease it is quite probable that in May there will be a large expansion when compared to April, thus avoiding the possibility of a recession. Our model shows that the economic policy response to COVID was at least sufficient.

Although, unemployment in April was high (14.7%) it is probable that May and/or June will show an important reduction as the stay at home measures recede or vanish. At this juncture workers are repossessing their jobs.

In our view many of the economic problems forecasted have been partially solved or postponed. There was a necessary economic adjustment realized in a matter of a quarter. The economy can resume its growth path. There was a lot of skepticism about the ability to implement fiscal policy in the short-term. Things have now changed and that doubt has now vanished.

Ironically, the economic measures propelled by the health crisis have generated economic confidence. In the face of major adversity a consensus can be generated to face it. And, in a short time things can change. Now the situation is completely the opposite. The problem no longer is that Monetary Policy had exhausted its effectiveness because interest rates had nowhere to go but into negative territory. Fiscal Policy has shown its power and now it is quite possible the Federal Reserve will be able to raise interest rates again in the near future to control the price level. There are many economic problems, perhaps more serious, remaining in the backdrop. However, this crisis has revealed that they might be solved if there were enough determination and conformity to do so.

Our quarterly model has been used again to forecast the next five years or twenty quarters. The model shows that a fiscal stimulus of $500 billion is more than enough to get the economy out of the COVID crisis. In the model the totality of the additional expenditures are injected into the economy between second quarter of 2020 and the first quarter of 2021. The assumption is that the "the rug will not be pulled under the stimulus" on the second quarter of 2021. Rather, it assumes that once the additional expenditure package finishes Government Expenditure will resume growing from that new higher level at a constant rate of 3.0% per year. If "the rug is pulled under the stimulus" and expenditures all of a sudden drop to the pre-COVID level a recession or worse is likely to occur.

In the short run the COVID crisis may have been solved and in the process brought an unexpected

positive economic policy externality. For the future, our model forecasts consistent GDP growth

with a reduction on private domestic investment. The additional Government expenditures contribute

to a reduction in private investment without a negative consequence for economic growth

over the five year period.

{kind=link}