Economic Trends -Latin America-

February 22, 2010

This is the third issue of Trends, a quarterly online Newsletter intended to inform readers about the latest economic developments in the four largest Latin American economies. The first issue of the Newsletter discussed how Latin America was being affected by the global financial crisis and recession. At that time, only Argentina was not already showing negative rates of economic growth. On the second issue all of the four countries under consideration had already negative rates of growth. As the United States has emerged from the recession, Latin America is beginning to show signs of improvement with respect to GDP growth.

Probably it will take years to reverse the damage that has been done to these economies in terms of the employment situation, even with a strong economy. The regular person will still suffer the most as social safety nets are almost non existent.

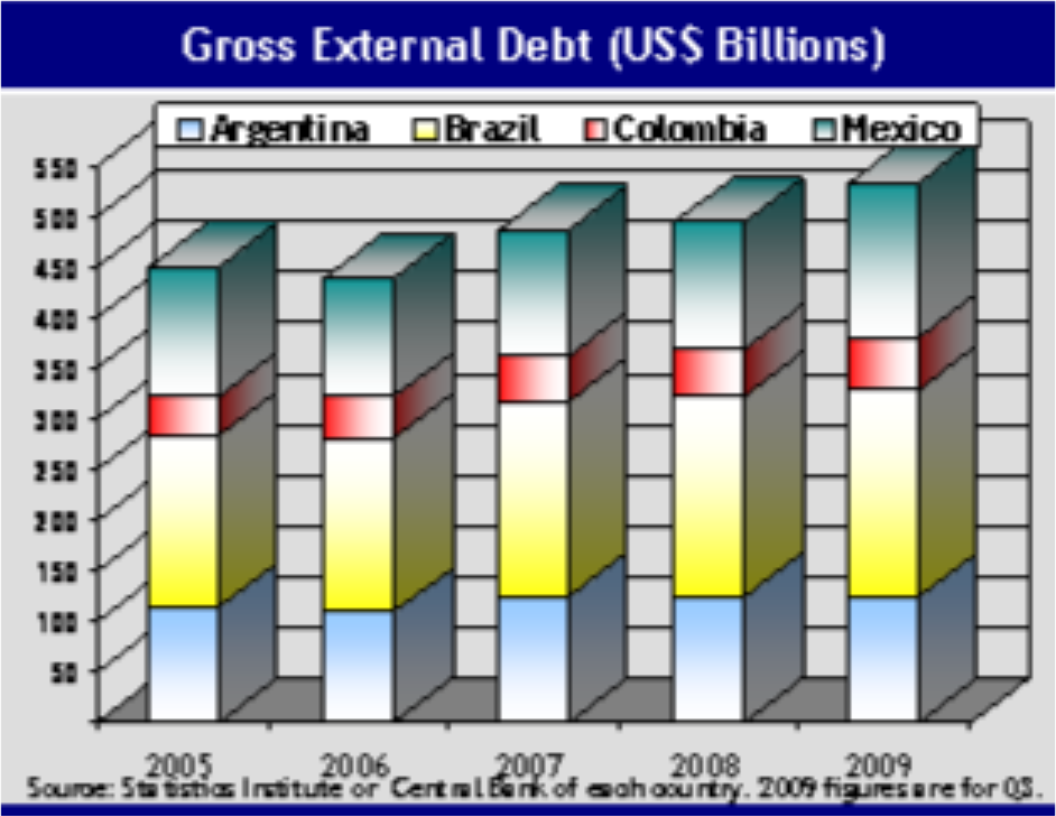

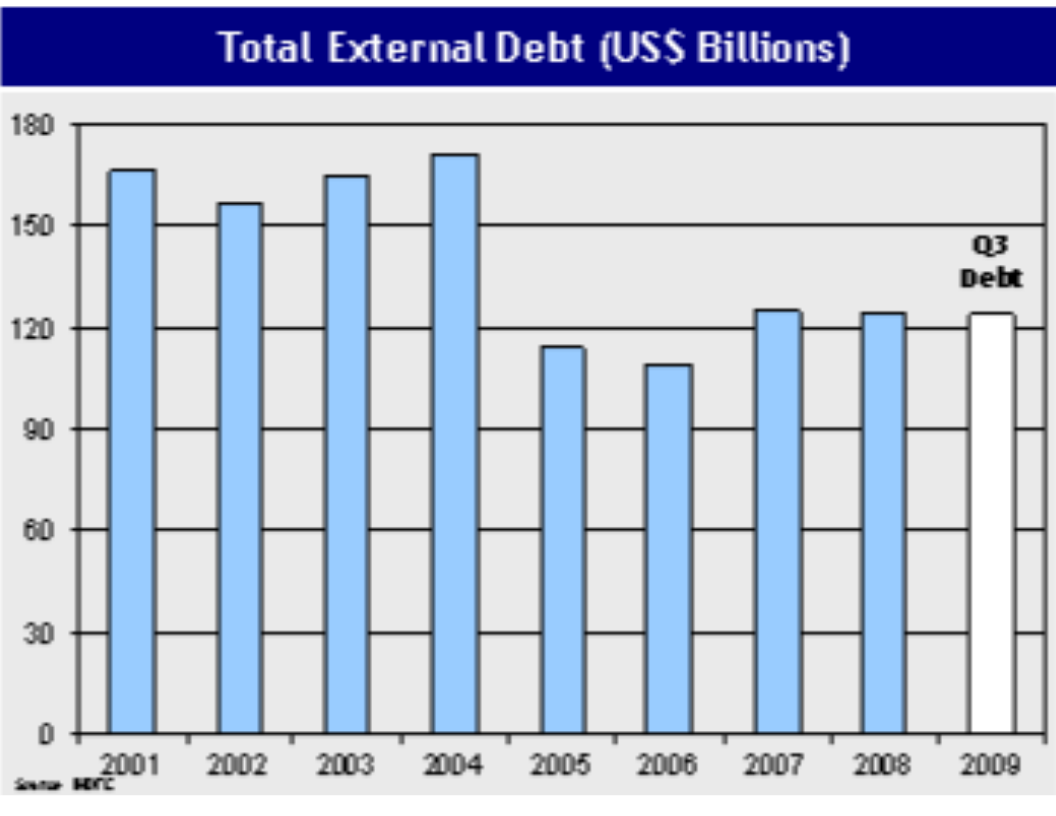

Gross external debt for the four economies increased by 8% in dollar terms between December of 2008 and September of 2009. This is equivalent to US$39.5 billion with Mexico being responsible for 73% of the increase or US$28.7 billion.

Public debt levels have risen significantly in the cases of Mexico and Colombia. Indeed, public debt in Mexico increased US$34.2 and in Colombia US$5.6 billion during the period. There is no doubt that fiscal stimuli played a role on these increases. However, this is not the end of the story because domestic public debt levels have also increased stressing even more the fragile local financial markets and crowding out private investment which is badly needed for a strong recovery

As the recession ends, tax revenue will increase allowing governments to expand debt in a less aggressive way. However, the debt stock will still be much higher than at the end of 2008 as countries find it difficult to control their fiscal deficits and stimulus measures.

The result of the current crisis is a large expansion in unemployment and debt levels accompanied by renewed inflationary pressures and uncertain prospects about GDP growth.

Argentina

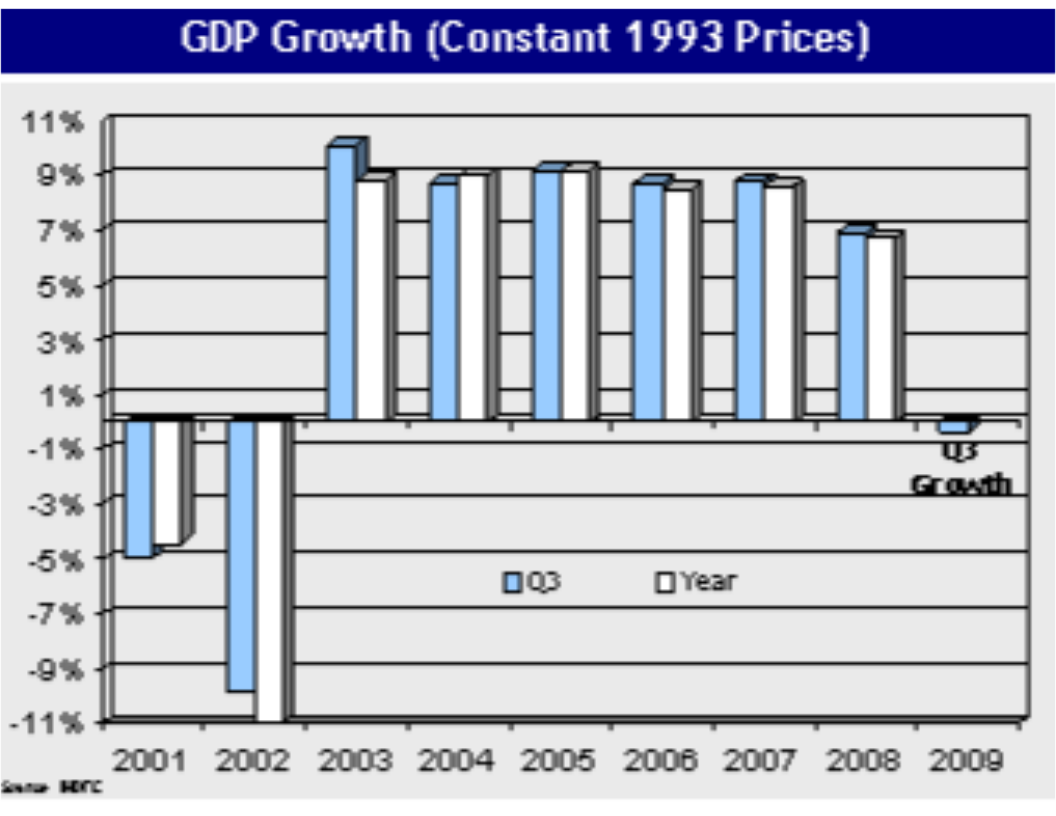

GDP Growth

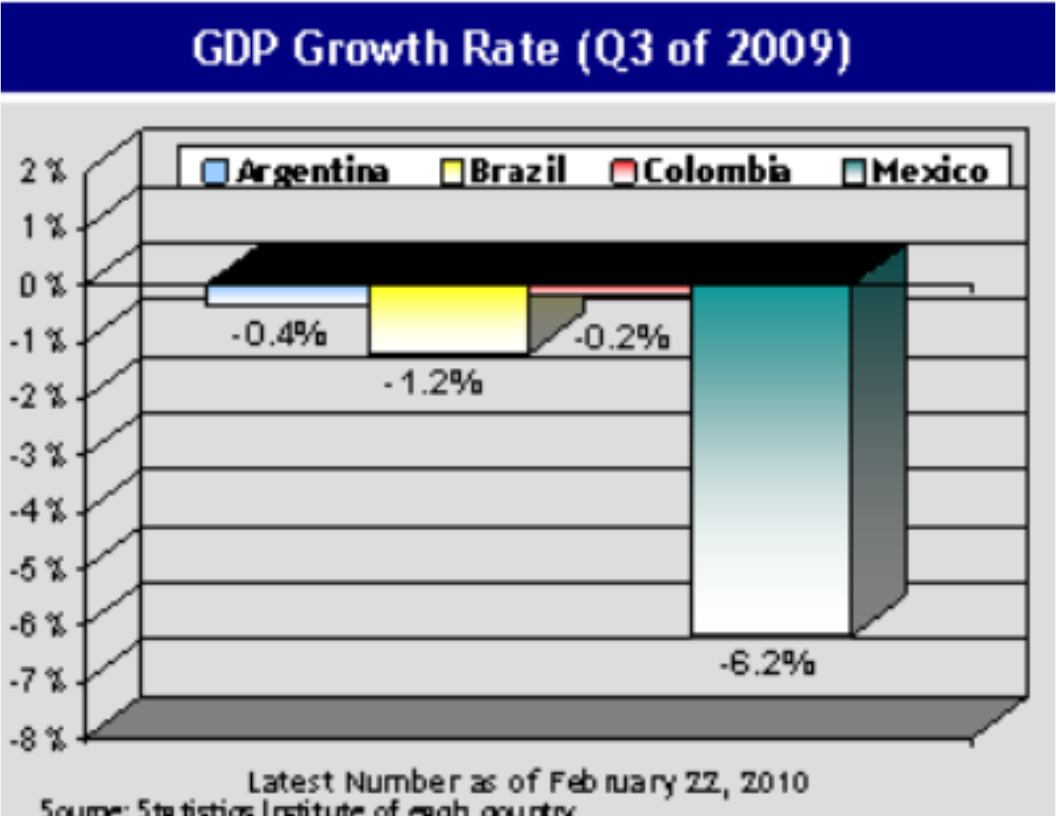

Indeed, GDP contracted at an annual rate of -0.77% during the first quarter of 2009 and of - 0.35% on the second. As well as in the rest of the region there has been a large adjustment in the current account with imports falling severely thus mitigating somewhat the fall in household consumption and private investment. Therefore, the decline in Gross National Income (GNI) has been longer and deeper than the one observed for GDP. In effect, GNI has now contracted for three consecutive quarters by -1.43%, -2.91% and -2.53% during 2009. This is despite a large fiscal effort that has expanded public consumption at rates of 6.8%, 6.3% and 8.1% in the same period. Due to this effort and other factors, Argentina may have a shorter recession than the other three countries emerging in the fourth quarter of 2009.

Prices

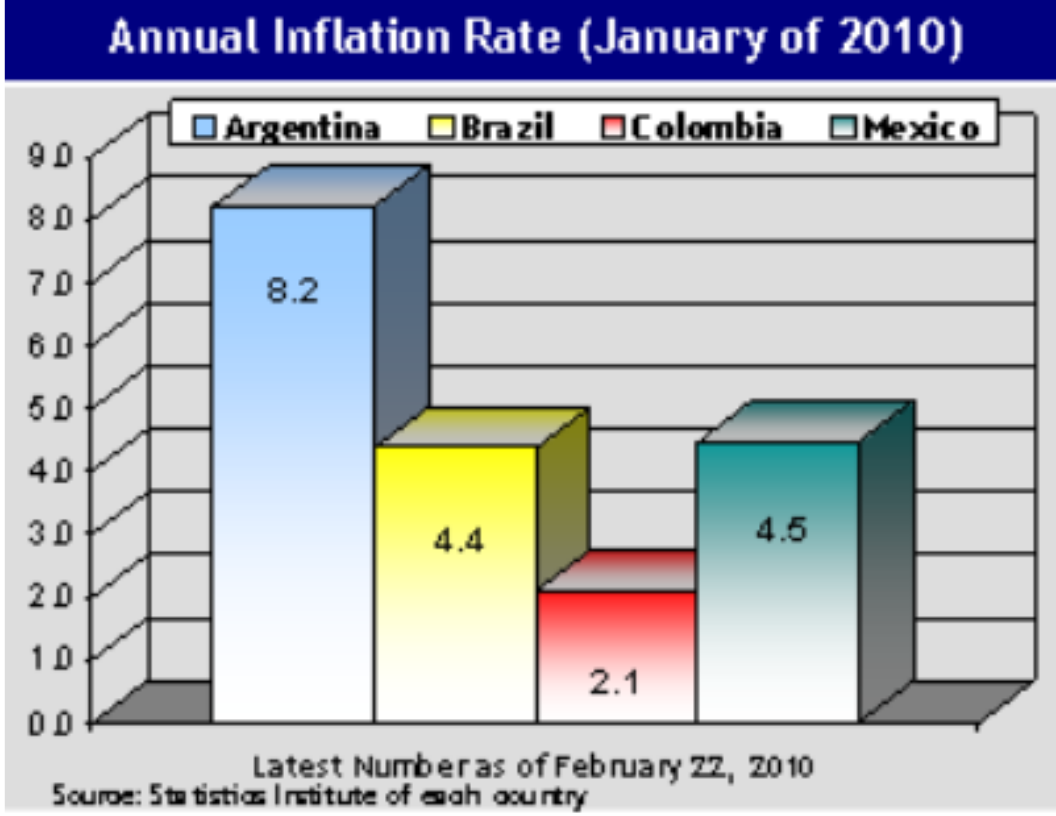

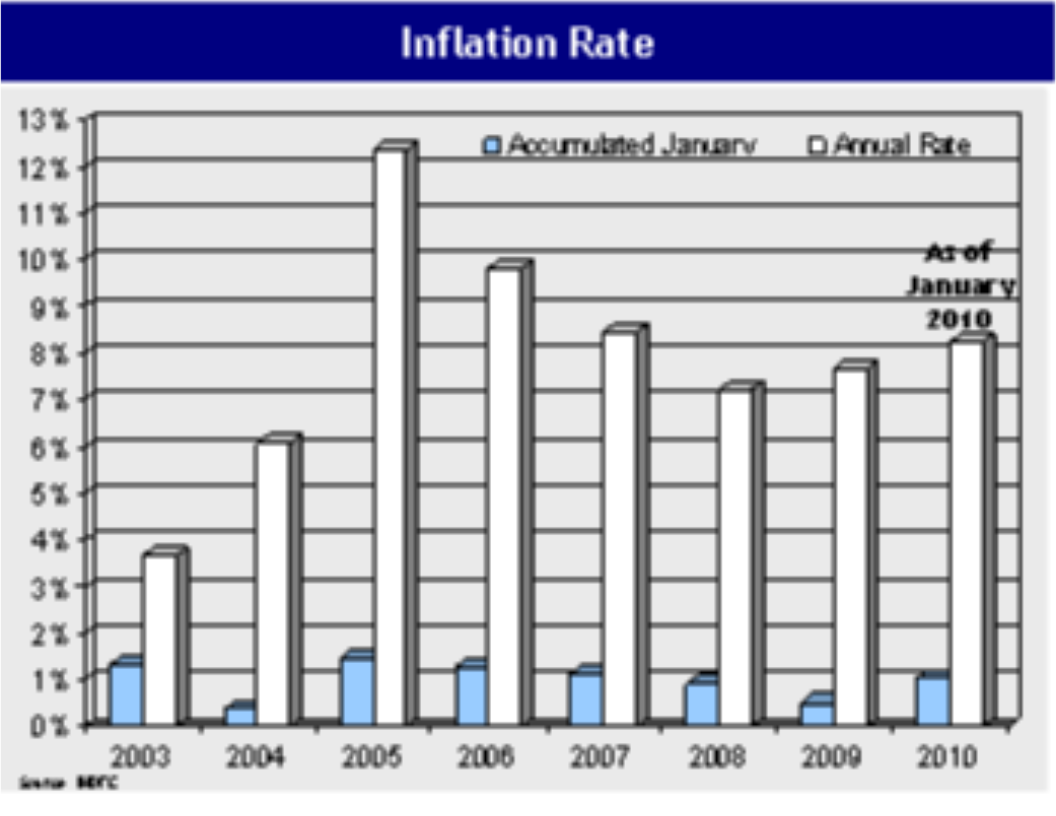

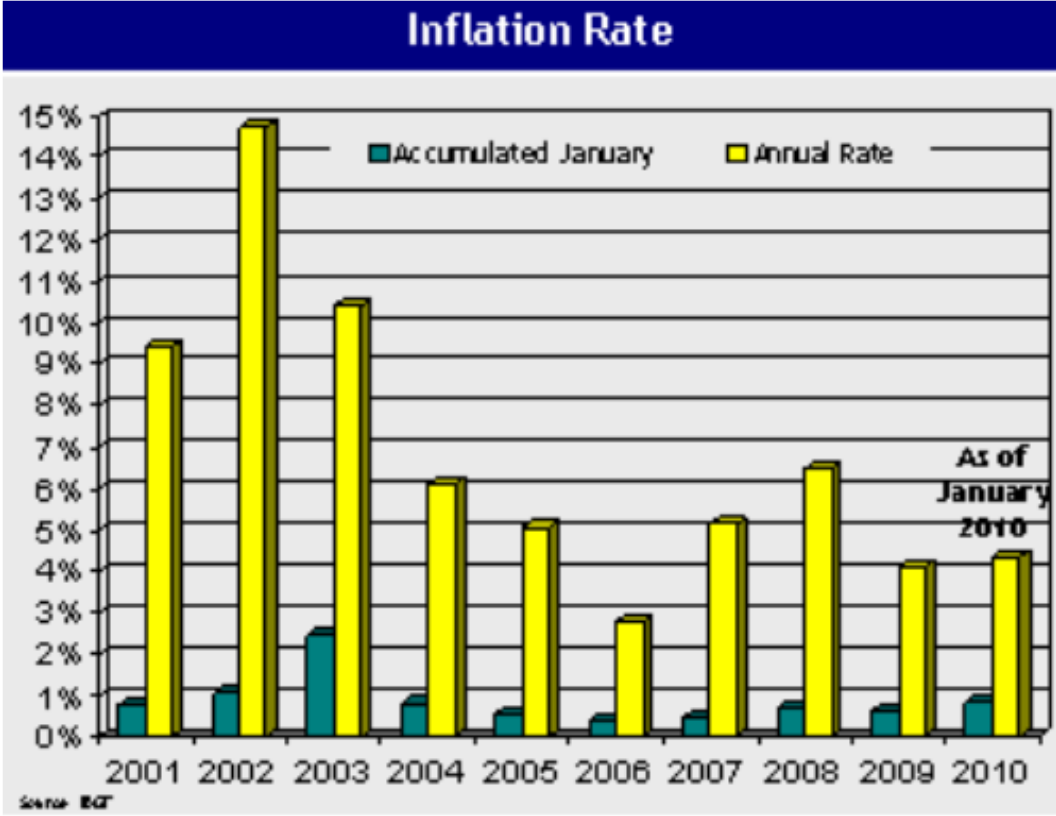

The annual rate of inflation for January of 2010 was 4.4% slightly above the 2009 rate of 4.1%. Brazil has not had a month with an overall contraction in the price level during the recession, reflecting the good behavior of consumption (private and public) and perhaps helping to stimulate production and investment.

The overall price level increased 0.9% during January of 2010 which is similar to the expansion observed during the fourth quarter of 2009. As inflation starts to increase Brazil faces similar policy choices than the rest of the world. It must exercise extreme caution in withdrawing fiscal and monetary stimuli in order not to avert an economic recovery while at the same time containing inflationary pressures.

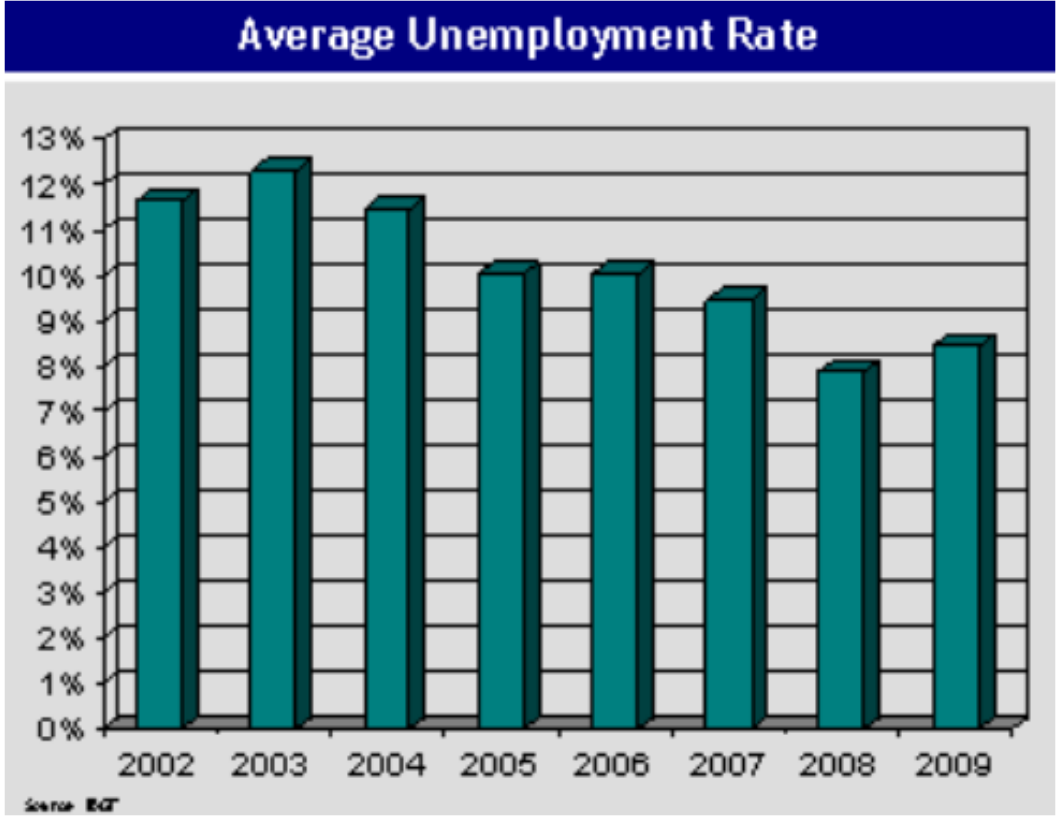

Unemployment

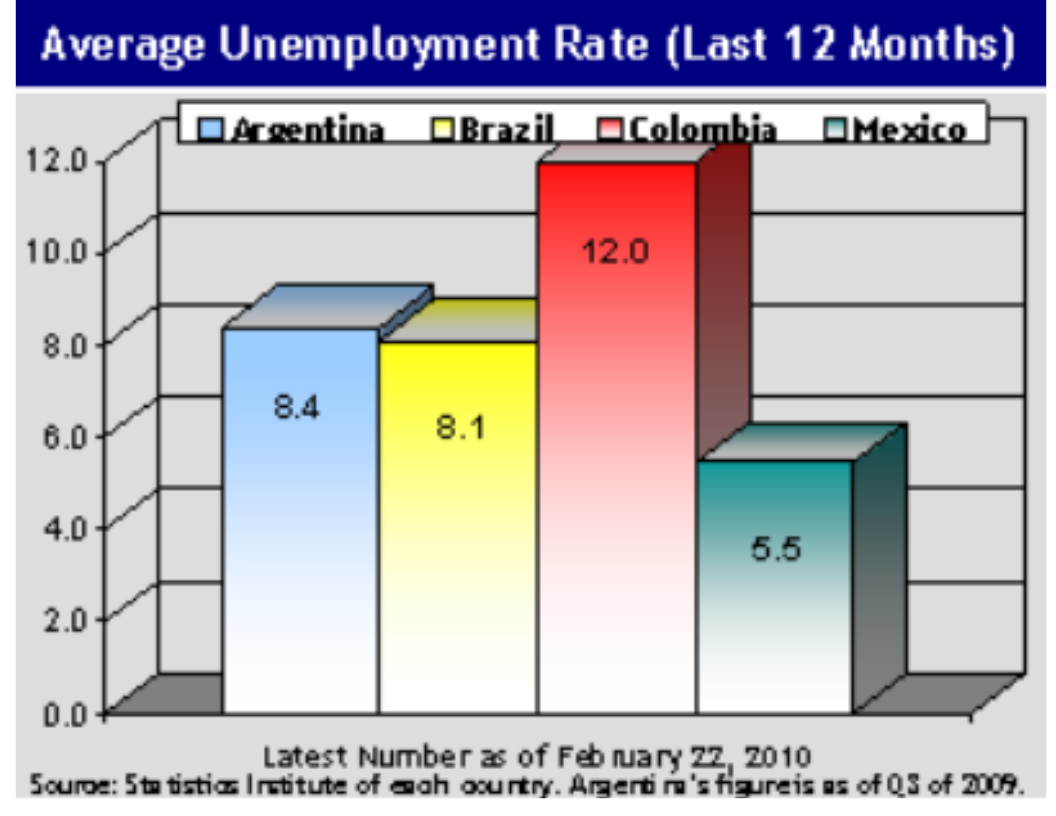

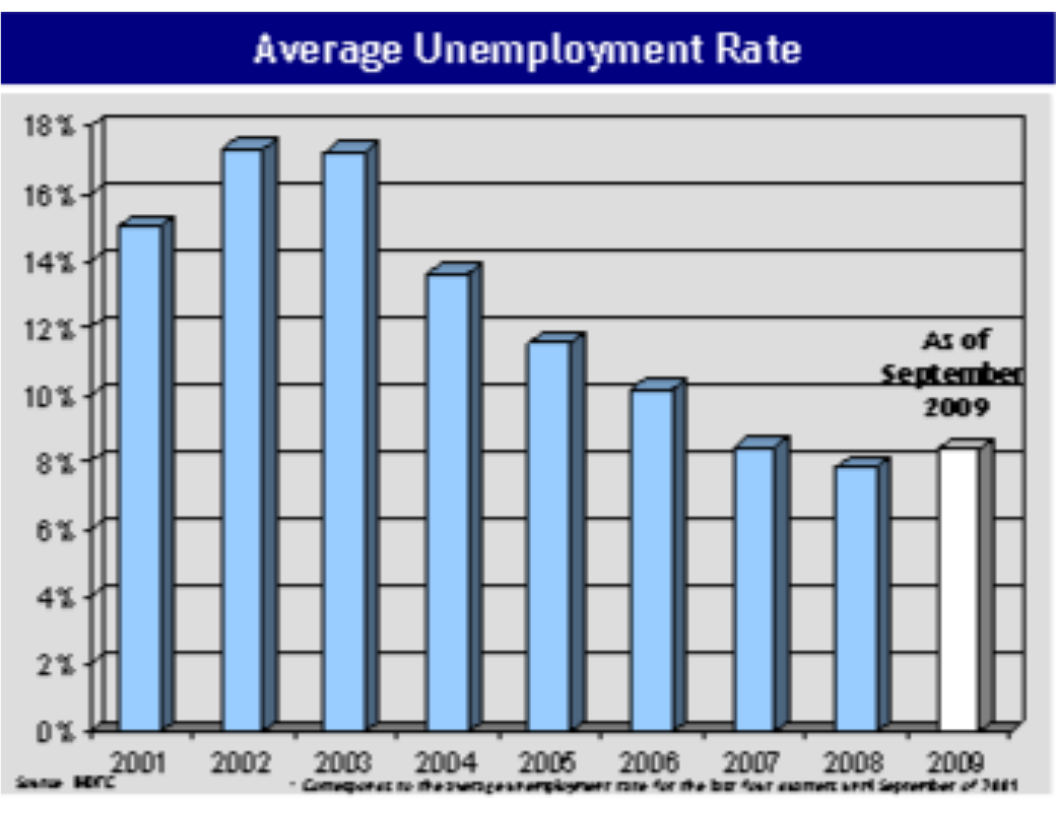

In fact, the average unemployment rate between the second quarter of 2007 and the same quarter of 2009 was 8.1% while the unemployment rate for the third quarter of 2009 has been reported at 9.1%, or 100 basis points higher. The slack in household consumption along with a deep decline in private investment and increasing unemployment make a strong recovery very doubtful. Unless the employment picture improves, it is unlikely that internal demand will strengthen enough for the emergence of a healthy economy over the next few years.

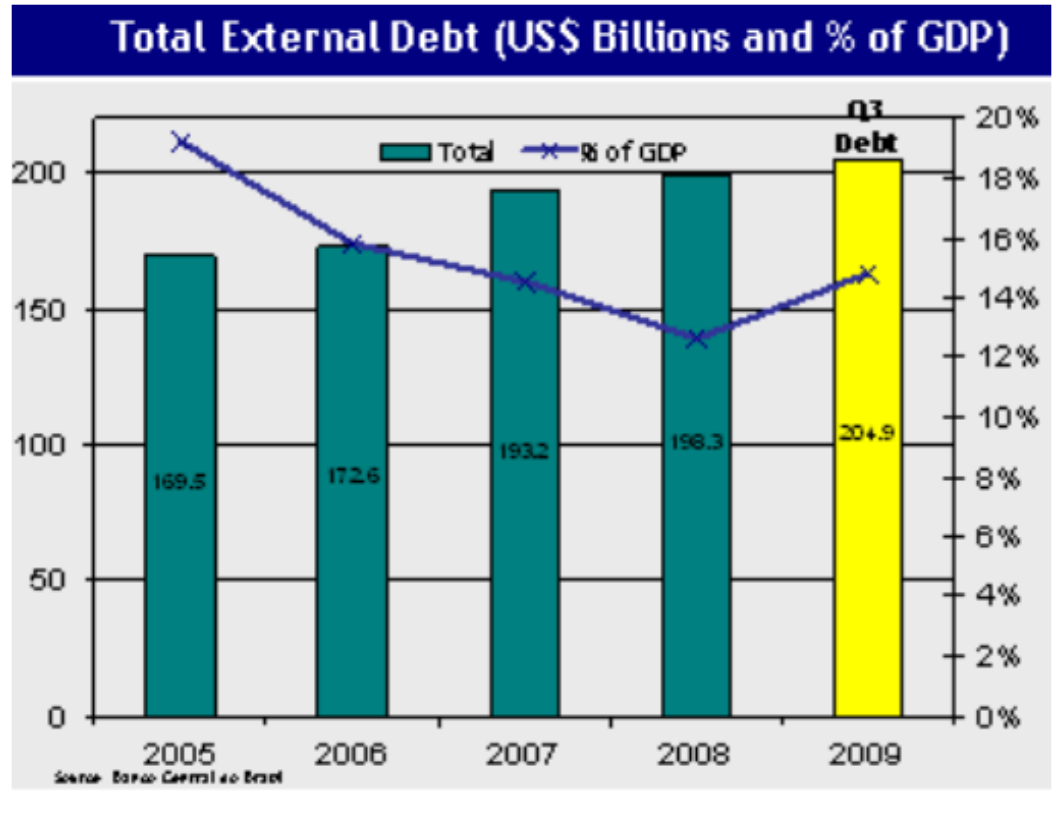

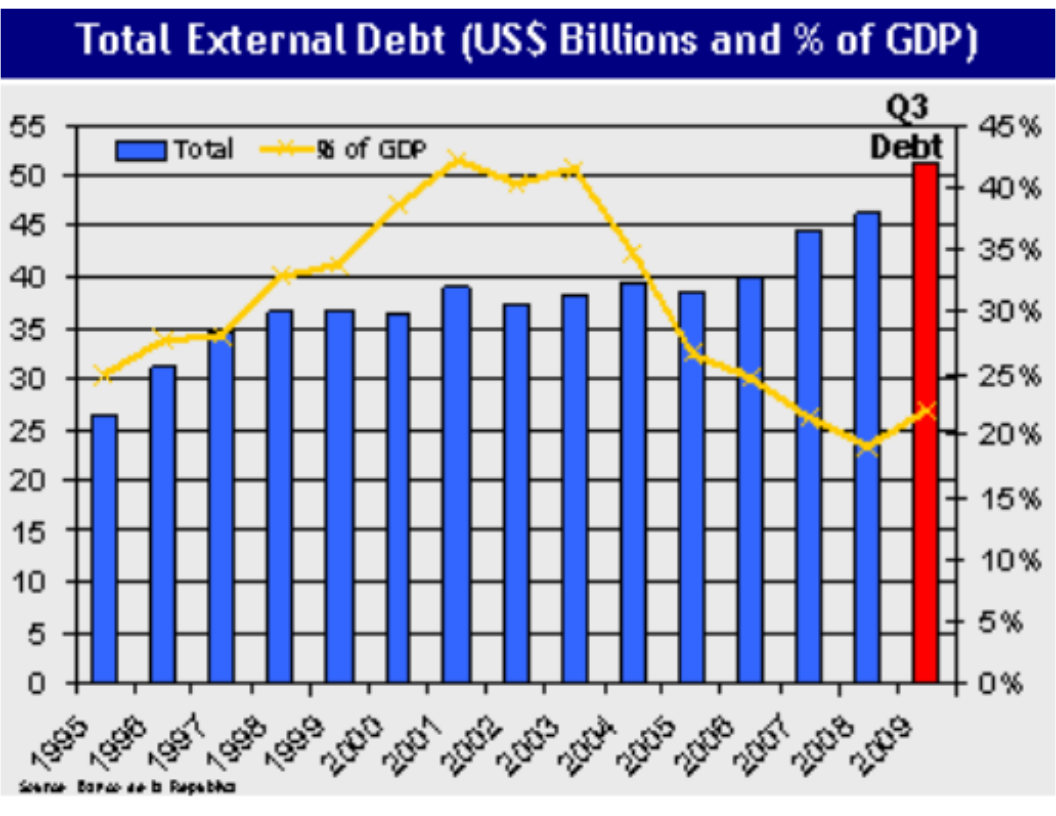

Debt Dynamics

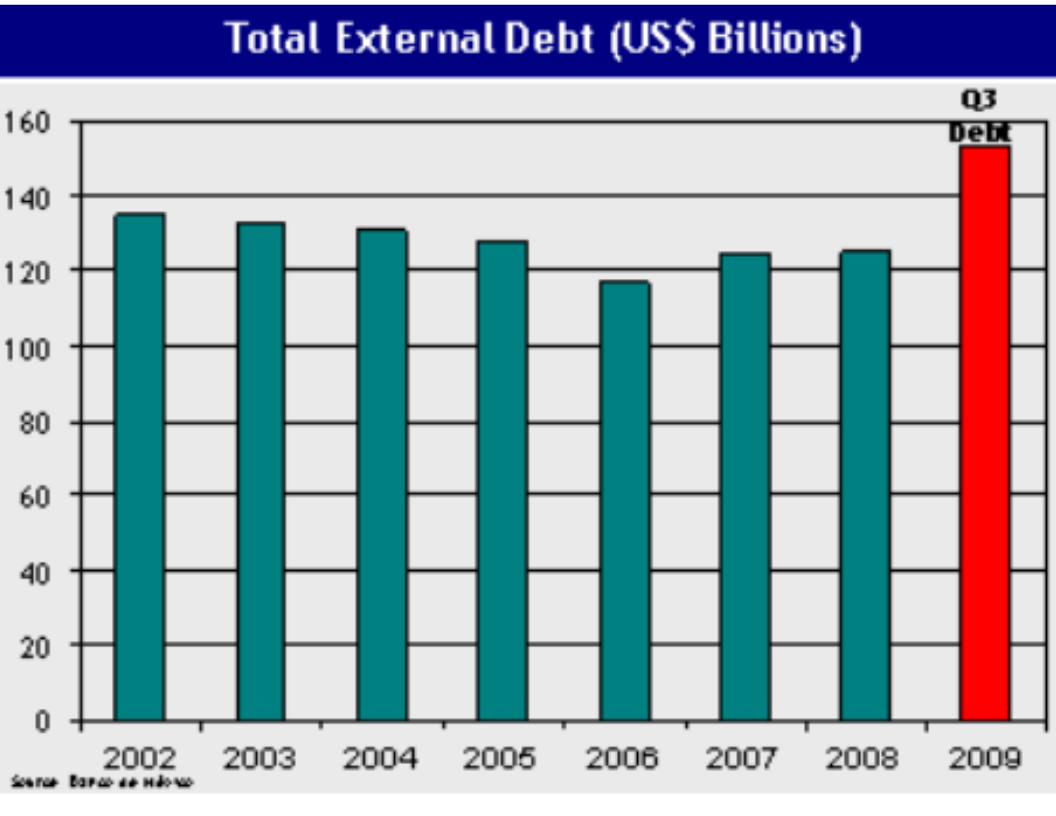

There is no doubt, that this rating increases overall financial costs and restricts credit, even more so, given the large expansion of the public sector. At the end of September of 2009 the external debt stock was US$123.8 billion, which was slightly lower than the US$124.4 billion reported at the end of 2008.

From the previous discussion some assertions can be made:

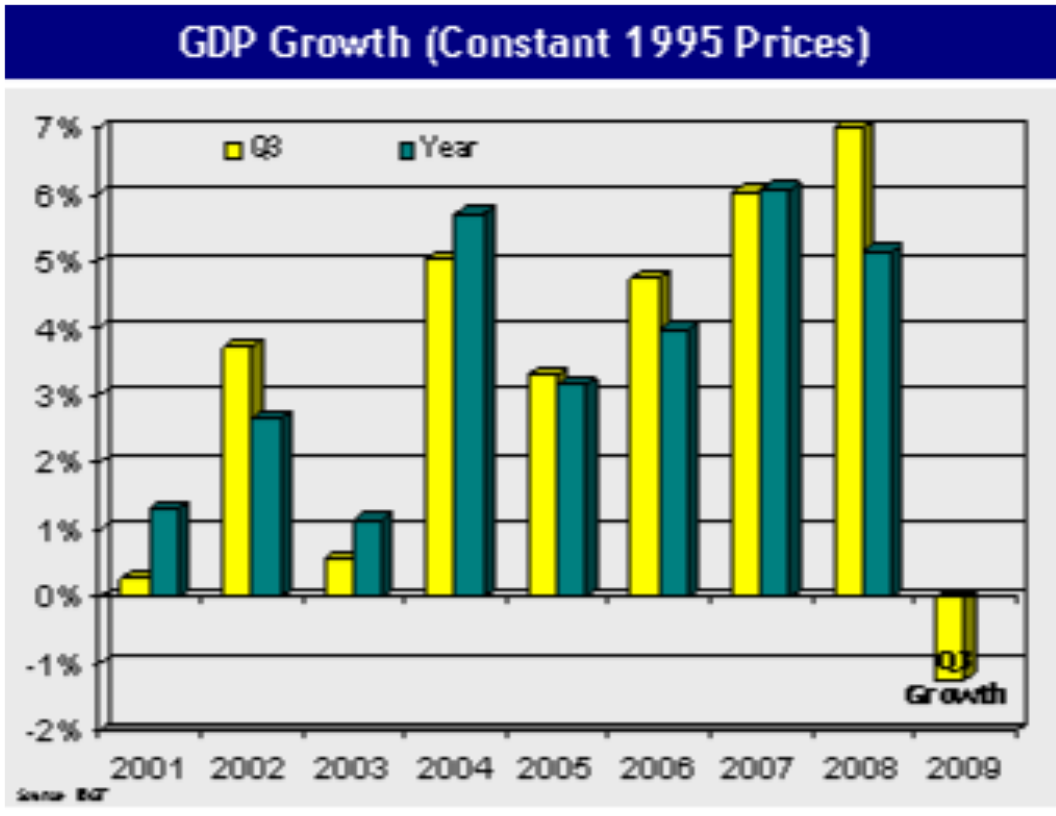

Brazil

Brazil has now posted the third consecutive quarter of negative GDP growth. Indeed, the rate is negative at -1.2% but it is less negative than the ones observed in the first and second quarters of 2009 of -2.1% and -1.6% respectively.

GDP Growth

The recession seems to be ending and probably fourth quarter GDP growth will be positive. However, it would take an extermely strong fourth quarter for overall 2009 GDP growth to be positive. Given the numbers for the first three quarters there would have to be an increase of 5% in fourth quarter GDP to be even for the year. A more likely scenario is a fourth quarter increase of between 1% and 2%, implying an overall GDP growth rate of close to -1% for 2009.

Brazil has approached the crisis more cautiously than other countries as public consumption has remained relatively under control. This however does not mean that fiscal deficits will remain stable since due to the recession government evenues have declined. On the other hand household consumption growth rates have remained positive all throughout the crisis. This makes Brazil, the economy with the best prospects for a sustained and smooth recovery.

Prices

The overall price level increased 0.9% during January of 2010 which is similar to the expansion observed during the fourth quarter of 2009. As inflation starts to increase Brazil faces similar policy choices than the rest of the world. It must exercise extreme caution in withdrawing fiscal and monetary stimuli in order not to avert an economic recovery while at the same time containing inflationary pressures.

Unemployment

Again, unemployment is a variable that shows how well Brazil has handled the international financial crisis and the recession. It is also a sign that the recovery may be faster and stronger than elsewhere in the region as household consumption can be maintained or increased.

Debt Dynamics

This is not a large amount when compared to the Colombian increase of US$4.8 billion for an economy of one sixth the size or the Mexican of US$28.7 billion. Given these facts, it is quite possible that rating agencies may be more open to improving farther the country's credit rating, thereby reducing funding costs for both the public and the private sector.

Colombia

GDP Growth

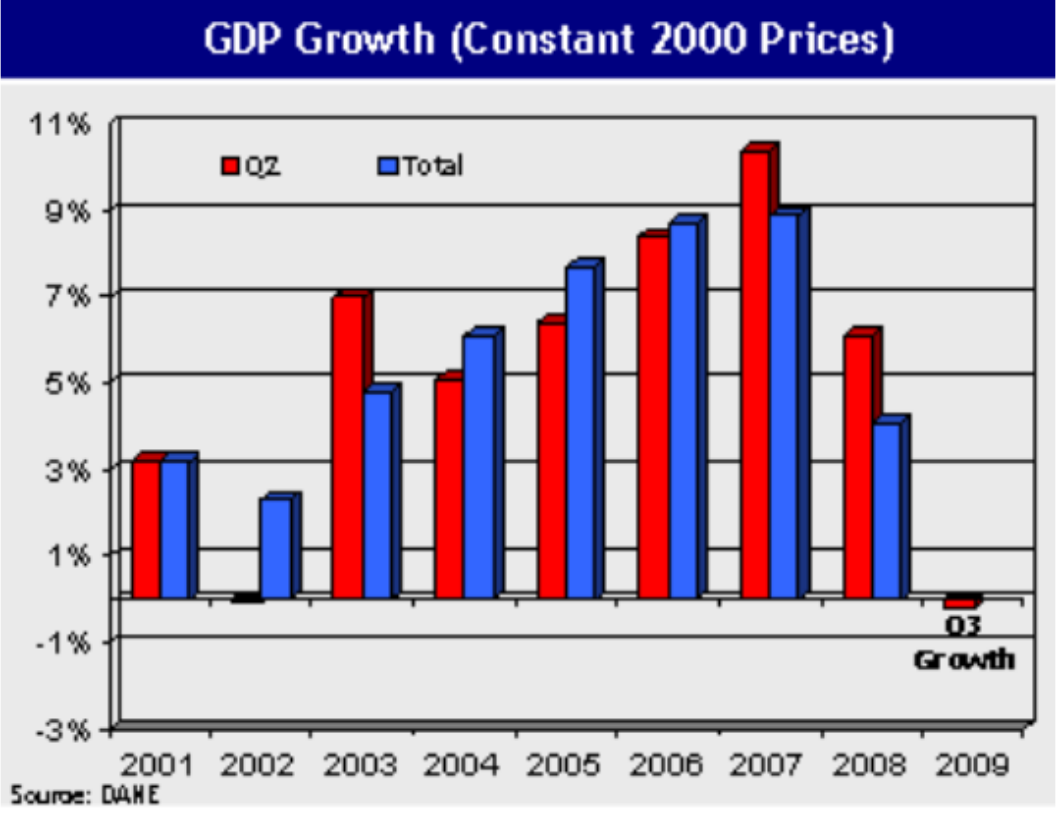

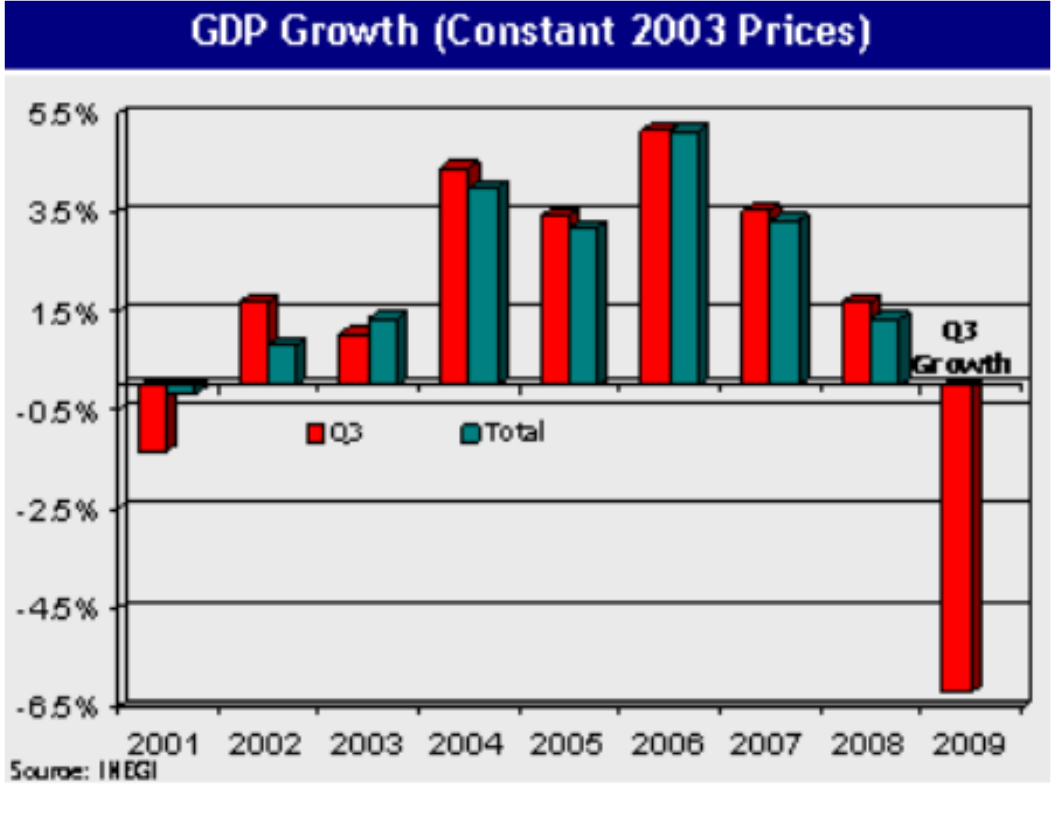

The Colombian economy decelerated significantly beginning in the first quarter of 2008 and started shrinking in the first quarter of 2009. Second quarter growth for 2009 is not yet known but it is possible that it will be negative again. Despite the severity of the global downturn it has not been as affected as other emerging economies.

GDP has not contracted much during the year. This means that if recovery indeed occurred in the last quarter of 2009, as our models are predicting, a small increase of 1% in GDP with respect to the same quarter of 2008 would leave GDP unchanged for the year in real terms. But our models are predicting that fourth quarter GDP growth was 2% which implies a small increase of close to 0.2% for the whole year.

To mitigate the effect of the recession, Colombia has also implemented an active fiscal policy. Government consumption has not severely increased but it has been enough to maintain total consumption from falling. Therefore, the decline in GDP has come more from a steep decline in investment that can affect future growth prospects. At the same time, if imports had not fallen as severely as they have, the GDP contraction would have been far greater. In other words, Colombia like the others, exhibits a major adjustment in the current account of the balance of payments during this crisis.

Prices

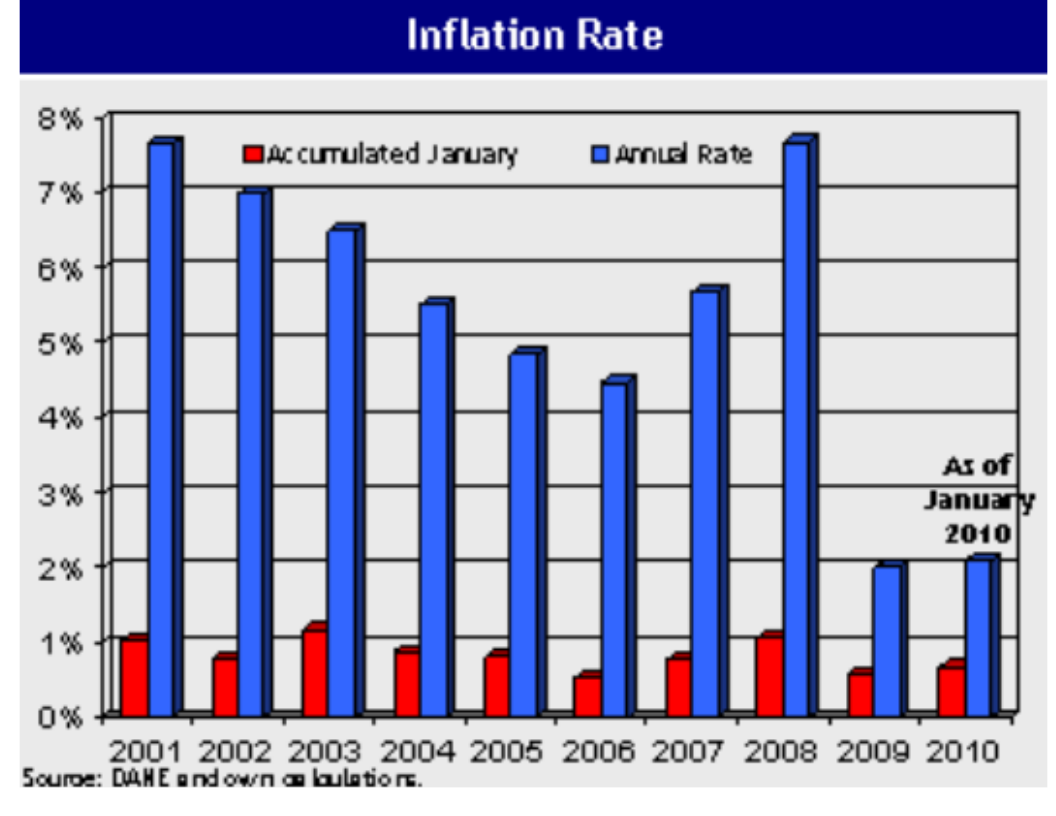

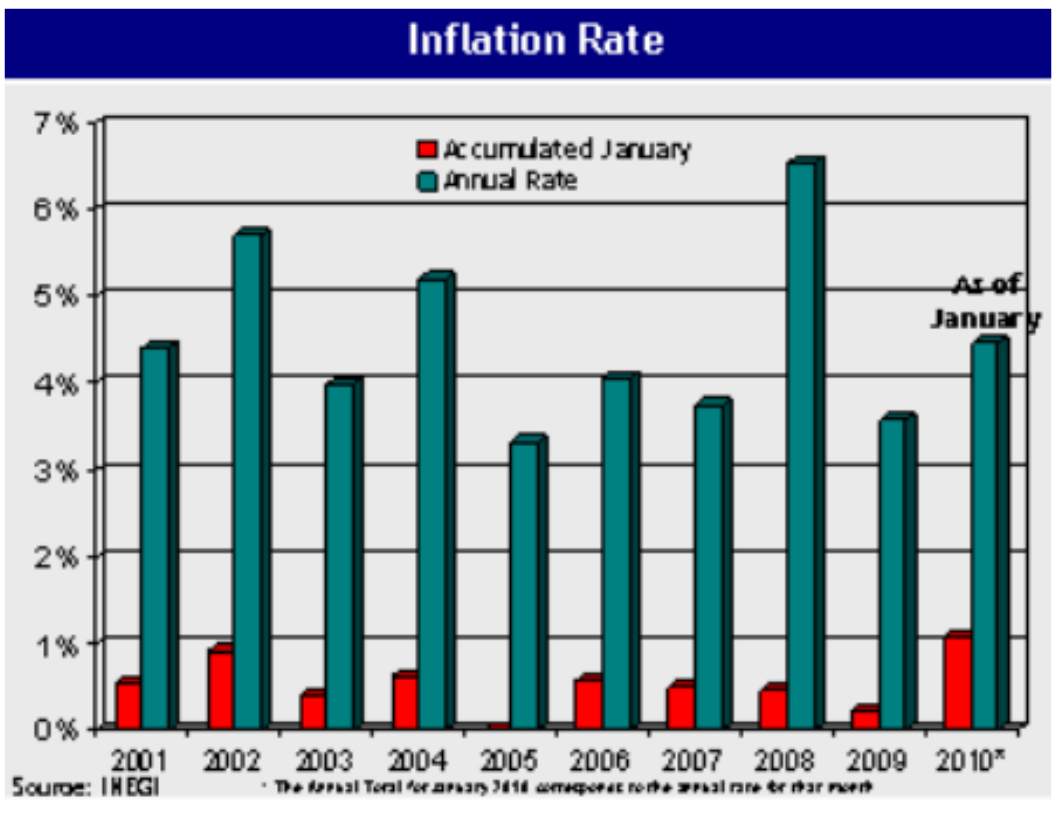

Of the four economies, Colombia shows the largest decline in the inflation rate moving from 7.67% in 2008 to 2.0% in 2009. Therefore, if one were to judge the severity of the recession by the decrease in the inflation rate, Colombia would have endured the severest one, with a drop of 567 basis points. This is hardly what could be called a “soft landing” from a period of unusually high rates of economic growth. Of course, Mexico also had a steep decline in inflation moving from 6.53% in 2008 to 3.57% in 2009 which is equivalent to 296 basis points or close to half of the Colombian reduction.

Labor Market

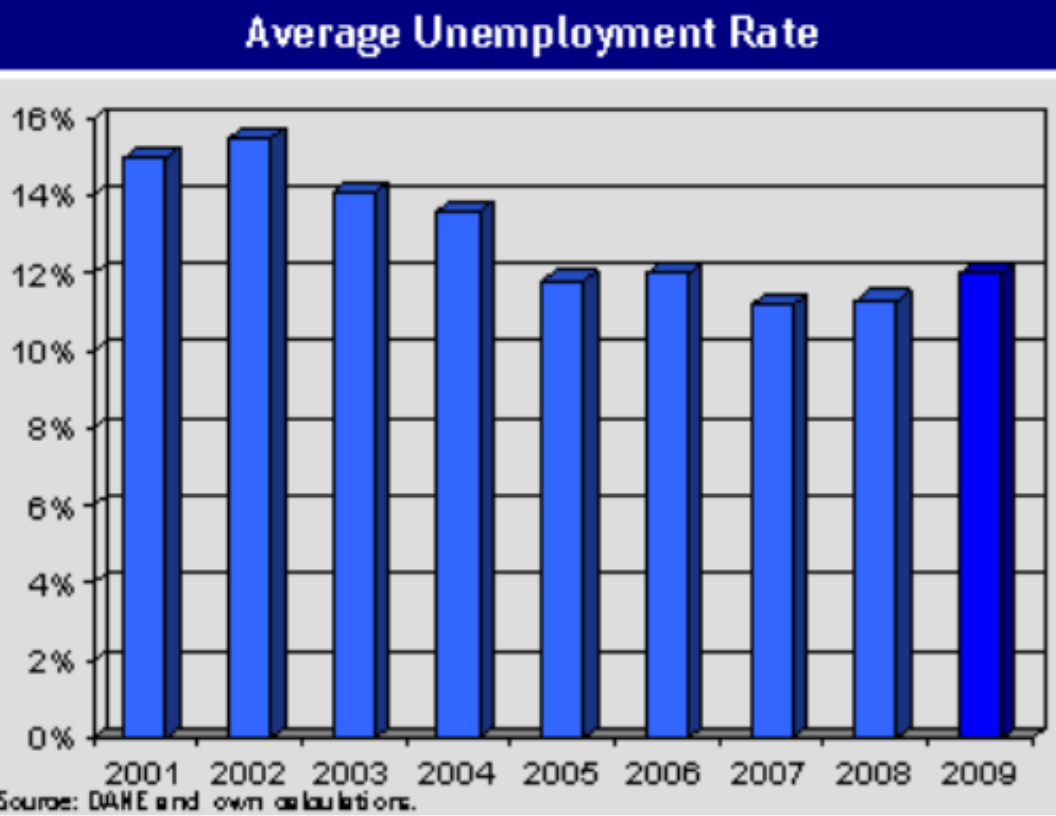

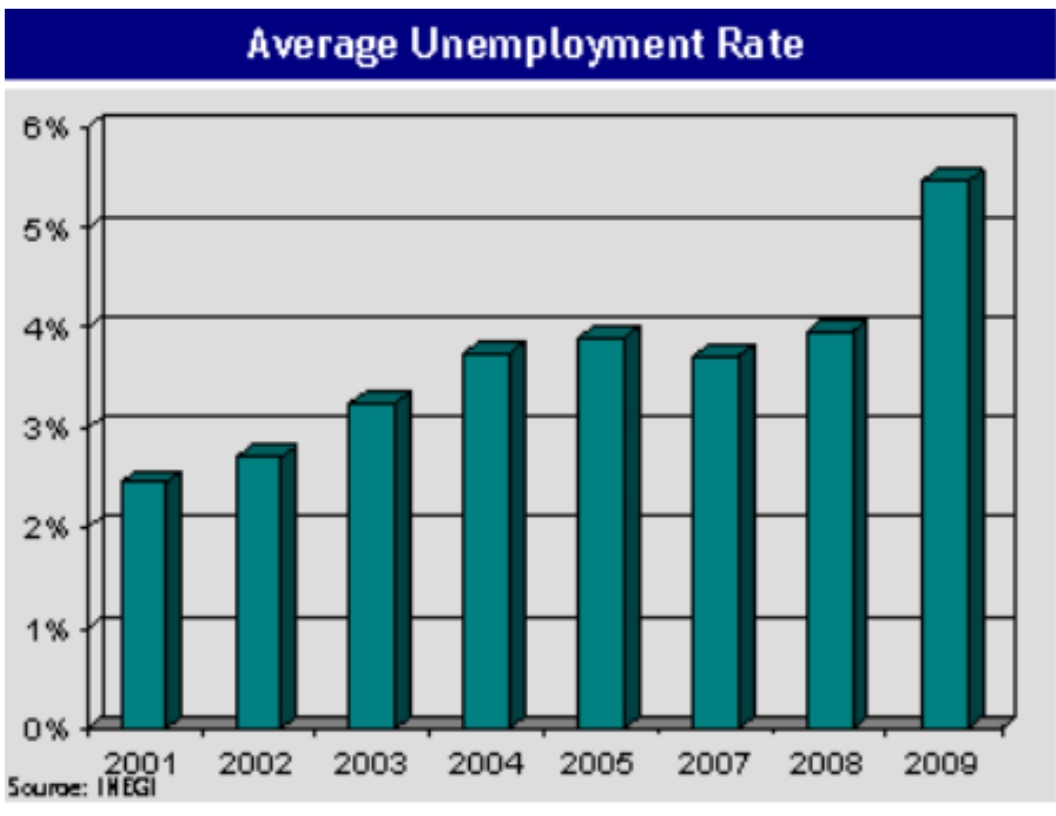

Due to the recession, household income has declined pushing the participation rate towards historical highs. The problem is that in the past, when the participation rate has been close to 63%, the unemployment rate has risen to levels above 14%. Indeed, the average participation rate over the decade has been 60.8% and in December of 2009 reached 62.6% for the month and 61.3% for the yearly average. Consequently, it seems certain that the unemployment rate will continue increasing up to levels of close to 14%. As has been amply discussed, high unemployment rates in Colombia pose a great threat to social and economic stability given the severe income inequality of the country and the lack of a social safety net and of automatic stabilizers such as unemployment insurance.

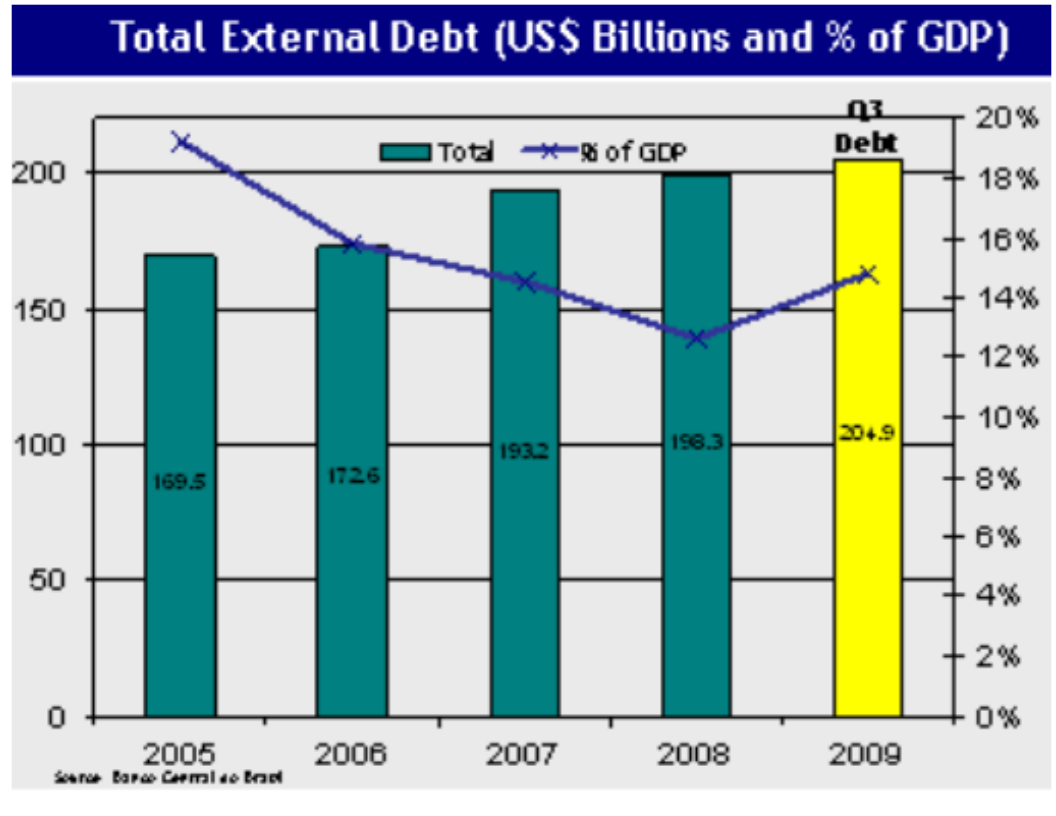

Debt Dynamics

Even though, government consumption has not increased like in Argentina or Mexico, judging by the public debt figures the fiscal deficit must have surged. Undeniably, as a result of the recession government revenues severely fell exacerbating the fiscal imbalance. What is of even greater concern is the fiscal picture for 2010 when income tax revenue will surely report a steep drop.

Also, the added debt burden in an environment where interest rates will be on the increase is going to have an adverse impact on fiscal and debt sustainability. Even at current interest rates an increase in external debt of that magnitude is going to permanently add $0.7 trillion pesos to the fiscal eficit at current exchange rates. Additionally, this increases exchange rate risk, something that over the past several years was on the decline. On the other hand, internal debt has also suffered a large increase. Indeed, it is the second largest in history with $16.9 trillion pesos and at current interest rates implies a permanent addition to the fiscal deficit of $2.2 trillion pesos in interest payments. Overall the increase in internal and external debt implies a permanent addition to the central government deficit equivalent to 0.5% of GDP according to the forecasts at Newnube.com.

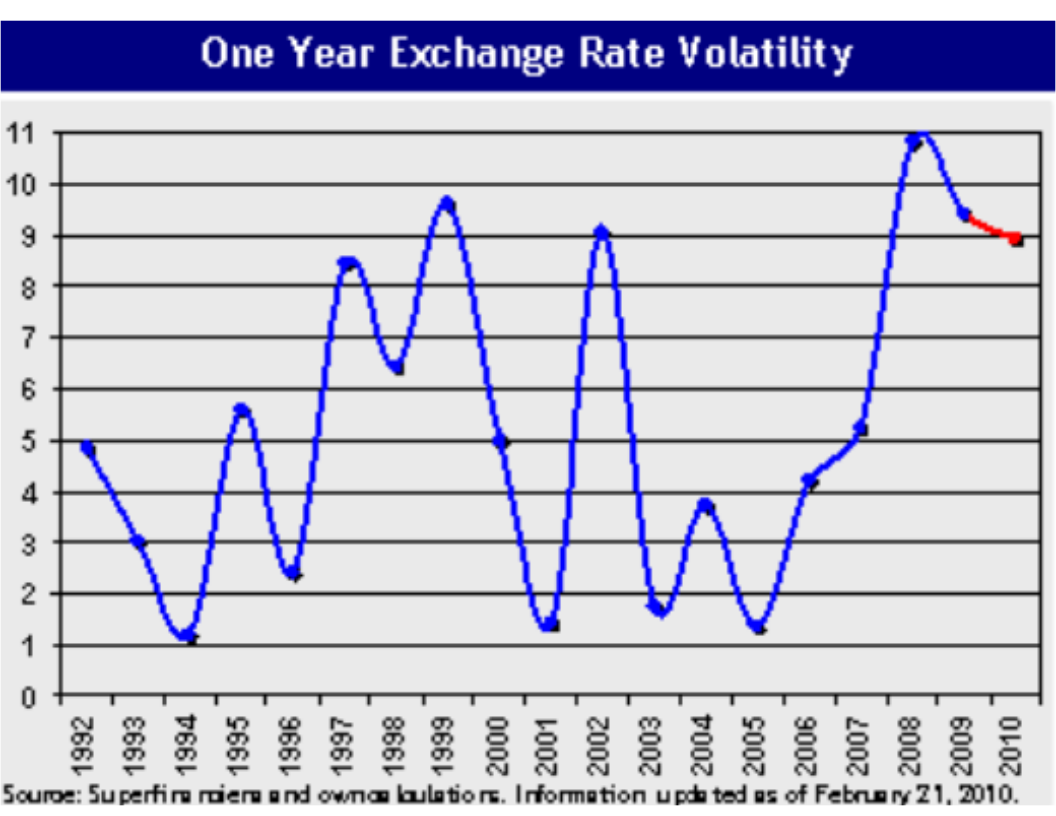

Volatility

2008 was a record year in terms of volatility and it has declined since then to the current level. Nonetheless, 2010 should be a very volatile year and indeed could break 2008's record. Most of the uncertainty will come from an unstable political situation. In the first half of the year the political future of the current's President third term in office will be decided. To remain in office he will have to overcome many legal hurdles, including a constitutional change. If he is able to become a candidate there will be instability as he is questioned and challenged by political opponents and as the results of the election are an open game. If he is not able to become a candidate, which is very doubtful, a tighter race for the presidency may develop an volatility will shoot up. Given that he is reelected to a third term, there will be some discontent and a fragile democracy may be further weakened as the country's framework of checks and balances, constitutionally designed for a single presidential period, deteriorates even more. In case he is not reelected, then uncertainty will be extremely high as the country does not know much about what to expect from a new President. As a result, whether the current President is reelected or not, volatility is bound to increase from a political perspective. Economically, the news will not help to reduce volatility as the fiscal deficit increases and as companies start to report on a dismal 2009.

Therefore, for Colombia 2010, although better than 2009, presents serious challenges and risks from an economic management perspective:

Macroeconomic Model -Colombia-

Forecasts

In the last issue of Trends a compact macroeconomic model (CMM) was introduced. The model was a Gross National Income Model (Y) and it performed rather well with respect on the third quarter of 2009. While actual Y growth for that quarter was -1.9% the model had forecasted a contraction of -2.5%. Now net exports have been added so the model is able to handle GDP. It is important to note that the new CMM still is stochastic and uses a Montecarlo approach in finding solutions and expected values by running 50,000 iterations. Even though expected values are derived in this fashion a much more meaningful quantification are the consistent confidence intervals, as will be shown later.

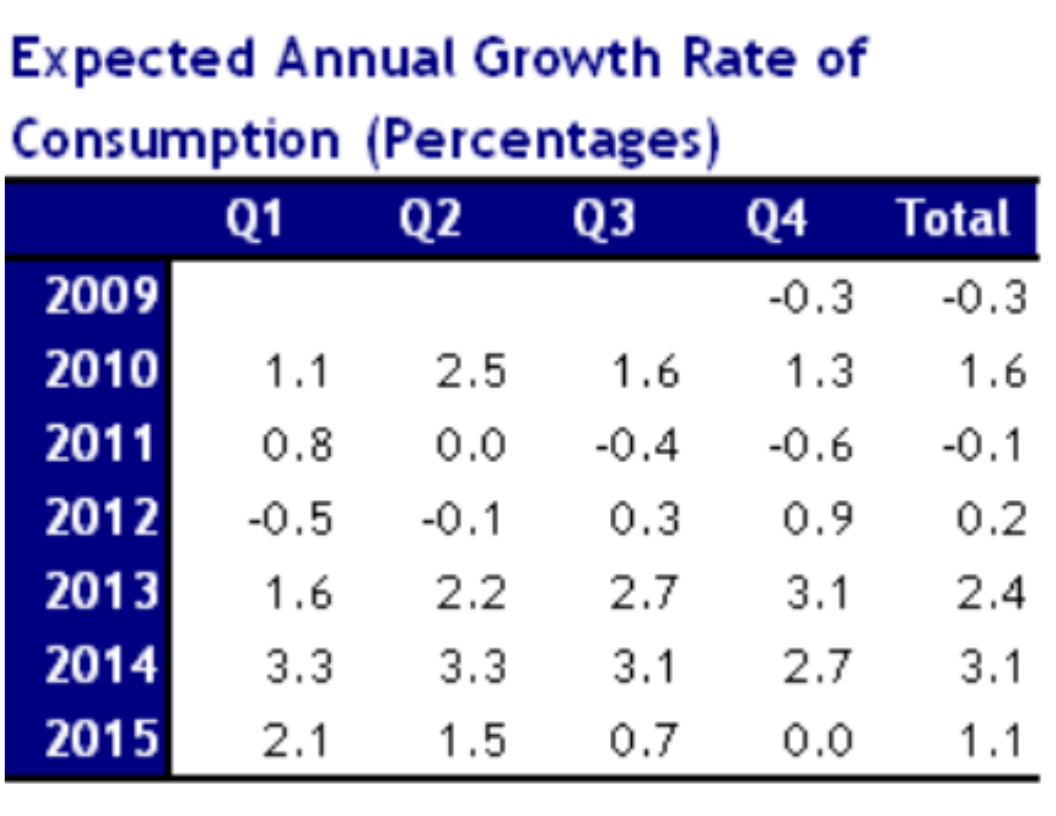

It seems that as long as household consumption does not recover the prospects for GDP and GNI growth will remain bleak. That is why the unemployment problem poses a severe risk to the incipient economic recovery. Indeed according to the CMM household consumption will grow in 2010 by 1.6% allowing for GDP to expand.

Unless a more balanced economic model is implemented in Colombia the country will continue to suffer from recurrent recessions. The development of a vibrant middle class is essential to economic prosperity, social stability and lower volatility. The high rate of unemployment is complemented by an extremely unequal income distribution which is among the top ten worst ones in the world.

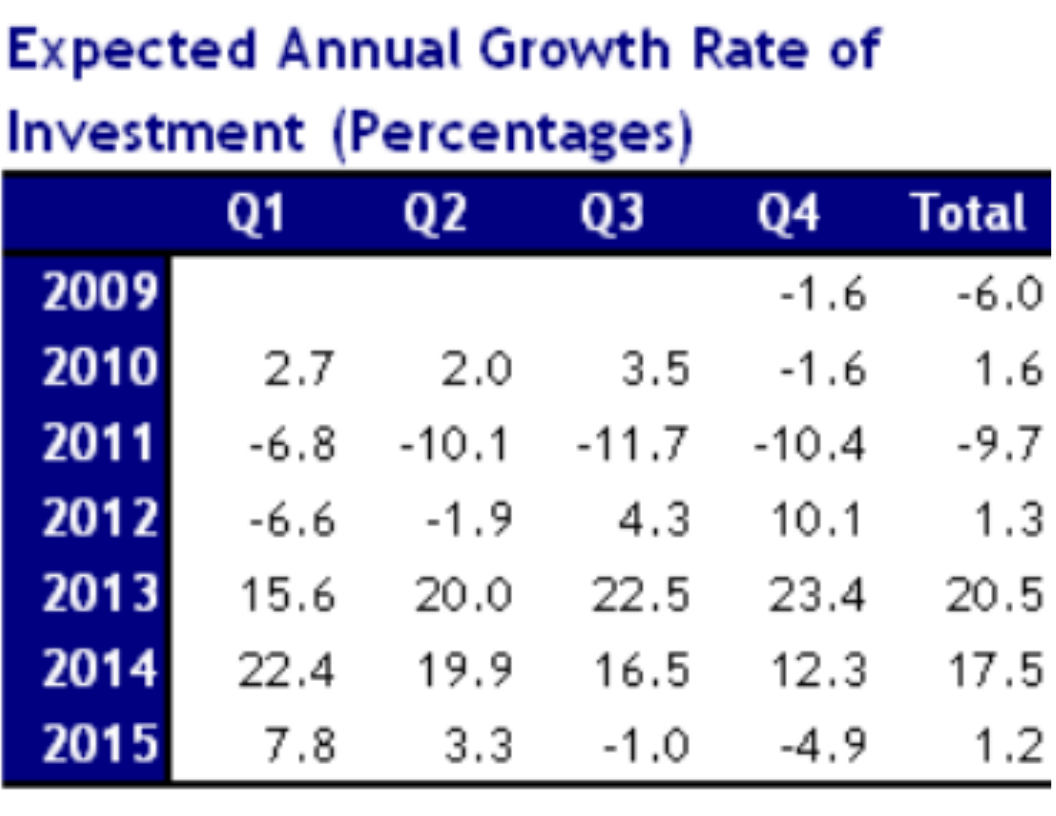

Investment is a very volatile variable, similar to net exports, and to rely exclusively on it for economic growth is, to say the least, an economic policy blunder. Once again, it is necessary to stress that Colombia must to do something to change the bias in favor of investment that has developed over the past few years whereby capital has many advantages over labor expenditures.

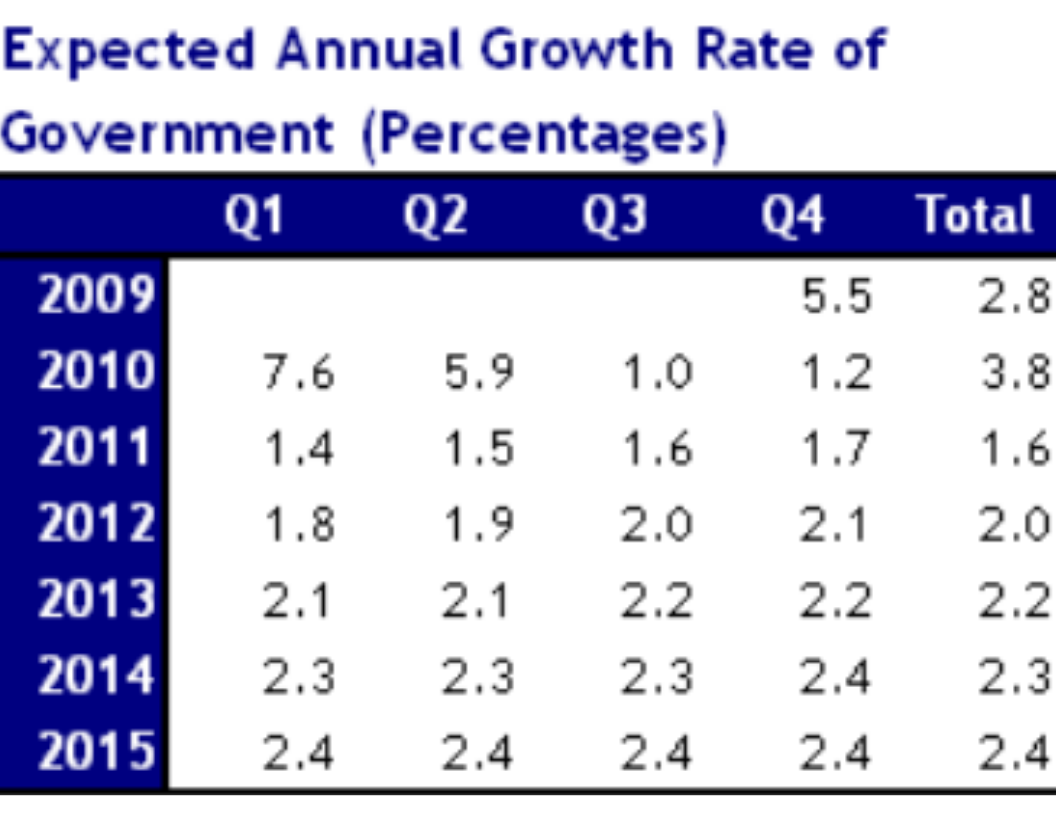

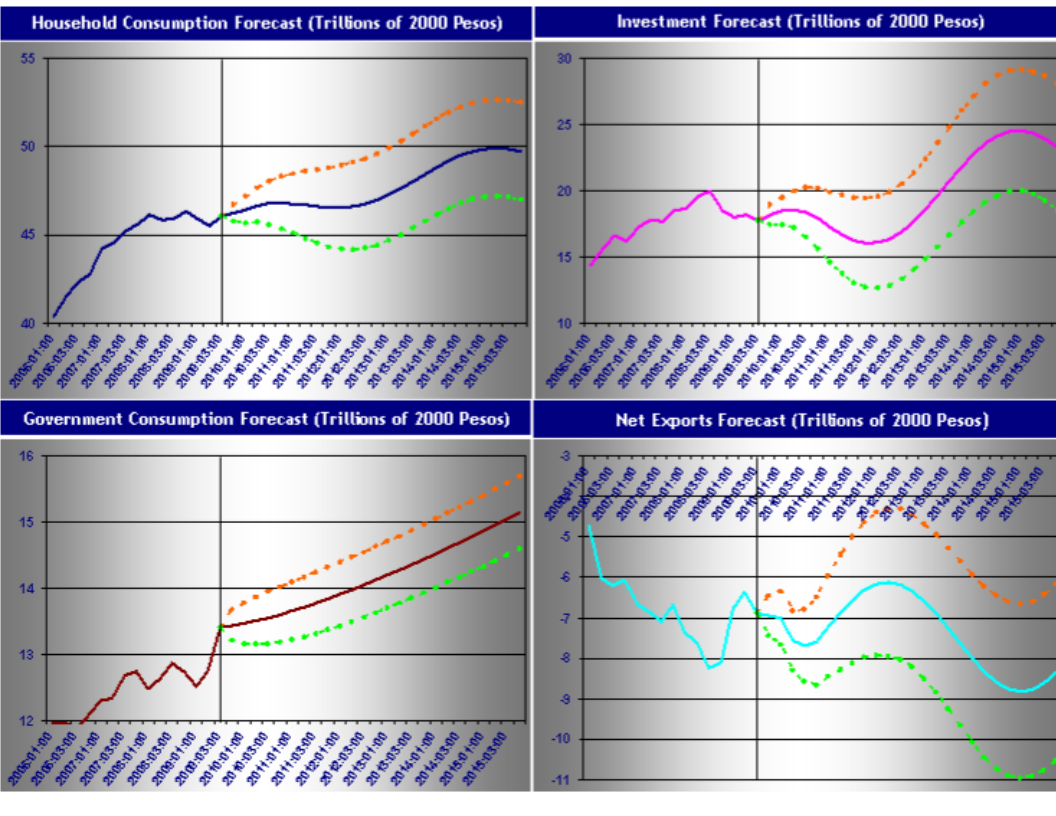

As the recession deepened over 2009, government consumption has gained momentum and it is expected to increase by 5.5% in the fourth quarter of 2009, reaching an annual rate of 2.8% for the whole year. The rate will still be very high in the first and second quarters of 2010 but there will be an adjustment in the third and fourth quarters to reach 3.8% for the year. Without a doubt, the government will find it difficult to contain the thrust of public expenditures after launching an aggressive effort to tame the recession.

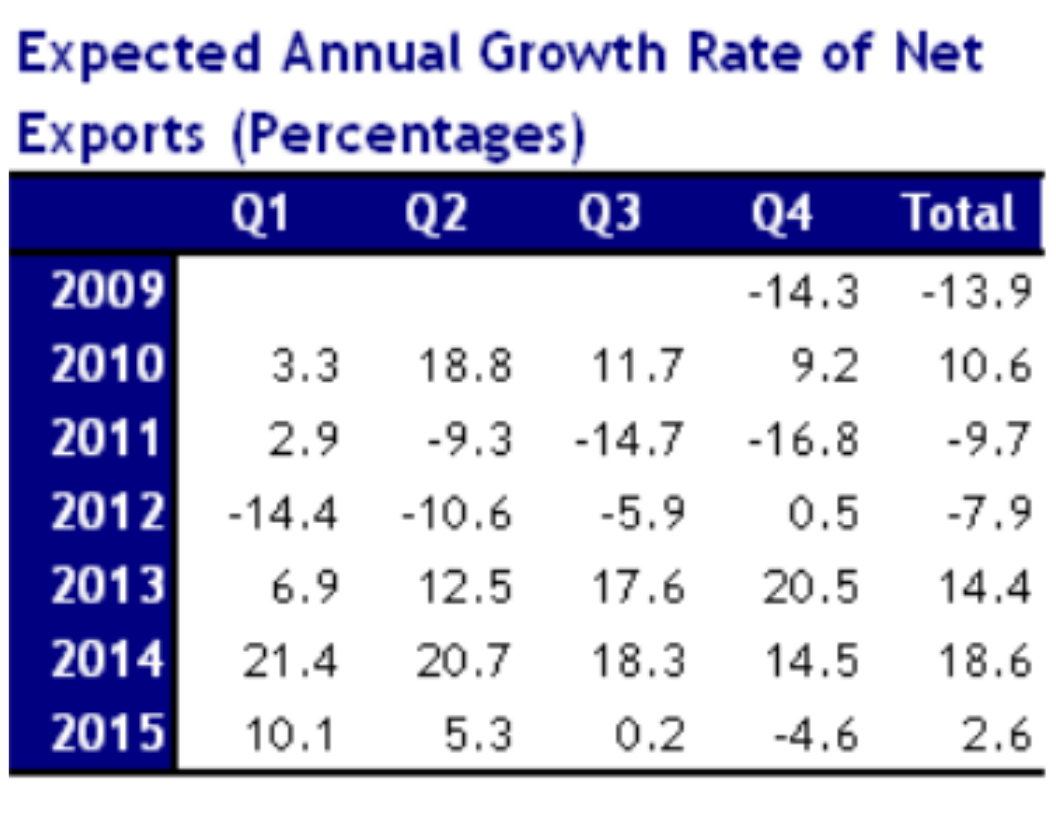

Also the interpretation of their growth rates, as shown in the table, is difficult since a negative rate does not mean a deterioration of the variable but quite the opposite. For example, the 13.9% annual decline for 2009 is actually an improvement in the trade deficit as imports declined faster than exports. In other words, what the decline means is that the trade deficit in 2009 will be smaller than in 2008 as forecasted by the model. Thus, the projection is that for 2010 there will be again an increase in the trade deficit as imports are reactivated due to the recovery.

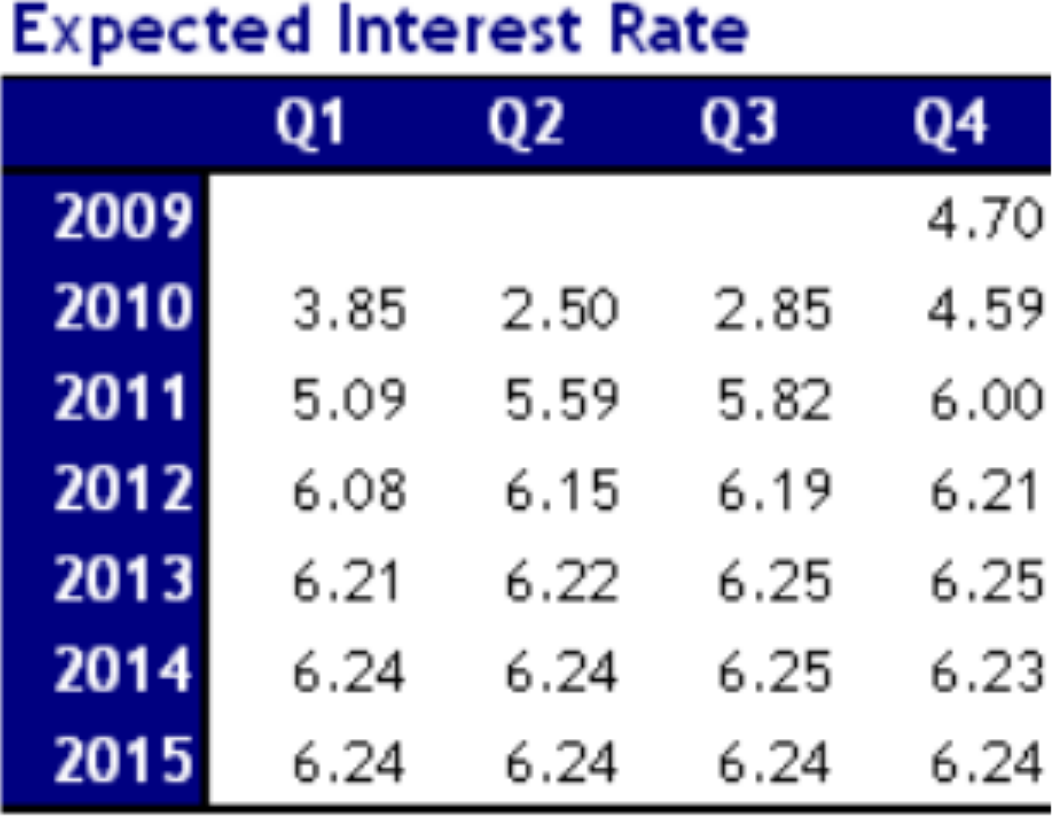

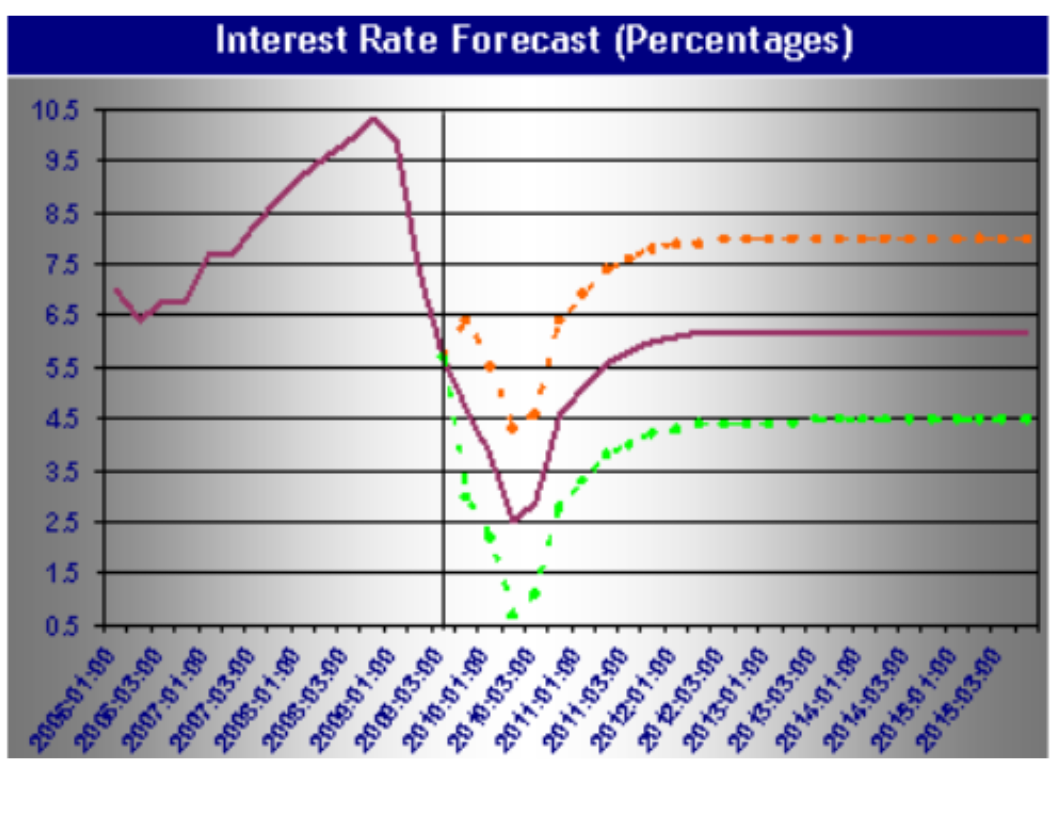

The table shows the expected values of the 360 day CD rate between the fourth quarter of 2009 and the same quarter of 2015. The rate is expected to remain below 5% during 2010 and then continually increase until it reaches 6.2% where it will stabilize. From a historical perspective this is a relatively low rate, but inflation has also declined significantly. Then, as long as inflation remains under control at its current level, or even somewhat higher, the forecast seems reasonable.

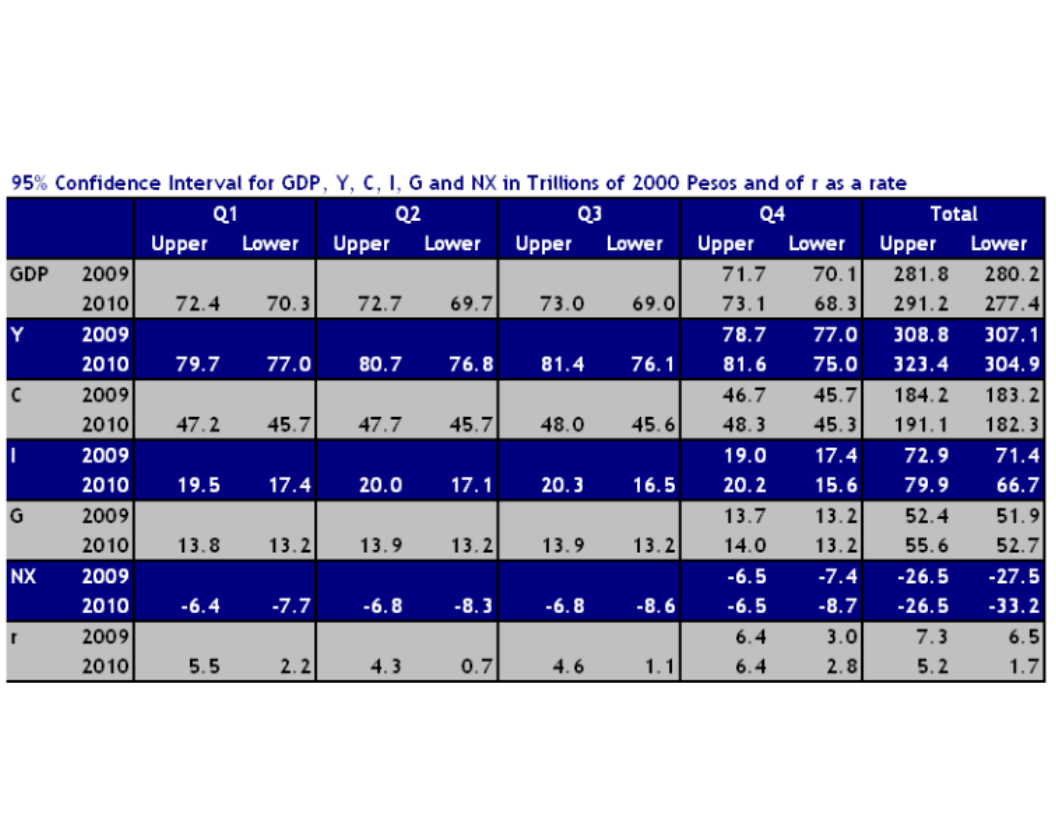

Confidence Intervals

The same principle applies to each of the endogenous variables of the model which are Gross Domestic Product (GDP), Gross National Income (Y), Household Consumption (C), Investment (I), Government Consumption (G), Net Exports and the Interest Rate(r). For example, in 2010 the average interest rate is forecasted to be between 1.7% and 5.2%.

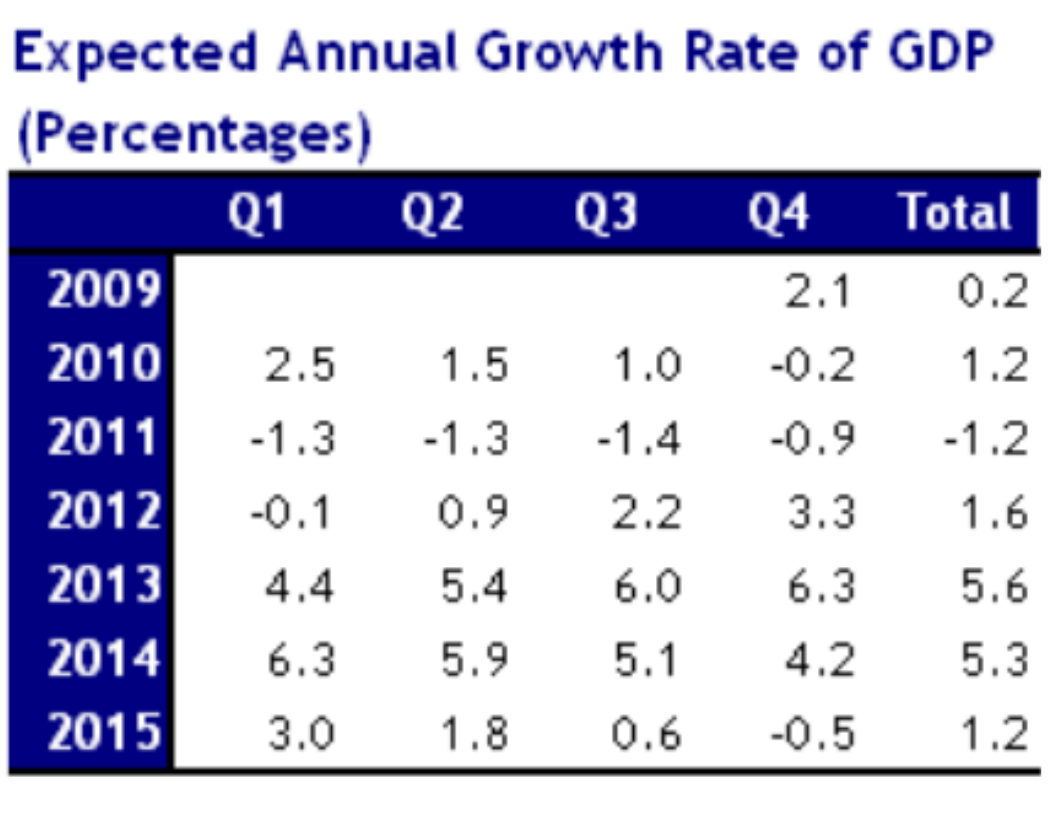

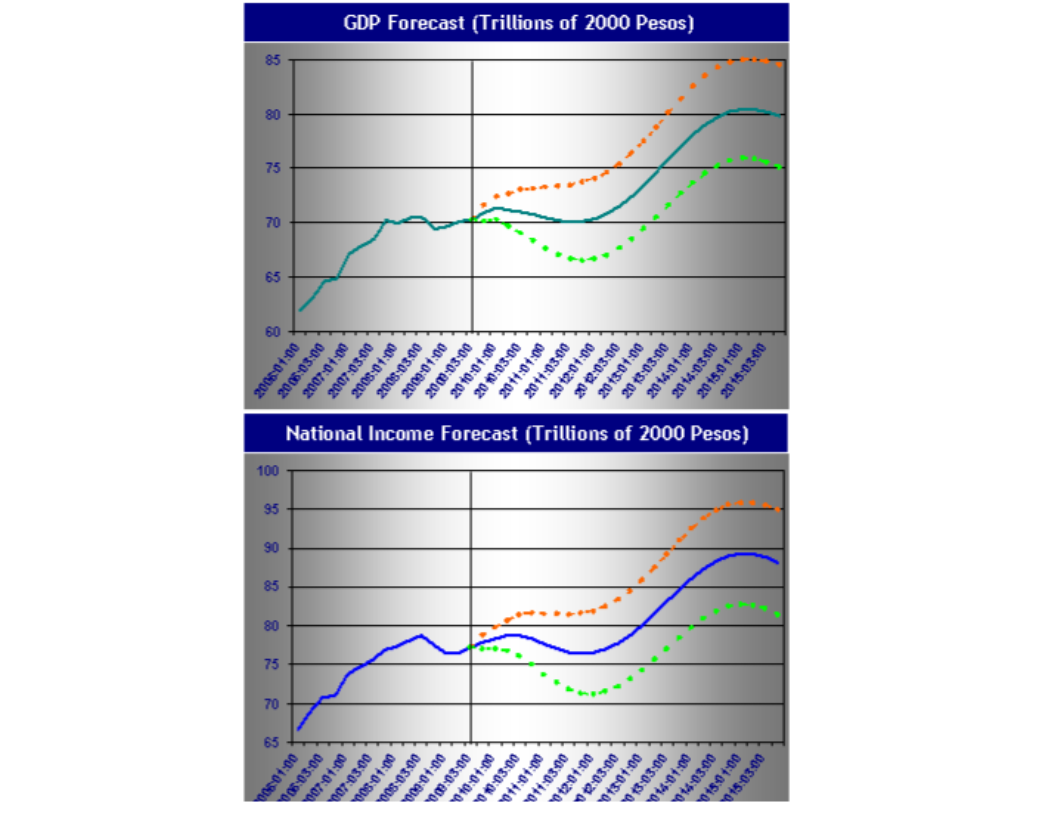

The graphs show the expected value of the forecast in the solid line along with the upper bound (orange dotted line) and lower bound (green dotted line) of a 95% confidence interval. For example, as was seen on the table, in the fourth quarter of 2010, GDP will be between $68.3 and $73.1 trillion pesos at 2000 constant prices while for the year will be between $277.4 and $291.2 trillion. This implies that GDP growth in 2010 will be between -1.0% and 3.4% with a probability of 95%.

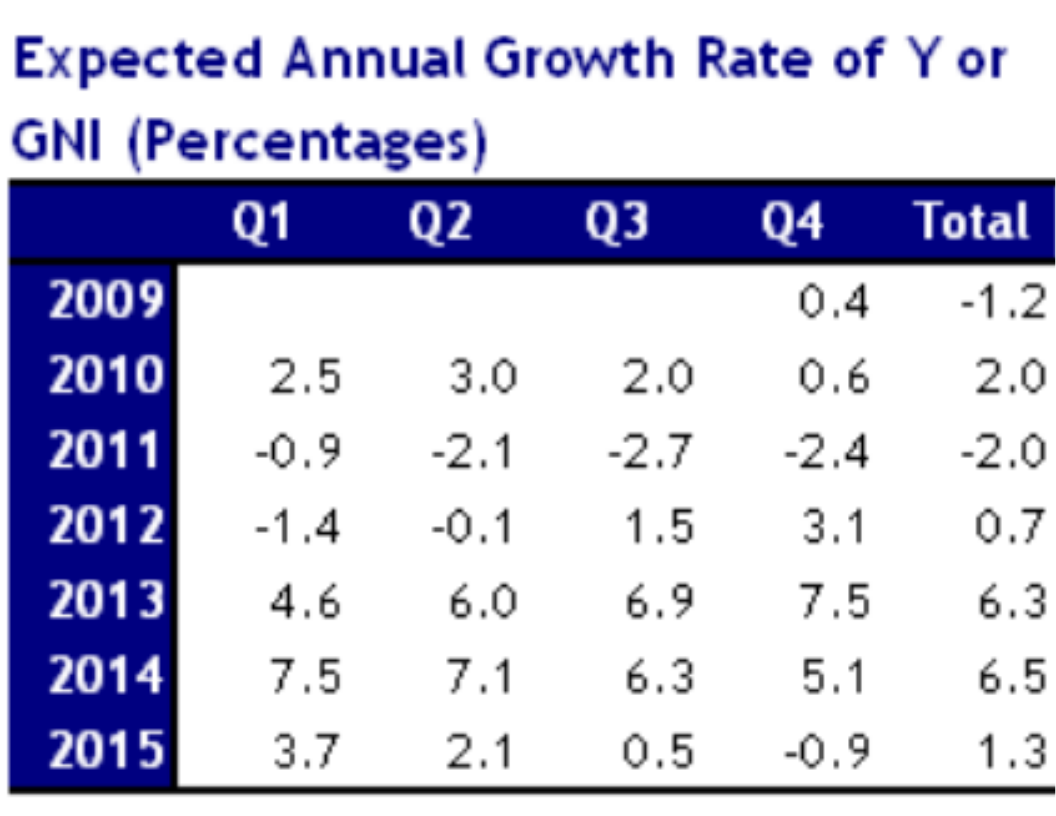

Gross National Income (bottom panel) behaves very similar to GDP. However, the impact of the forecasted recession is accentuated on this variable.

Nonetheless, as can be seen in the GDP graph there may not necessarily be a recession in 2011, given that the upper bound of the confidence interval (dotted orange line) still forecasts positive GDP growth. In other words, at this point the model does not forecast a recession with 95% confidence although on average a recession can be expected in 2011.

On the other hand, investment and net exports show large variations. For example, investment initially recovers in 2010 and then shows a large contraction in 2011 being the major cause of the forecasted recession. Net exports show the opposite behavior, when the economy and investment decline, net exports increase. This makes economic sense. As the economy contracts imports decline faster than exports because of two factors: First, a recession causes a decline in household income so people demand less consumer imports.

Second, the decline in income forces business to invest less thereby requiring a smaller amount of capital equipment imports.

It is clear that a small change in household consumption brings about large changes in GDP affecting also investment and net exports. The point made previously, that unless the employment picture improves, this economy is vulnerable to sluggish economic growth becomes all the more evident.

However, as the economy recovers during 2010, inflation and the interest rate will be under pressure to increase. The model forecasts a stable interest rate after 2010.

The important point of the graphical analysis is to see how the variables will move within a given range for a certain period with a probability of 95%.

Mexico

GDP Growth

Although, the worst of the recession seems to be meandering away, as the GDP contraction is slowing from annual rates of -7.9% and -10.1% in the first and second quarters of 2009 to -6.2% in the third quarter, the overall contraction for the year will be significant. Even if GDP were to expand at an annual average rate of 5% during the fourth quarter, the contraction with respect to 2008 would still be -4.6%. A more likely outcome is an overall 2009 contraction between -5.0% and -5.8%, assuming that Mexico overcame the recession on the fourth quarter.

As well as in the other countries there has been a large adjustment in the current account of the Balance of Payments as imports have fallen at much higher rates than exports. As a consequence, again we have an example where the contraction in GNI has been much larger than the one for GDP. Fiscal policy has been centered on aggressively expanding public investment as public consumption has expanded at trend rates. With the fall in imports and a large contraction in private consumption, the average consumer has been severely affected by the recession.

Prices

However, the annual inflation rate is still within the average for the decade of 4.5%. Although, the authorities may be somewhat concerned about the trend it pales in comparison to the much bigger GDP growth problem. Here again there is a policy dilemma as to how to unwind fiscal and monetary stimuli without aborting an economic recovery.

Unemployment

Definitely, unemployment may evolve into a chronic problem thereby negatively affecting other social indicators such as income distribution. The unemployment rate in Mexico has remained below 7% since the mid 1990's and hopefully it will not surpass this level in the near future.

Debt Dynamics

It means the public sector is crowding out private external credit and investment. Of course in the absence of private investment the government has tried to fill part of the void. What this means for the future is yet unclear. It will depend on how productive public investment projects undertaken during the recession turn out to be.

Of the largest economies in Latin America, Mexico is the one that has suffered the most during the current crisis and recession. The consequences are still uncertain but some general conclusions may be drawn:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}