Economic Trends -Latin America-

The fourth issue of Trends reviews

the financial and economic

developments that occurred in the

major Latin American economies

during 2009. Also, given that first

quarter of 2010 GDP data is not

yet available, it makes assertions

about the most probable outcomes

and formulates assertions for

the future. In the case of Colombia

there are detailed forecasts for

the next six years.

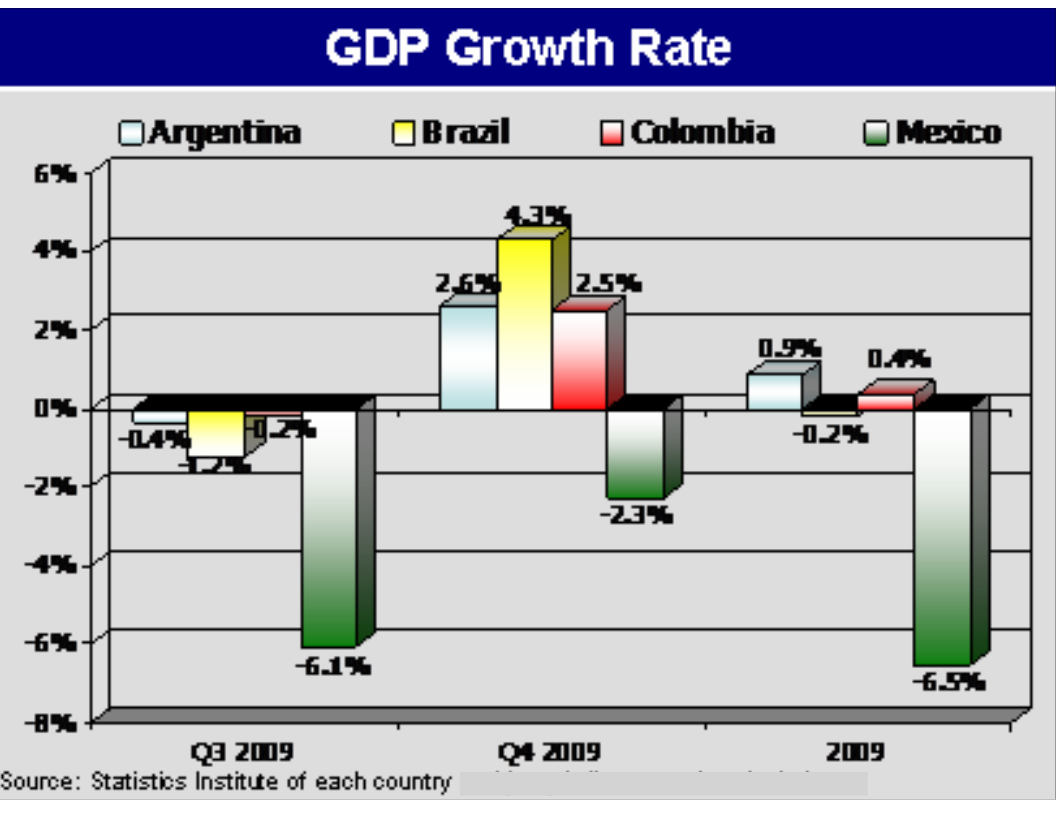

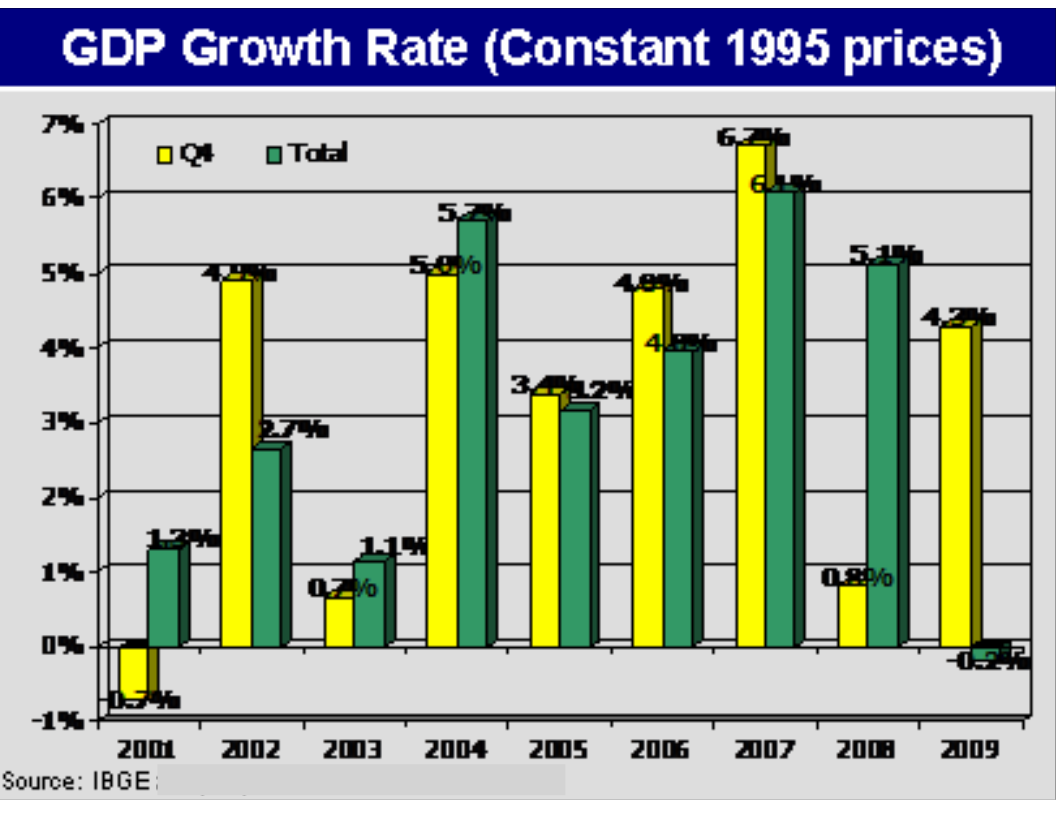

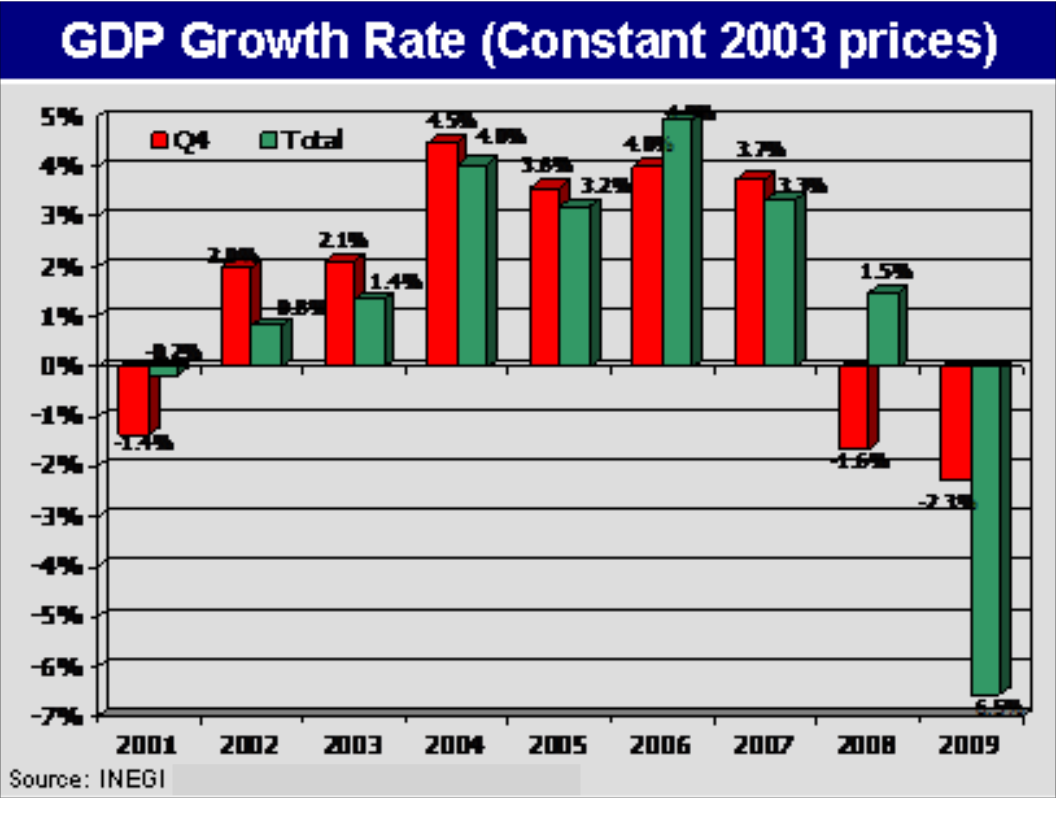

The GDP graph shows how Mexico was the regional economy

most affected by the crisis with a contraction of 6.5%

in real terms. At the end of 2009, Mexico had endured

five consecutive quarters of negative growth. On the

other hand, Brazil and Colombia had three quarters of

negative growth and Argentina two. However, it is highly

possible that first quarter of 2010 data shows Mexico

emerging from the recession thereby making it the last

large Latin American economy to do so. Thus, in the first

quarter of 2010 the four economies will show positive

real GDP growth leaving behind a painful and challenging

2008-2009 crisis.

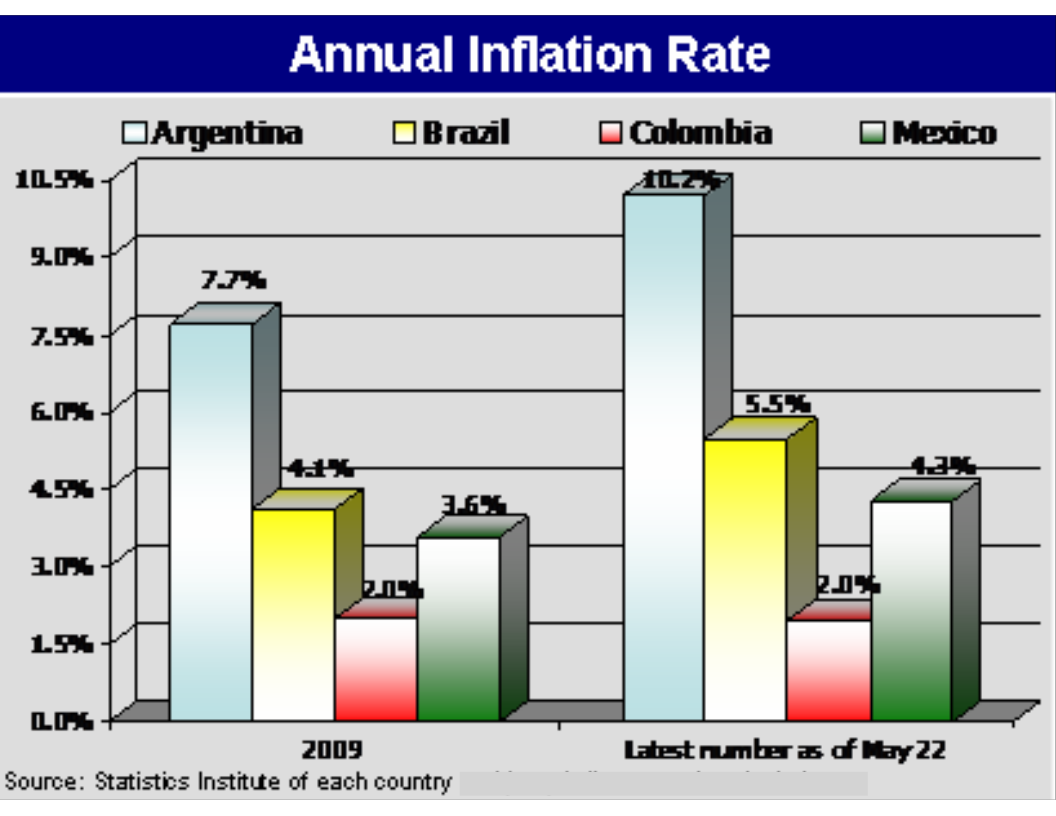

For these four economies 2010 will surely be better

than 2009. However, Argentina and Brazil face renewed

inflationary pressures that may hinder the economic

recovery while Colombia and Mexico seem to have suffered

the most during the crisis. Thus, the argument made in

2008 that these countries were somehow isolated from

the effects of the international crisis has been discredited

as well as the contention that they had somehow decoupled

from the U.S. economy.

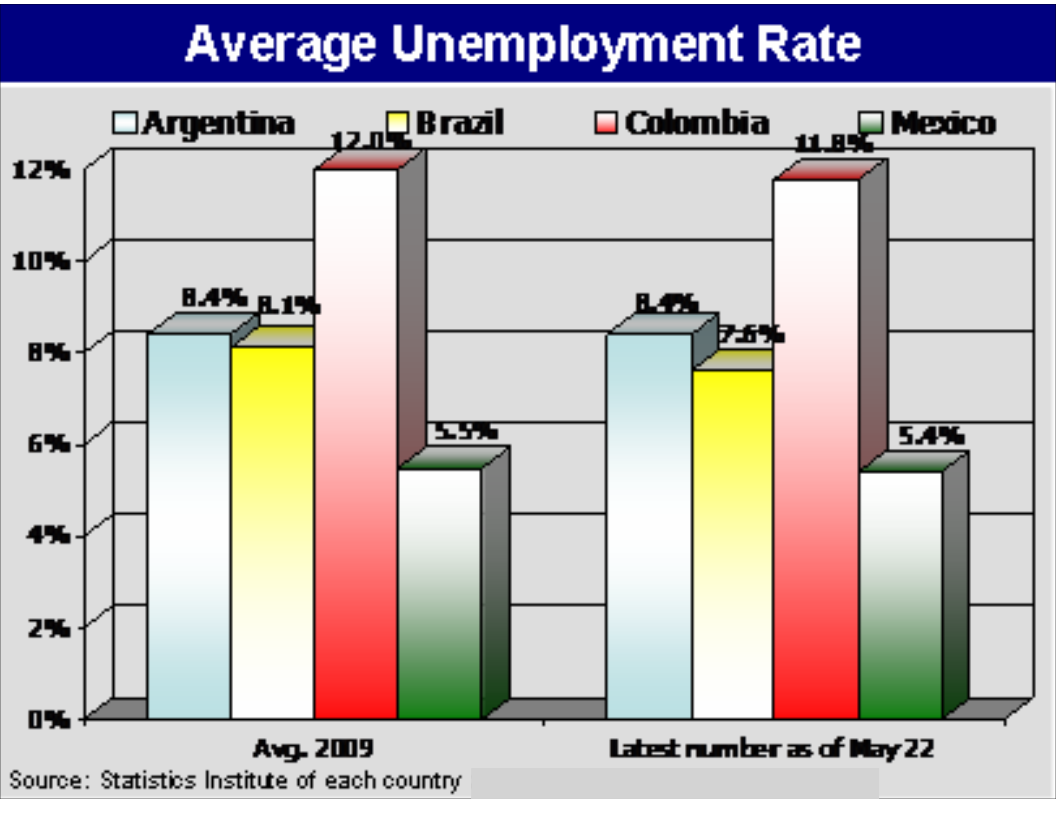

In 2010, despite a sizable increase in external debt,

the countries that seem better poised to take advantage

of the global recovery without increased inflation are

Colombia and Mexico given the severity of the recession

in the case of Mexico and the monetary adjustment endured

by Colombia. In both countries inflation so far is not

a major issue and while growth may not reach the levels

observed in 2007 in the case of Colombia, Mexico could

easily surpass it. Furthermore, with a prudent mix of

fiscal and monetary policy, 2011 could be even better

for both countries.

Argentina

There have been many unconventional moves

with respect to Central Bank management

including the destitution of its manager and

the use of reserves to partially finance a

government shortfall. Economic policy in

Argentina has also suffered by a lack of

confidence from financial markets as bond

yields have increased thereby delaying the

execution of debt swaps that could allow the

country to improve its debt profile and

international standing. At the same time,

the 2011 upcoming elections make it less

likely that government expenditures will

slow down in 2010 as the incumbent administration

seeks to perpetuate itself. Thus, although

Argentina avoided a significant recession

in 2009 the economic policy challenges

for 2010 loom even bigger.

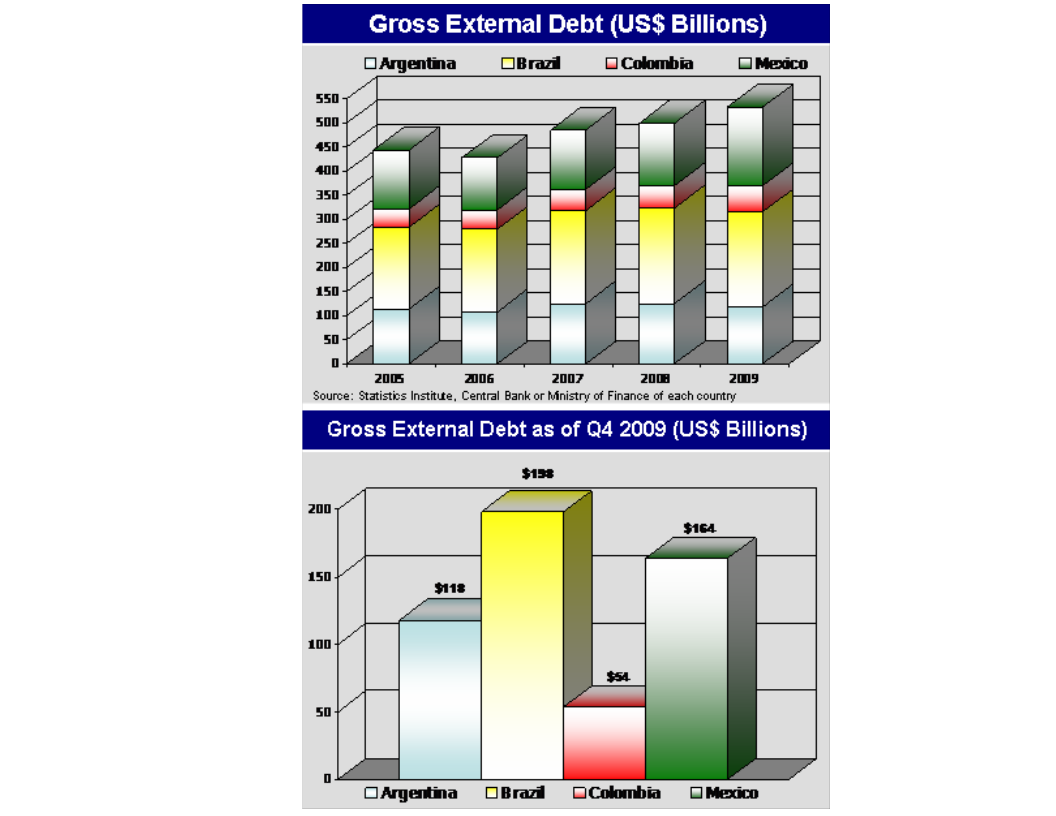

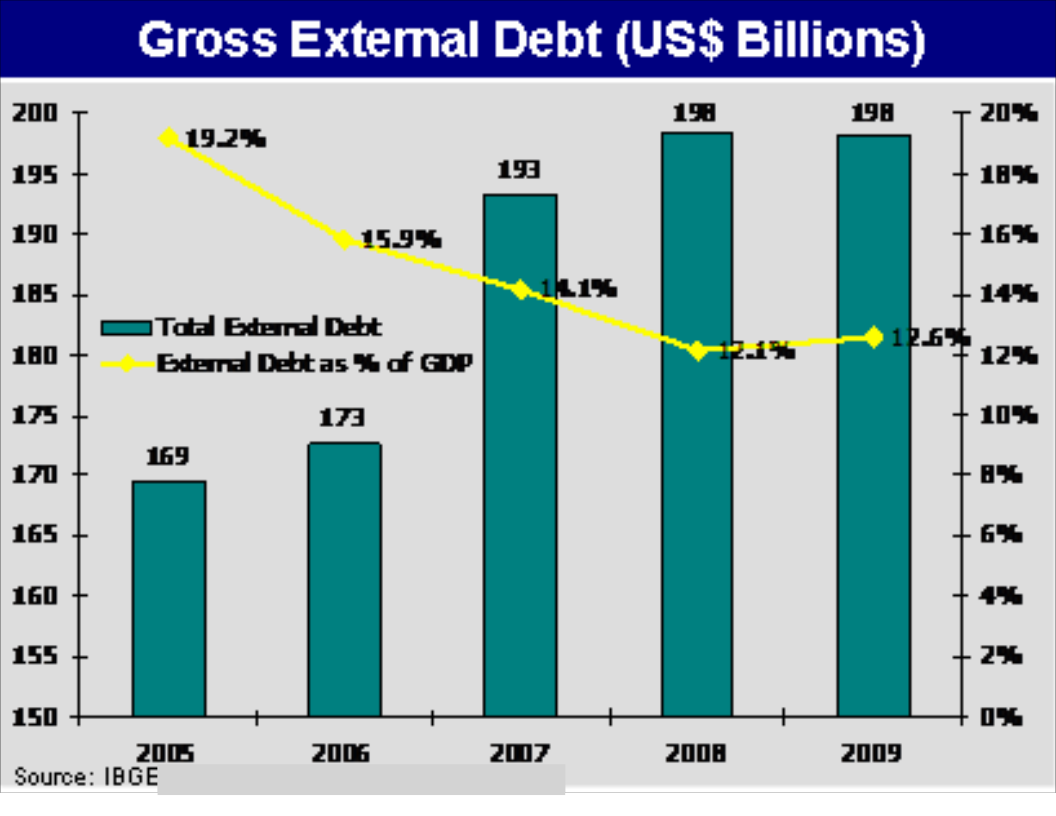

However, given the scope of the

European debt crisis it is important

to underline that Brazil's external

debt has fallen from being equivalent

to 19.2% of GDP in 2005 to only 12.5%

of GDP in 2009. Thus, the country has

ample room to maneuver on this respect

and rating agencies may be looking

favorably at this development.

-

Economic growth will be higher in 2010 and

the government will do everything to make

sure this happens given the upcoming elections.

-

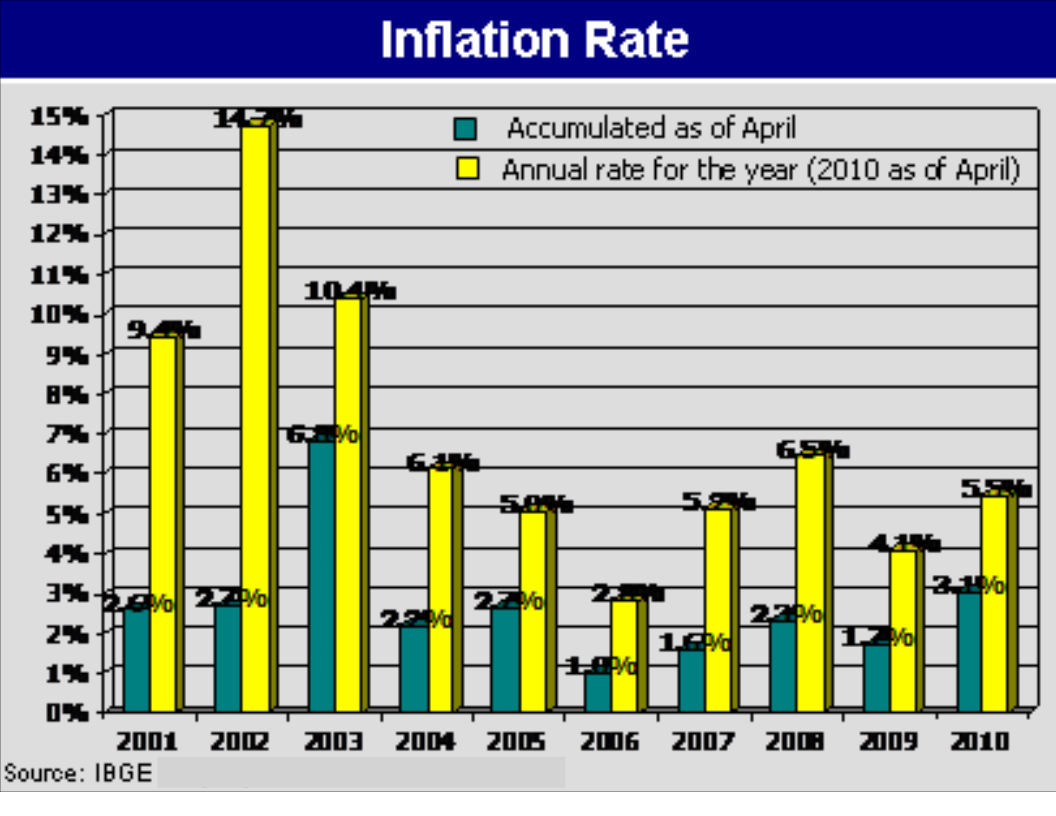

There is no doubt that inflation will increase

with respect to 2009, probably approaching the

2005 level of 12.3% and with the risk that

could come close to 30%

-

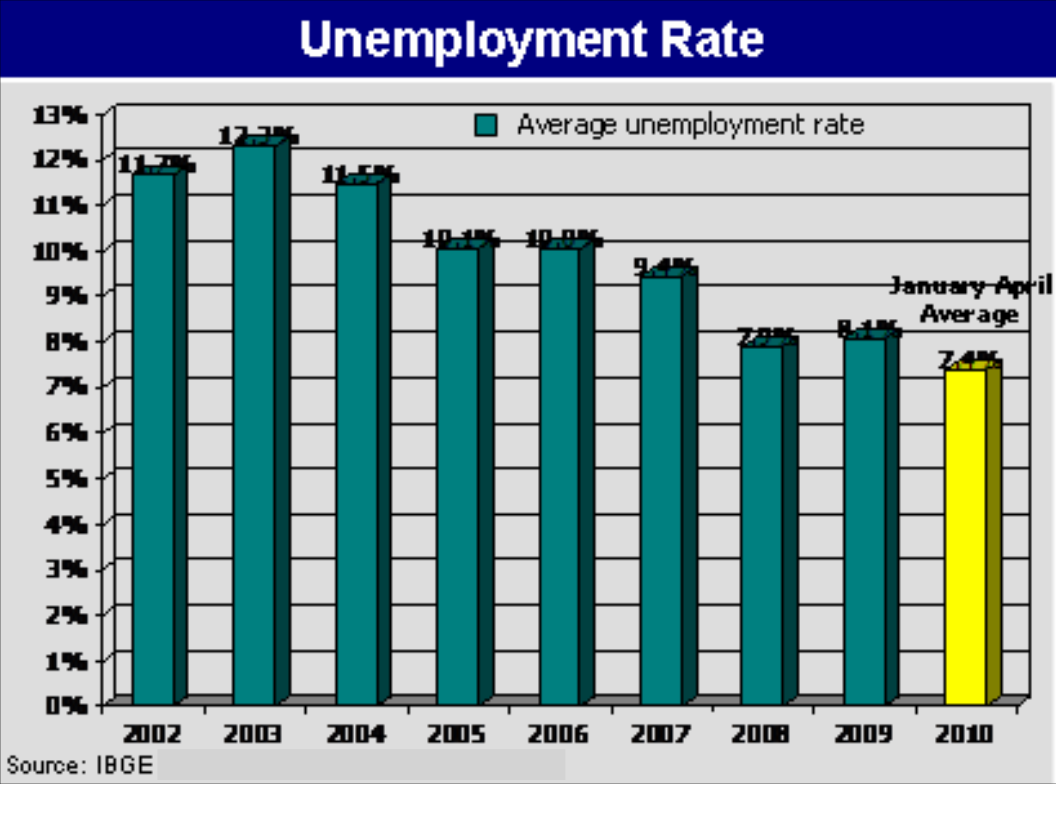

Given the recovery it is possible that the

unemployment rate stays around the 8% level.

-

At this point is yet uncertain whether

Argentina will be able to return to

the international capital markets by

executing a debt swap and placing a bond.

-

Argentina's economic management is

unorthodox and therefore introduces problems

in terms of current and future stability and credibility.

Brazil

At the same time imports and exports contracted

at similar rates implying that there was not

a significant adjustment in the current account

balance. However, there was a large contraction

of -9.9% in investment during the year. These

facts make Brazil a good candidate for a stable

and sustained recovery.

Given that the inflation target for the

year is 4.5% plus or minus 2 percentage

points the central bank may be forced

to increase interest rates further.

However, it is unlikely that inflation

becomes a major destabilizing factor

that could hinder the recovery.

Nonetheless, it is quite possible that

inflation for 2010 will be at the top

of the range of the central bank's target

of 6.5%. Despite possible additional interest

rate increases it is expected that economic

growth for 2010 will be around 5% which is

above the average for the decade.

The debt crisis in Greece may paradoxically

help Brazil. As investors take a more cautious

approach towards emerging markets inflationary

pressures may be somewhat relieved since

aggregate demand may increase less. In any case,

the country is likely to remain one the most

attractive emerging economies in the world.

However, given the scope of the European

debt crisis it is important to underline

that Brazil's external debt has fallen

from being equivalent to 19.2% of GDP

in 2005 to only 12.5% of GDP in 2009.

Thus, the country has ample room to

maneuver on this respect and rating

agencies may be looking favorably

at this development.

Overall it can be said that Brazil has managed

the crisis effectively without a significant

fall in GDP during 2009 while consumption,

household and government, increased at relatively

acceptable rates. While some inflationary pressures

are evident the commitment to a stable level of

prices and lower government expenditures will

ensure that the inflation rate stays under control. Thus:

-

GDP will likely grow at a real rate of 5%.

-

Inflation will probably be at the top of the 6.5% target and could even be higher.

-

The unemployment rate will fluctuate between 7% and 8%.

-

The main risks for Brazil at this point are inflation

and being so attractive that large capital flows

(long and short term) may be destabilizing.

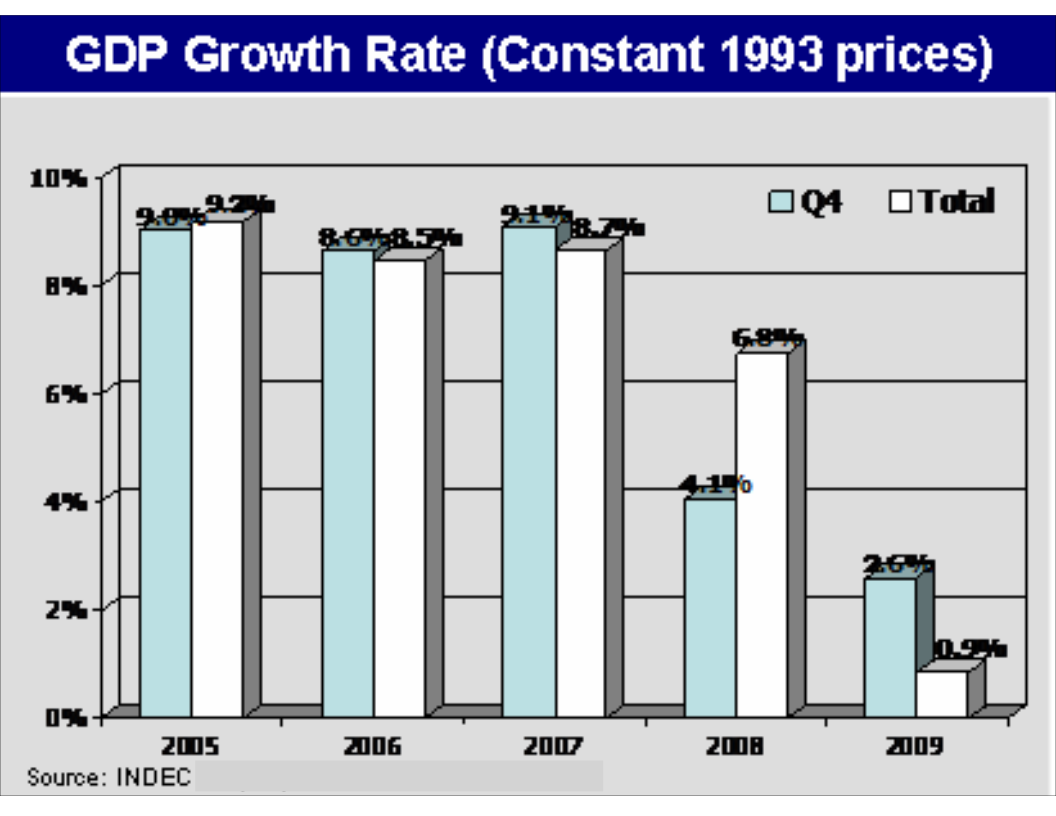

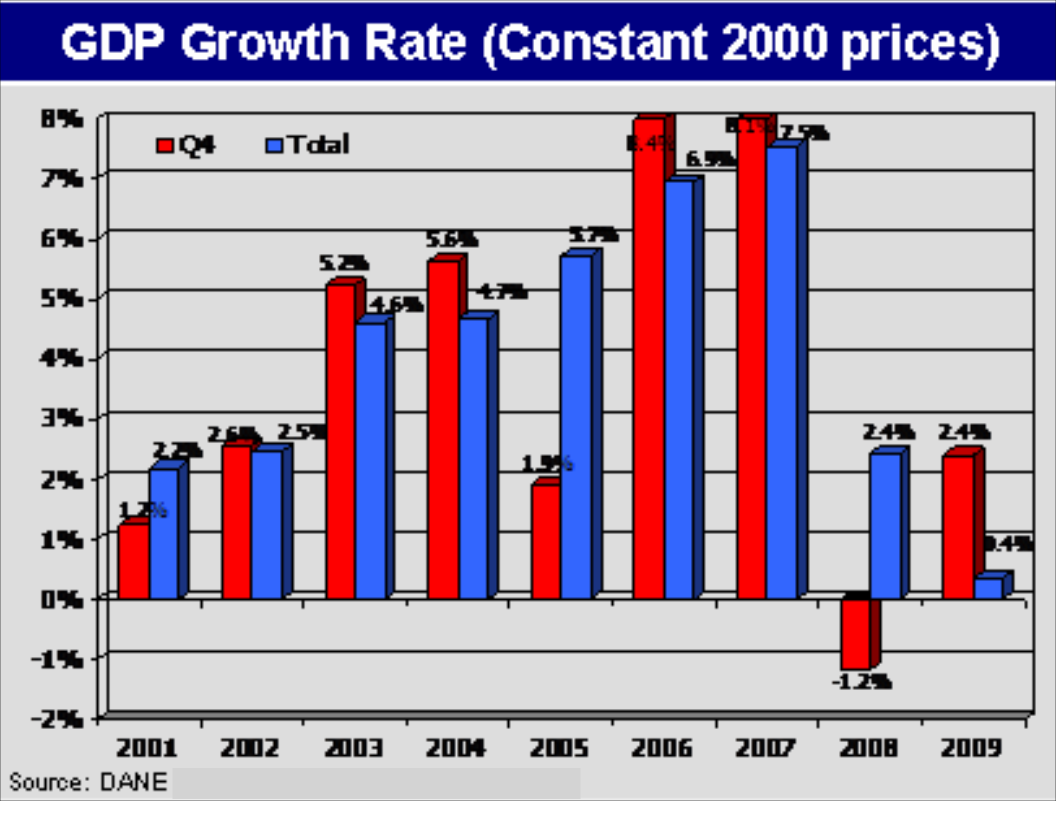

Colombia

In the fourth quarter of 2009 GDP grew

by 2.4% with respect to the same quarter

of 2008. The strength of this recovery

is similar to Argentina’s (2.6%) but

smaller than Brazil's (4.2%).

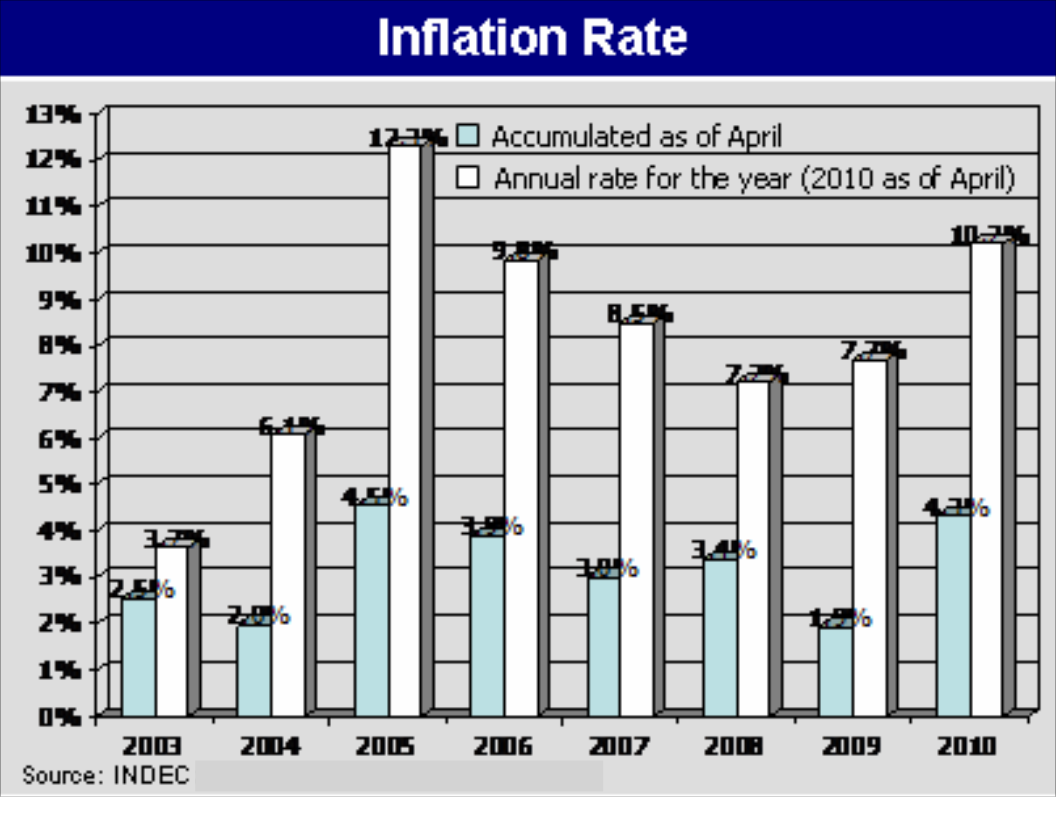

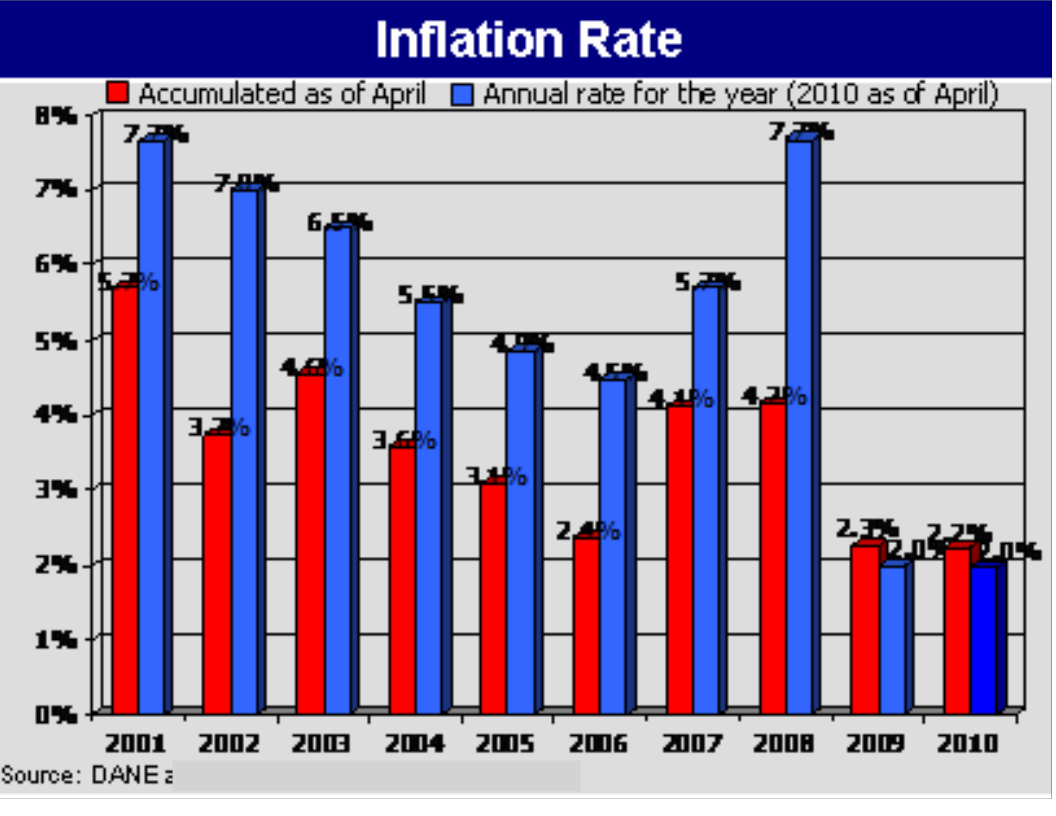

The case of Colombia is somewhat

different than the other three countries,

where inflation has already picked up,

as the annual inflation rate remains one

of the lowest levels in history in April.

Indeed, monetary policy was very tight in

2008 before the crisis fully developed as

inflation in 2007 and 2008 had been above

the Central Bank’s target.

Thus, the international recession combined

with tight monetary policy brought inflation

down to the lowest level in history. The

undesirable consequence of this policy was

that economic growth was perhaps curtailed

more than it was necessary and unemployment

higher. However, the good outcome is that the

country does not have to immediately increase

rates as in the case of Brazil but could enjoy

a dose monetary stimulation. In fact, in 2010

Colombia's Central Bank has adopted a more

active role by relaxing monetary policy

and there is even speculation about a possible

interest rate decrease.

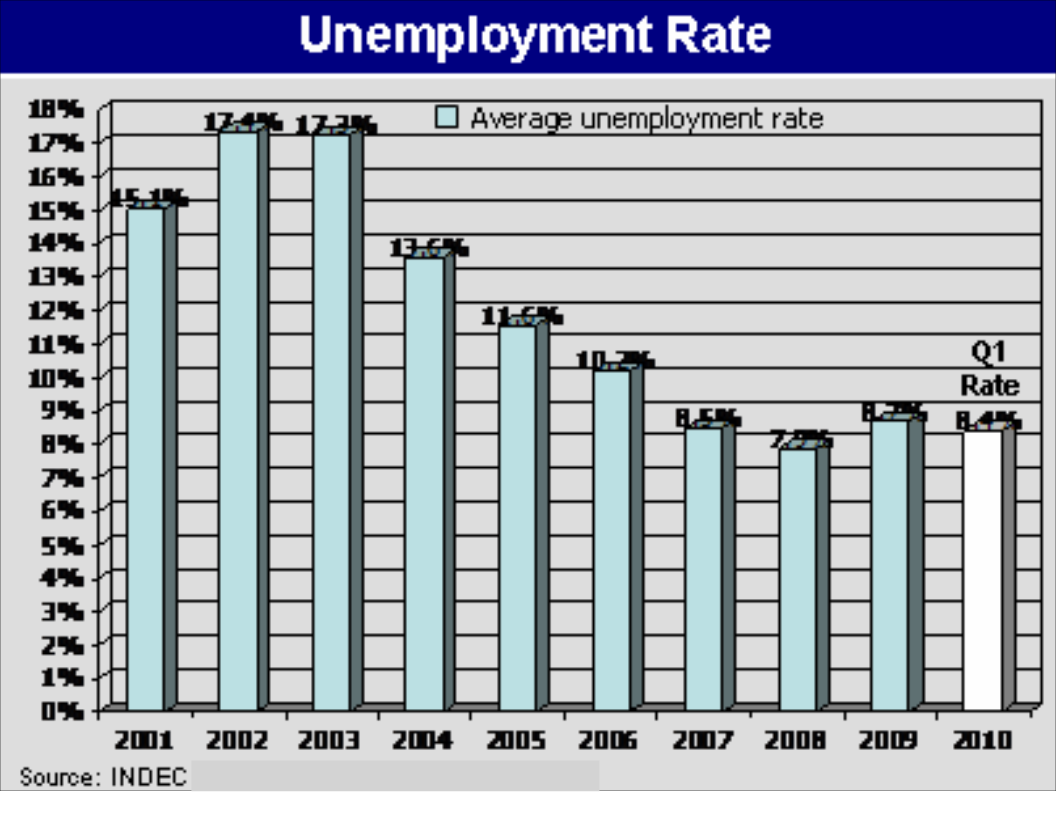

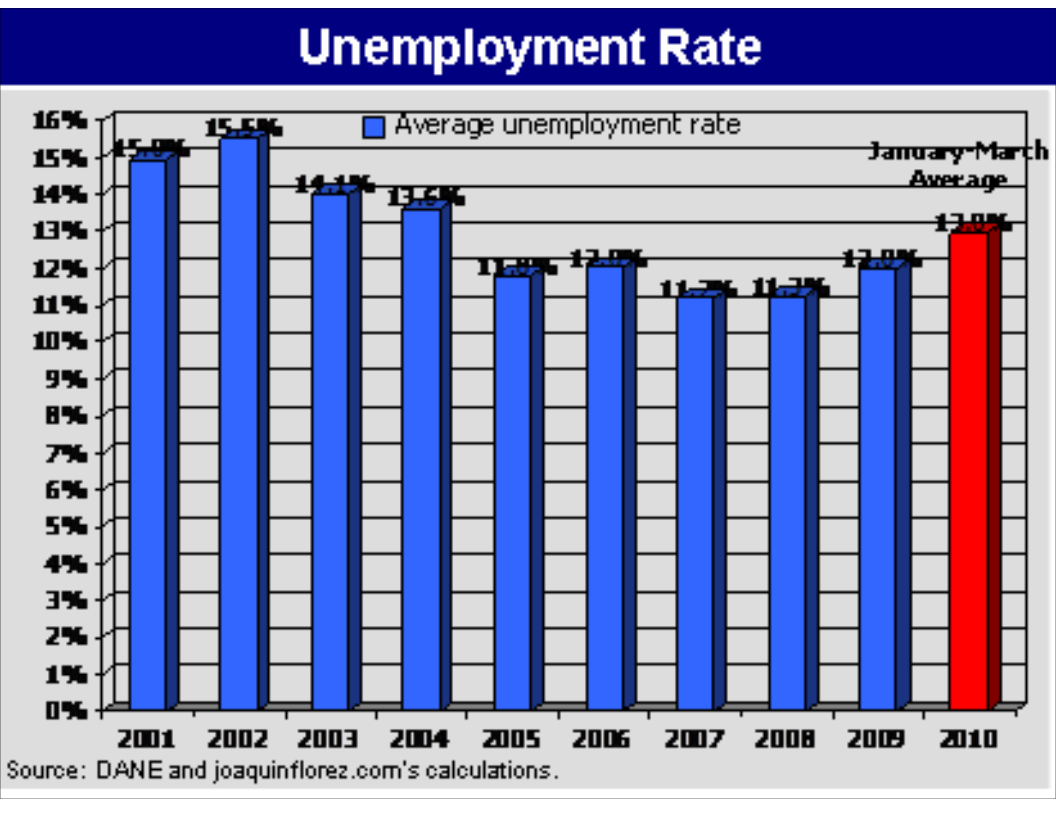

As was discussed on the previous issue of

Trends as the participation rate increased

the unemployment rate was meant to be higher.

Indeed, as had been predicted with a participation

rate above 62% the rate should remain at a level

of close to 14% which was effectively reached

in January. However, in March the participation

rate was slightly reduced pushing the unemployment

rate down so that the average for the quarter is

below 14%. This will remain a problem this year

and in the future unless policies to favor employment

are adopted. It should be stressed again that due

to extreme income inequality and a lack of a proper

social safety net in Colombia, unemployment

there is particularly harmful.

Part of the problem is that over the past decade

only capital friendly policies have been adopted

at the expense of the labor force. And unemployment

is not only bad for the individual and family suffering

its consequences but also for consumption, social stability

and mobility and for the economy as a whole. Indeed, unless

consumption increases in 2010 economic growth is likely

to remain depressed.

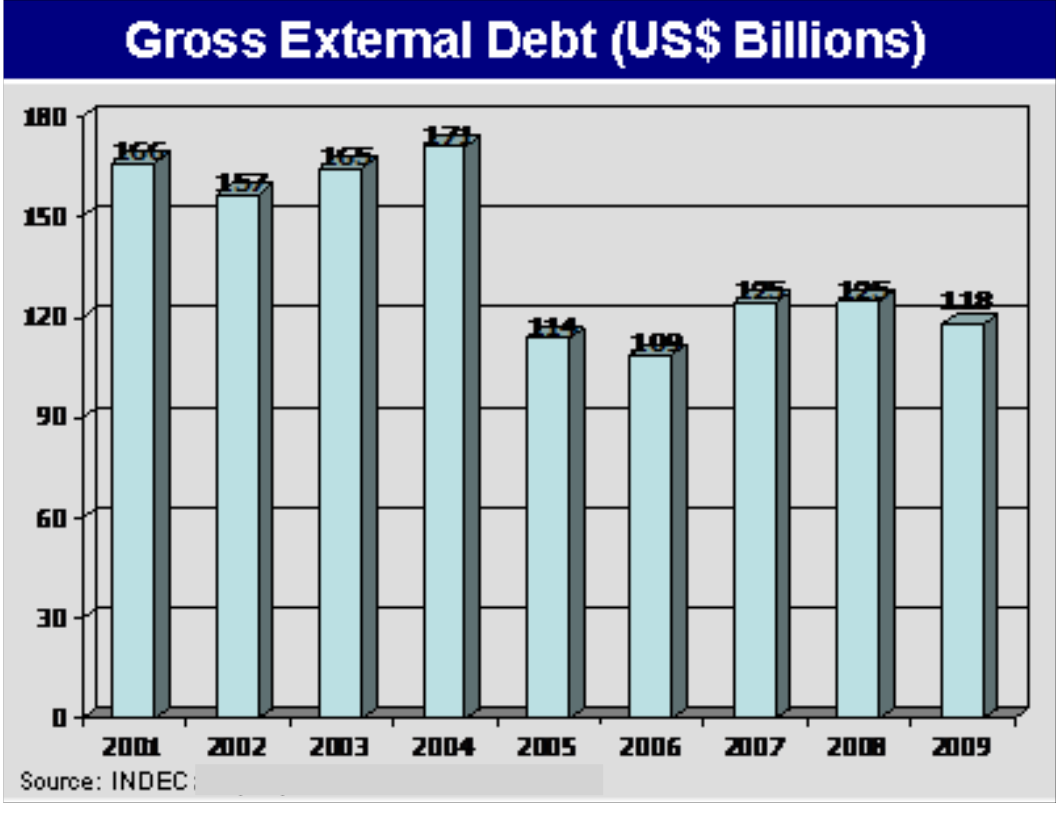

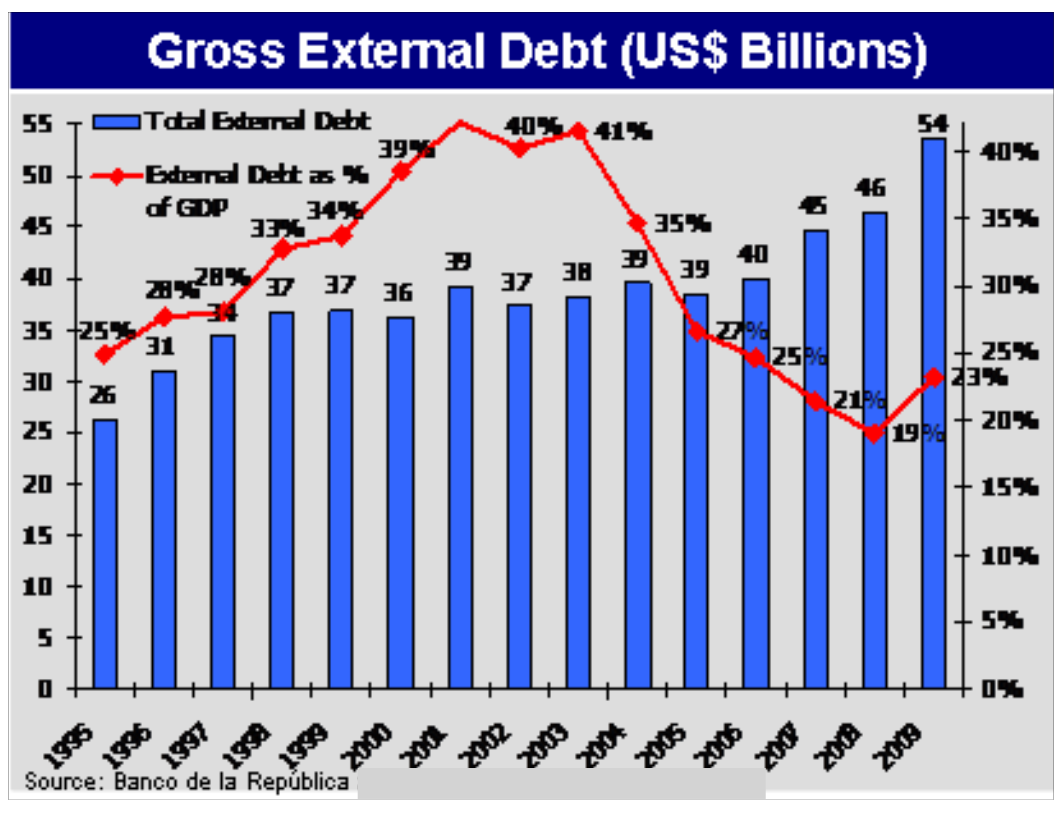

External debt will only increase in 2010

as the fiscal deficit expands due to a fall

in revenues because of the recession and

expenditures increases because of the lingering

effects of fiscal stimulation during 2009.

Colombia is currently seeking to improve its

credit rating and obtain the elusive investment

grade but these developments do not help.

At the same time, with the international debt

crisis looming, rating agencies will be less

sympathetic to consider rating improvements.

For Colombia, 2010 presents great opportunities

to consolidate a strong economic recovery

but also some serious challenges and risks.

The situation can be described in the following terms:

-

In 2010 Colombia has the opportunity to consolidate

a solid economic recovery by adopting a more restrictive

fiscal stance and a softer monetary policy given that

the risk of increased inflation is low.

-

GDP growth in 2010 is forecasted to be above the 2009

level (0.4%) but lower than the average for the decade (4.1%).

-

Now that the risk of a financial crisis has passed,

the government should concentrate in reducing the

fiscal deficit and improving public debt indicators

in order to bring them back to the levels observed

at the end of 2008.

-

The major risk for Colombia at this point is that

the economy remains relatively depressed as consumption

stays subdued due to the high unemployment rate.

-

Without a main policy change, the country is likely

to experience chronic unemployment of above 12%.

The new government should launch a major effort

to address this problem.

-

As long as unemployment remains at this high level,

income distribution is bound to keep deteriorating

making Colombia a serious candidate to have the worst

income distribution in the world with all of its ailments.

-

Given the reduction in inflationary pressures interest

rates are likely to remain low favoring the recovery

and increased investment.

-

As the economy recovers, imports will increase relatively

faster than exports bringing about a deterioration of

the trade balance.

-

The other major risk for 2010 is political as a new

president takes over. However, the market seems

to already have discounted this factor and appears

comfortable with either of the leading candidates.

-

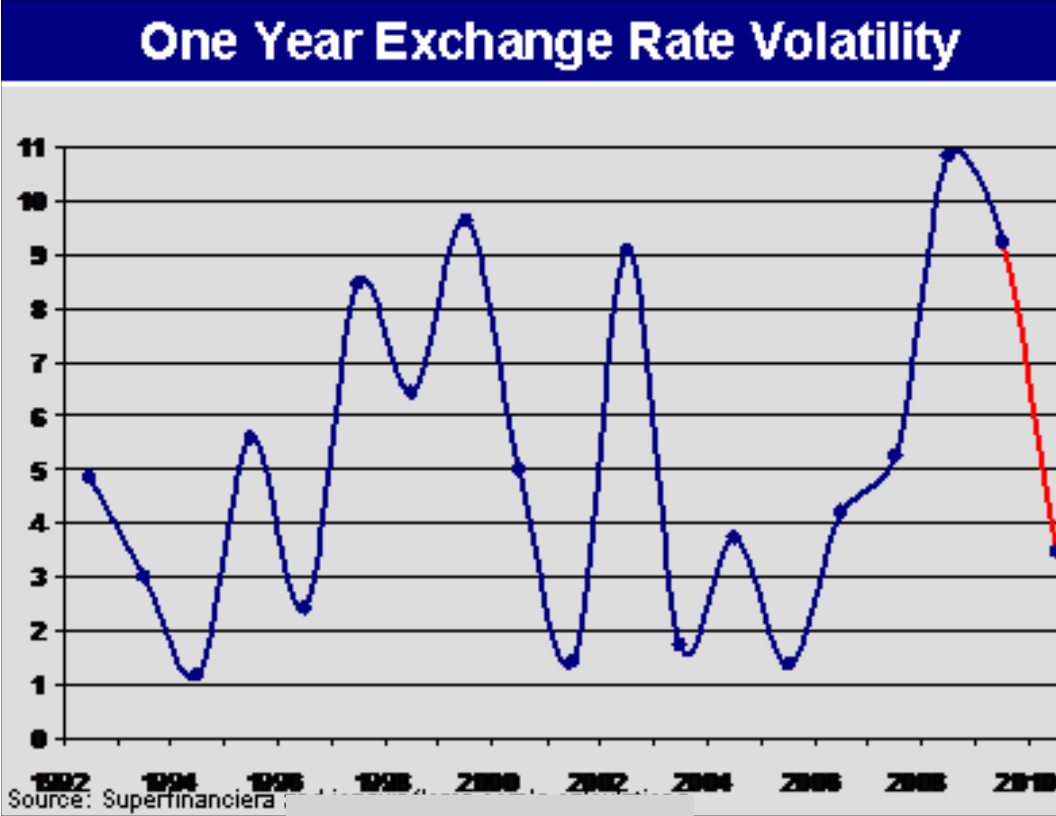

Although volatility is now lower, implying a decrease

in risk, the new president may change this if he is

unable to articulate a clear and sound economic policy

agenda for the next four years.

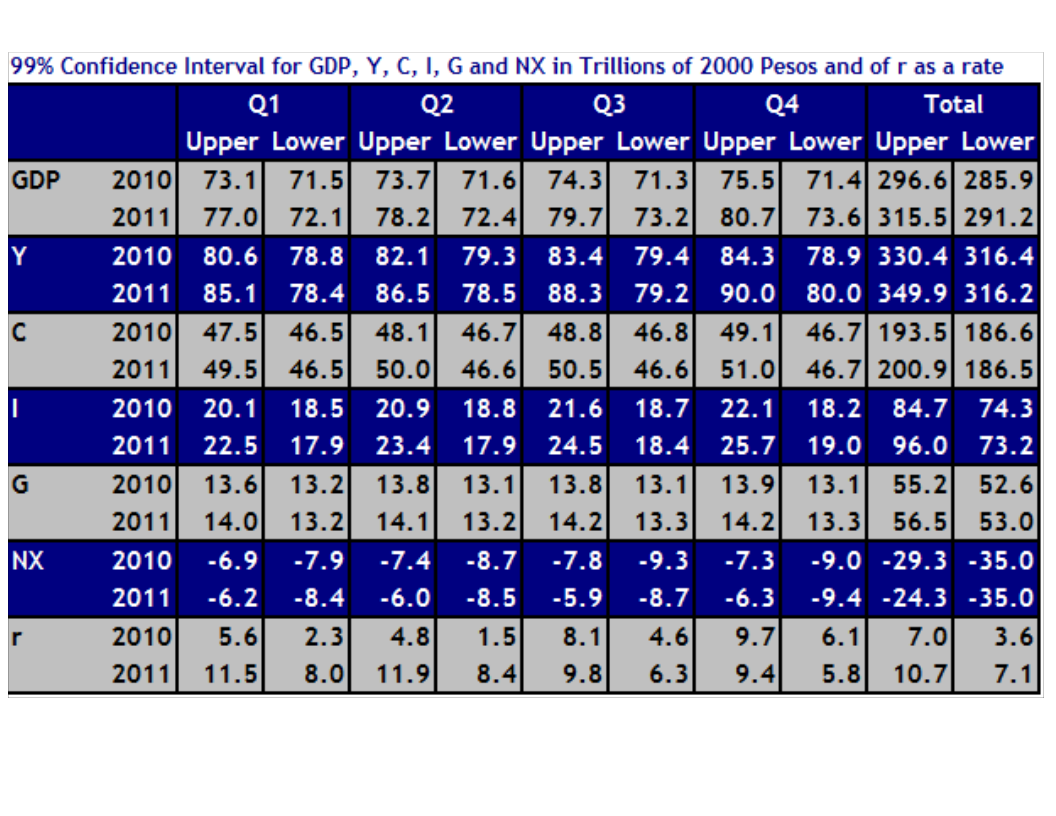

Macroeconomic Model -Colombia-

The compact macroeconomic model (CMM)

has been updated with the latest information

available in order to produce quarterly forecasts

until 2015. This is a multiple equation stochastic

model that was run at the 99% confidence

level with 50,000 iterations.

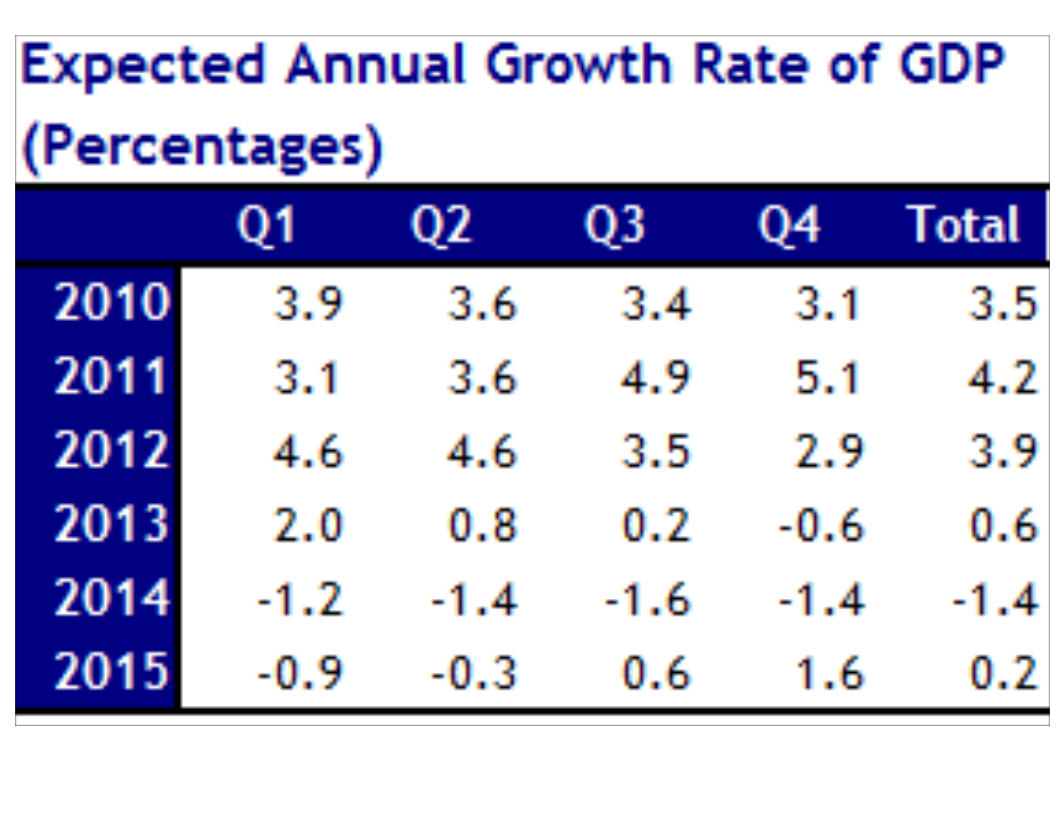

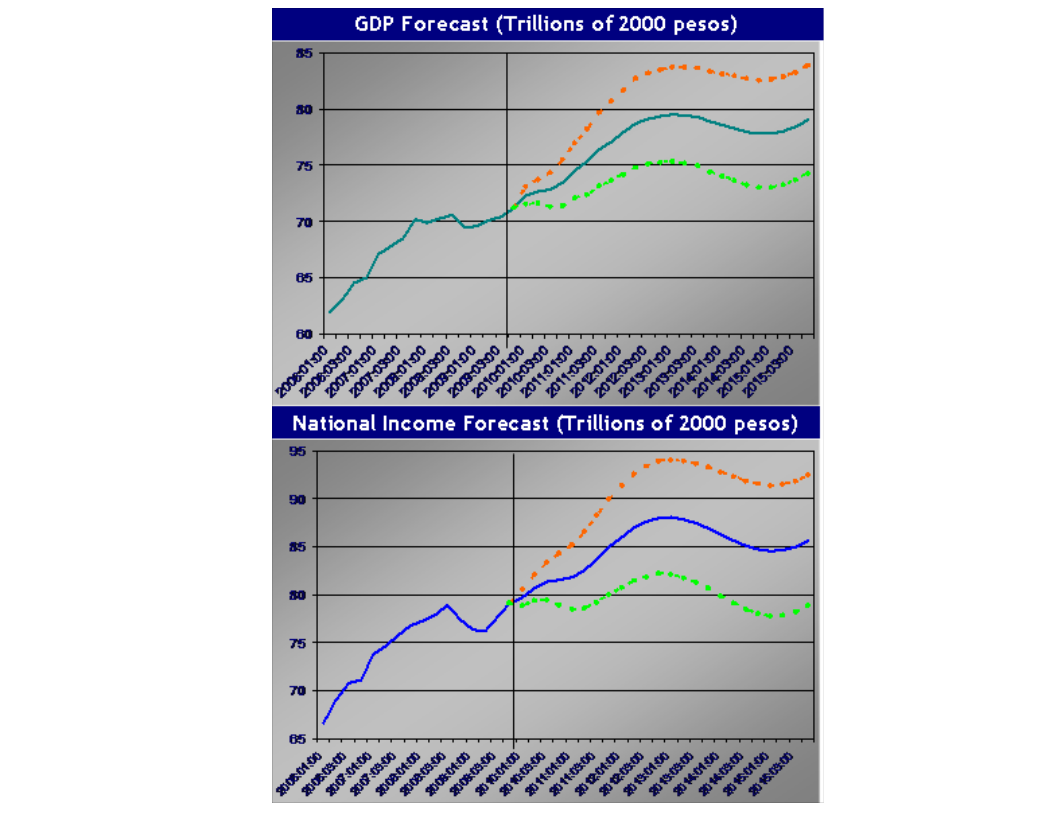

In the last issue of Trends GDP growth had been

forecasted to be 2.1% for the fourth quarter

of 2009 and 0.2% for the whole year. The

actual numbers were 2.4% and

0.4% respectively which somehow validate the

effectiveness of the model. For the first quarter

of 2010 the model now forecasts a growth rate of

3.9% with respect to the same quarter of the

previous year while for the entire year has an

expected annual growth rate of GDP of 3.5%.

On the first quarter of 2010 issue of Trends

the expected annual growth rate of GDP for

2010 had been calculated at 1.2% for the year.

Now growth is expected to be higher due to

improved investment and household consumption.

At that time, the CMM was also forecasting a

mild recession in 2011 while it now predicts

growth for that year to be at 4.2% and a

recession in 2014.

The different versions of the model seem

to suggest that there may be a recession

between 2010 and 2015 unless policy measures

can improve consumption growth and reduce

investment volatility. Whether unemployment

can be reduced will make an important

difference for growth stability.

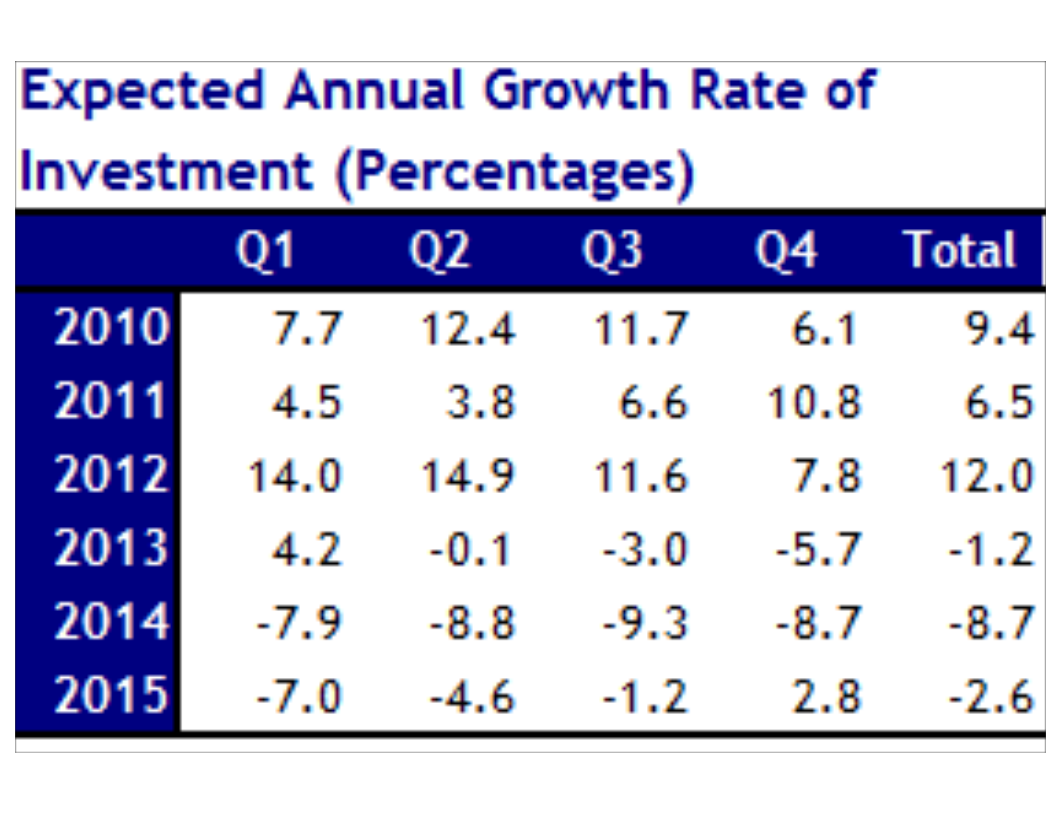

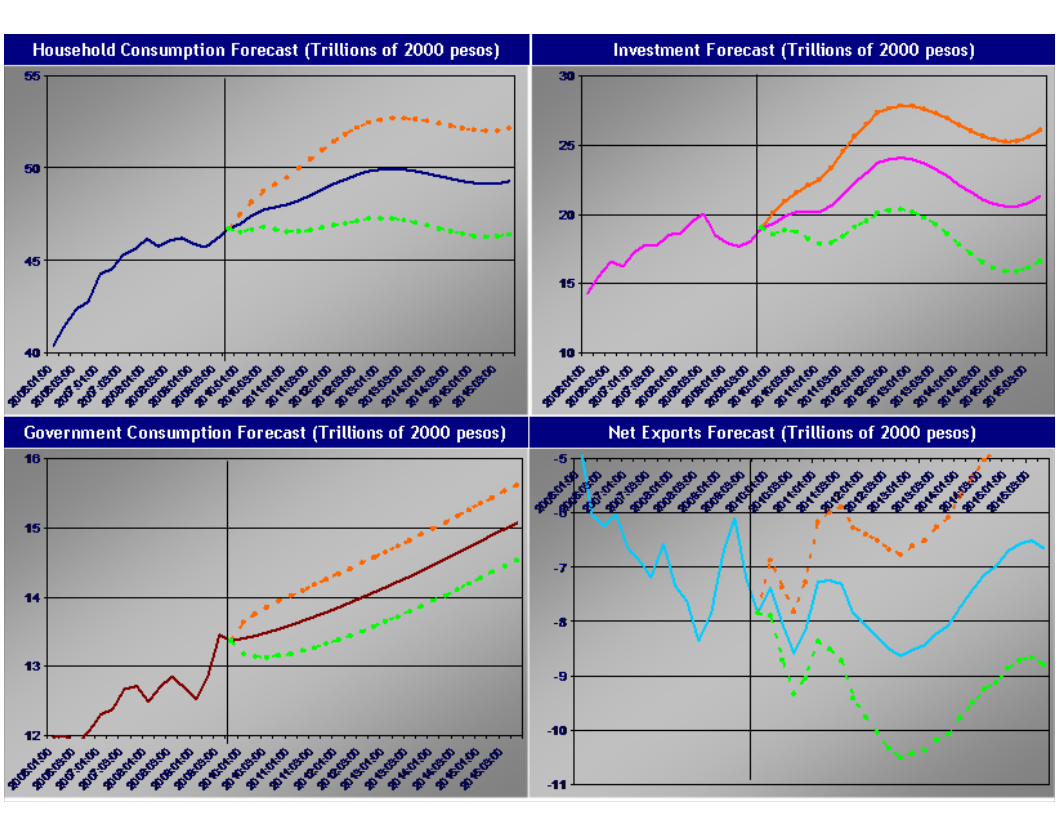

On the other hand, the forecast made in the

Q1 2010 issue of this newsletter expected

the growth rate of investment for the fourth

quarter of 2009 to be -1.6% and -6.0% for

the entire year. The actual numbers were

3.0% and -5.2 respectively.

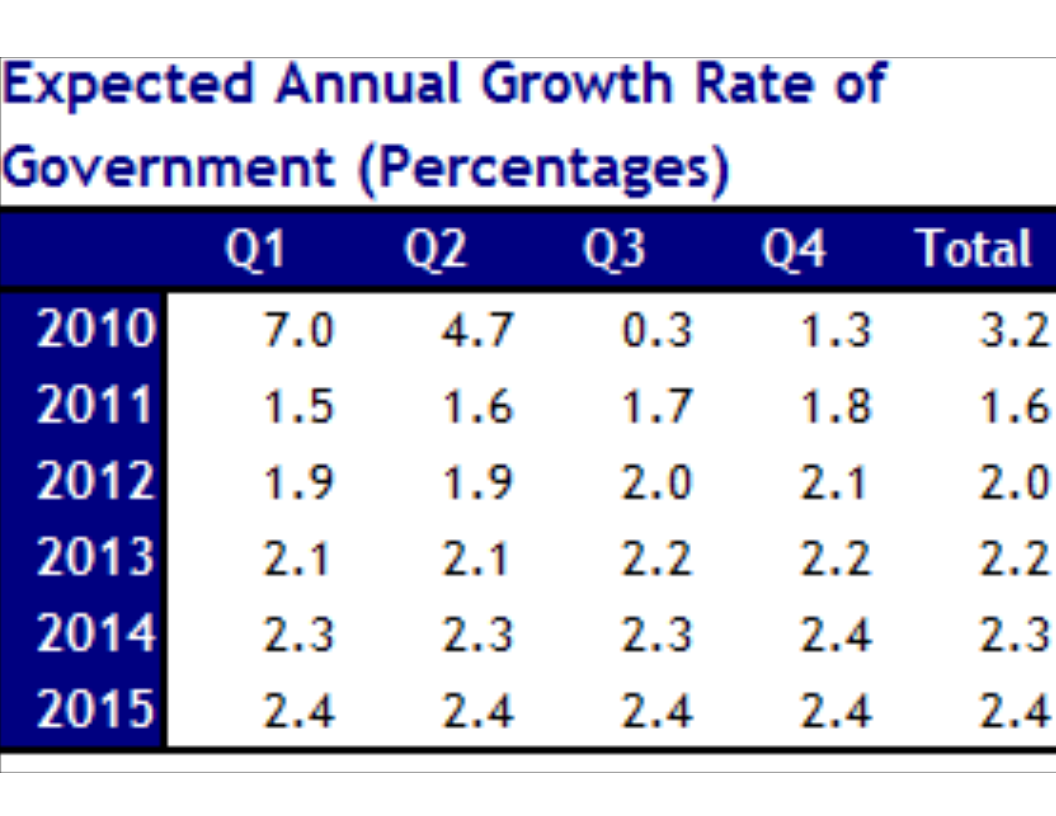

In order to fight against the recession

the government was forced to adopt a more

active fiscal policy by increasing expenditures.

However, given budget rigidities it is difficult

to promptly increase government expenditures

and what usually happens is that they will

peak well beyond the end of the recession

as seems to be the case right now.

The growth rate of government expenditures for the

fourth quarter of 2009 had been forecasted to be

5.5% in the Q1 10 issue while the growth rate for

the whole year had been estimated to be 2.8%.

The actual numbers came in at 5.3% and 2.9% respectively.

Given the large increases in the fiscal deficits

of 2009 and 2010 the government does not have a

lot of room to increase expenditures further.

Also, central government foreign debt had the

largest increase in history during 2009 while

domestic debt had the second largest increase

in history. Thus, probably the new government

will have to address this problem by cutting

expenditures, increasing taxes or both.

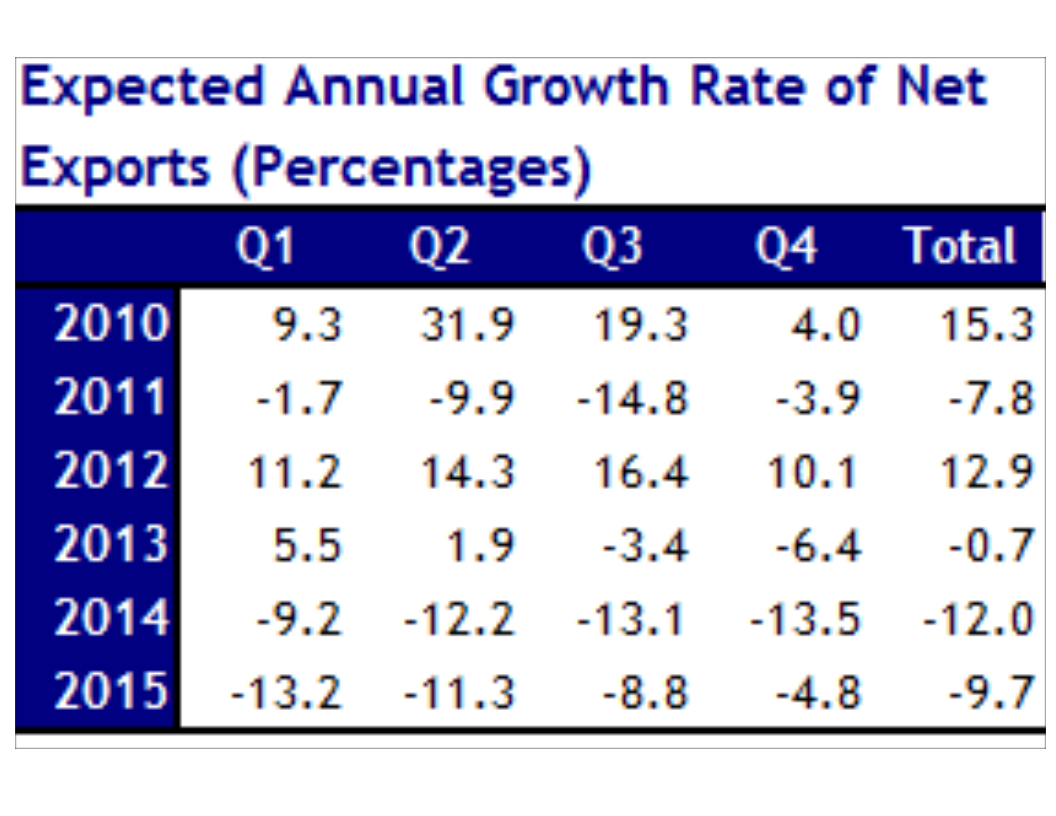

Considering these technical details,

net export growth had been forecasted to

be -14.3% for the fourth quarter of 2009

and -13.9% for the whole year. The actual

numbers came at -0.5% and -10.5% respectively.

The actual GDP number for 2009 was $281.4

trillions of 2000 pesos which is well within

the range forecasted at the 5% error level.

This confirms that, at least in the short run,

the model performs rather well.

Household consumption, which is the most

important determinant of GDP, will grow

at a rate between 4.9% and 1.2% during 2010.

It is therefore expected to be between $186.6

and $193.5 trillions of 2000 pesos. After 2010,

consumption growth will remain relatively soft

until 2013 and then contract in 2014 and 2015.

However, it is important to underline that given

the width of the confidence intervals GDP and

household consumption may never contract so that

the forecasted 2014 recession may indeed never

materialize. For now, the country seems to be headed

for three consecutive years of acceptable economic

growth with an average of 3.9% and start a gradual

slow down in 2013. The historical data and the CMM

model seem to suggest that growth rates much above

4% are unsustainable in the long run in Colombia.

Government expenditures are expected to grow throughout

the forecast period. This is the most stable variable and,

unless there are a major policy changes, no substantial

deviations from its trend behavior are expected.

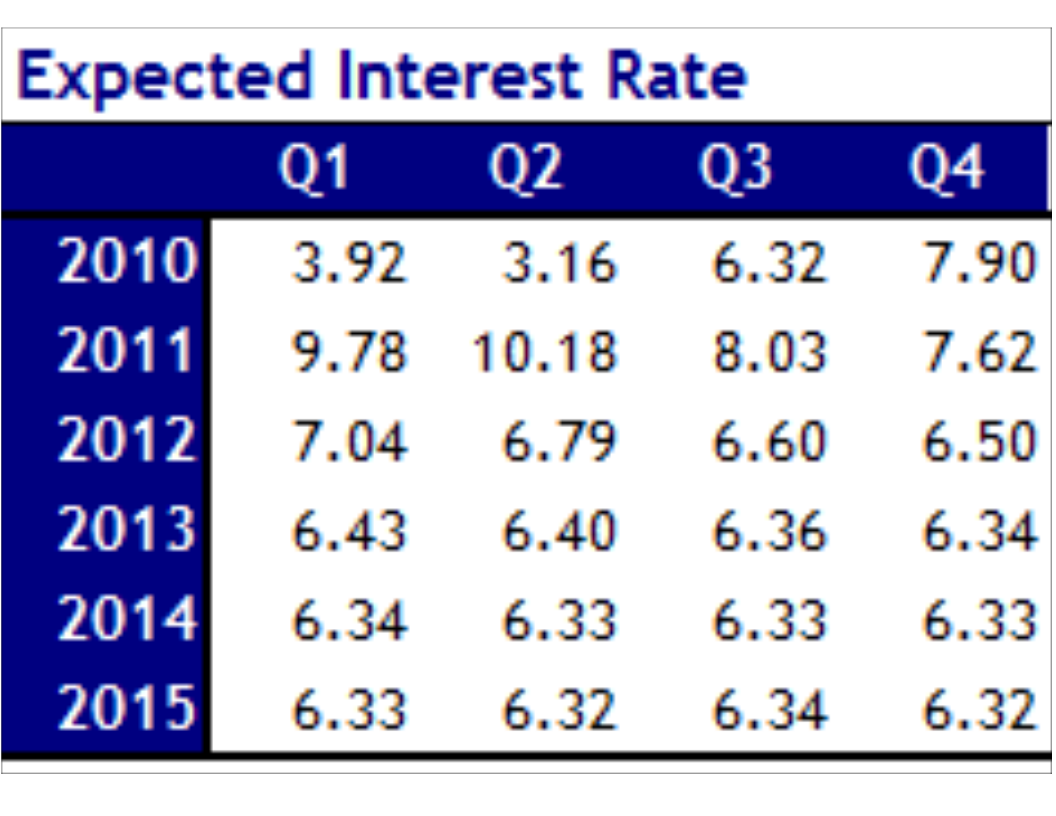

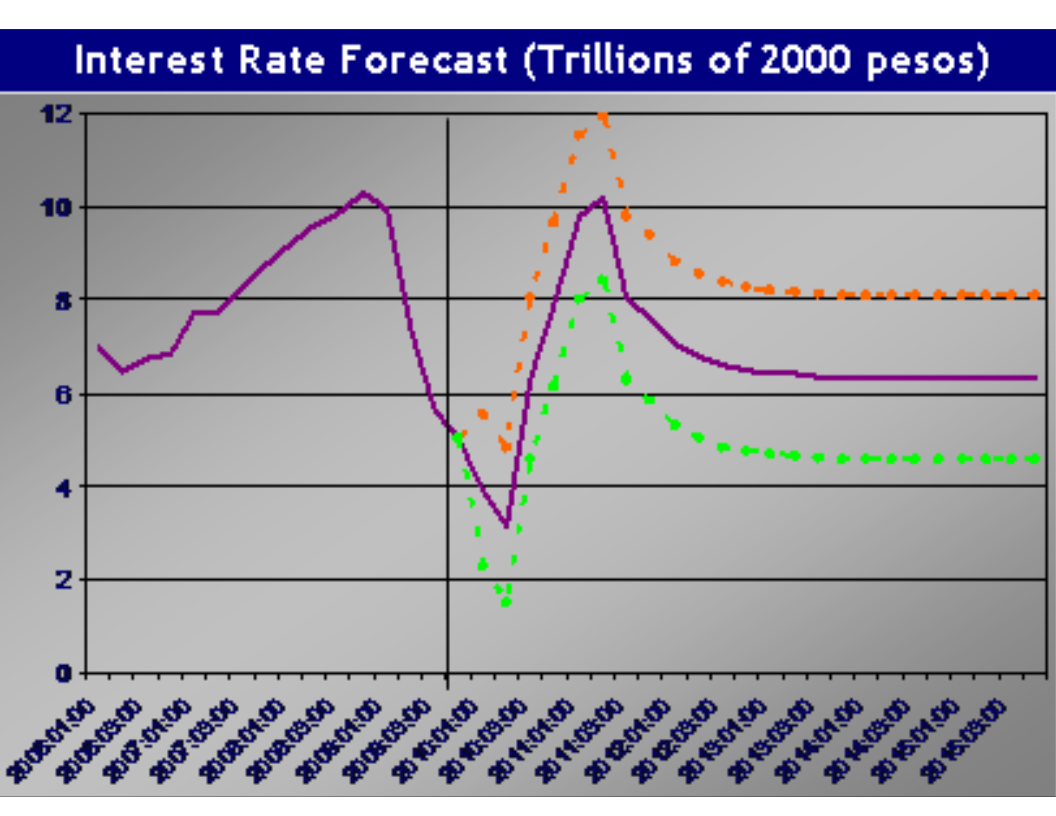

During 2010 and part of 2011 interest rates should

increase as the economy recovers. Interest rates

right now are at an all time low and there is little

room for them to decrease anymore unless the economy

fails to recover. The model is forecasting that the

average 360 day CD rate in 2010 will be between a

maximum of 7% and a minimum of 3.6%, in 2011 between

10.7% and 7.1% and between 2012 and 2015 between

8.5% and 4.6%.

The graphical depiction of the confidence intervals

at the 99% level is useful to see the possible amount

of fluctuation of each variable.

Mexico

Also while the U.S. had four consecutive

quarters of negative real growth, Mexico

had five as of the end of 2009, making

the recession there not only deep but also long.

Nonetheless, in the first quarter of 2010 Mexico

will be the last country to pull out of the

recession after being the first to go into it.

In 2010 Mexico will probably show a strong recovery

with GDP growing above 4%. Mexicans will be grateful

to have left the most serious economic crisis in at

least three decades. While it is true that in 1995

GDP contracted by 6.2% and there was a major financial

crisis, GDP growth for the previous year was 4.5% and

5.1% for the subsequent year. Thus, this crisis seems

more distressing than the one observed between 1994

and 1995.

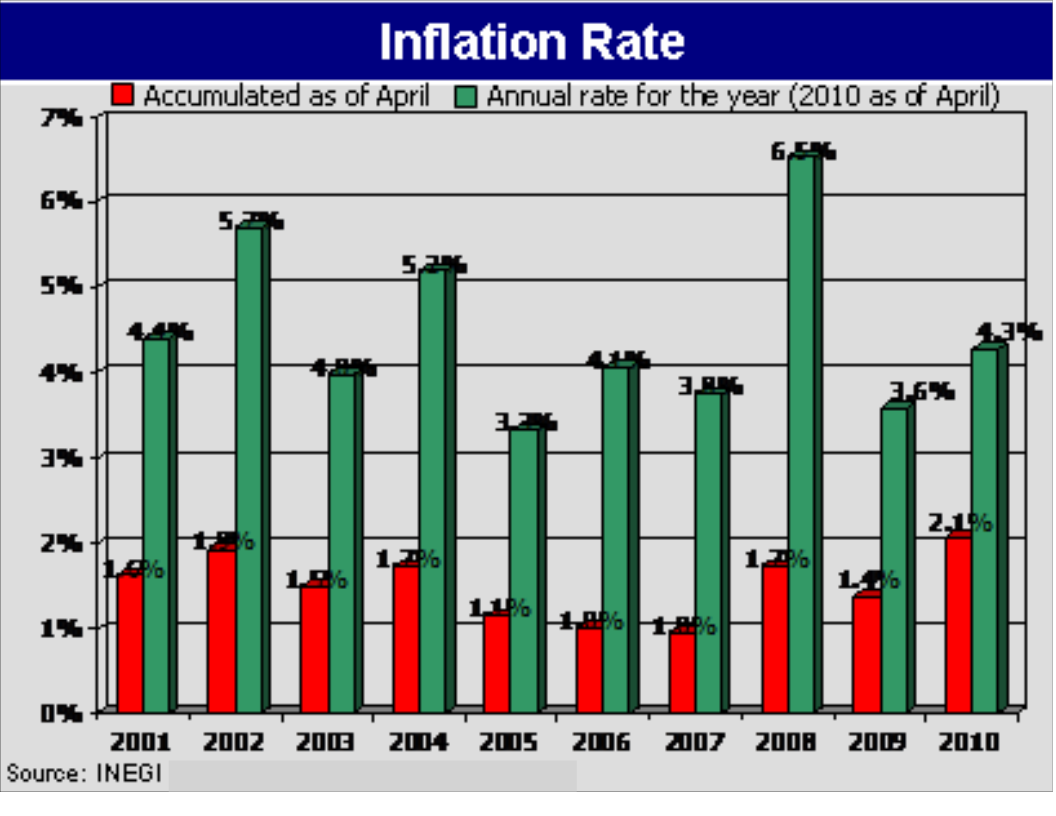

Inflation for the year will most likely

be close to 5% well within the targets

established by Mexico's Central Bank. With

a low inflation rate and no major inflationary

pressures on the horizon, a strong recovery

is certainly going to take place. Furthermore,

the latest evidence of robust growth in the

U.S. will only help the Mexican economy.

If Mexico ever looked bad because of the

U.S. recession now it looks good due to

the recovery.

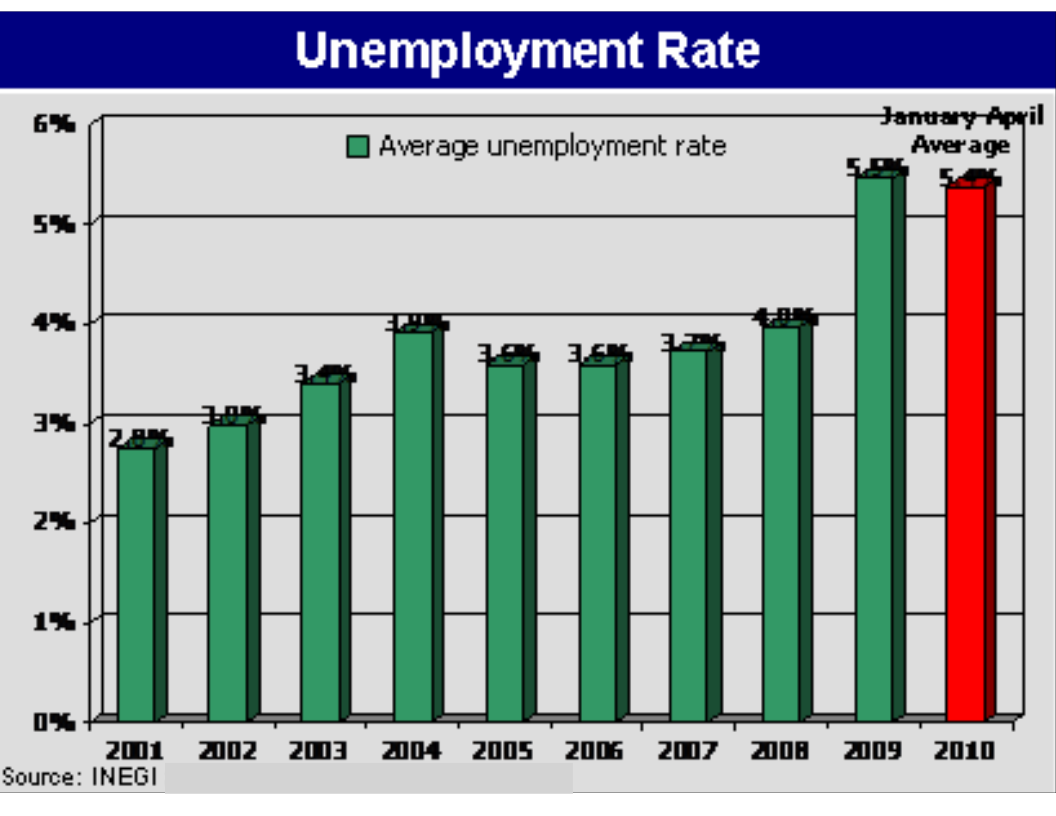

The large increase in the unemployment

rate observed in 2009 will surely be

one of the main economic policy challenges

during 2010. Although the recovery seems

well cemented the large increase unemployment

could hinder household consumption thereby

affecting the recovery.

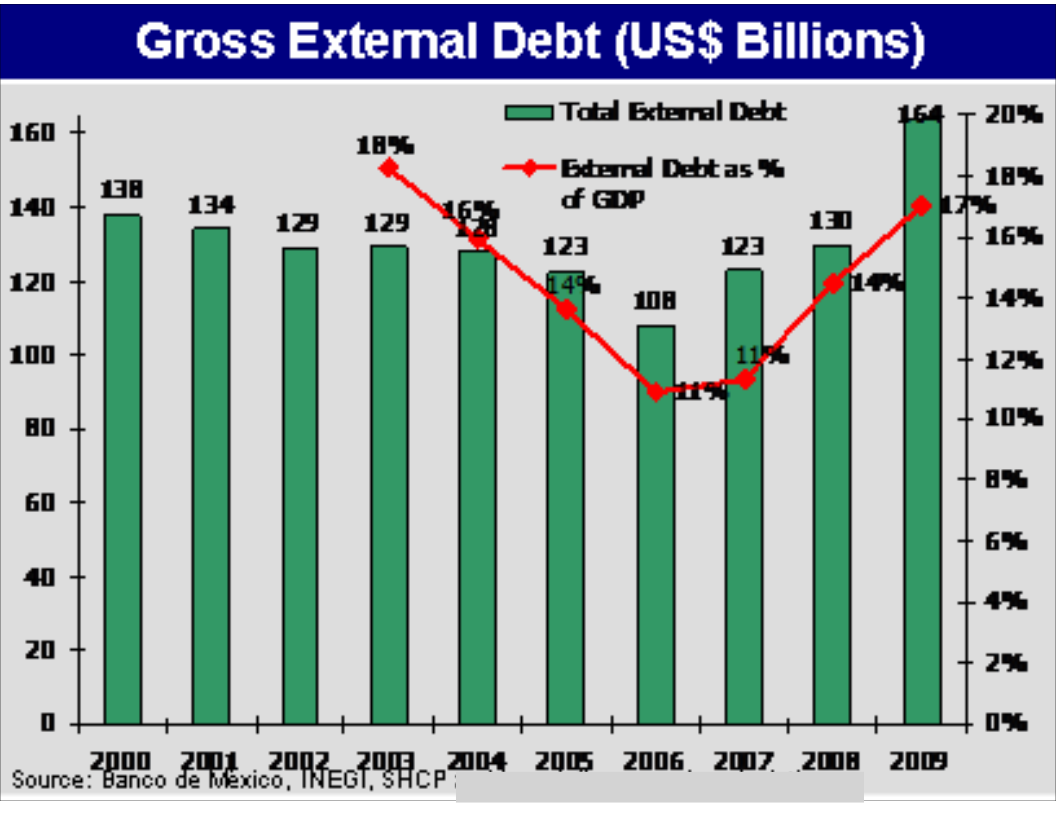

However, this is not a good moment to be

increasing debt levels. Indeed, with

the development of the European debt

crisis interest rates for Sovereign

debt are likely to keep increasing.

Nonetheless Mexico in 2010 will be

much better off:

-

GDP will grow above 4% during 2010.

-

The most important risk for the

Mexican economy is that the unemployment

rate remains relatively high affecting

consumption and the potential of the recovery.

-

The added debt burden represents an additional

fiscal pressure to already stressed public finances.

-

Inflation does not seem to be a risk at this

point and will probably remain under control.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}