Economic Trends -Latin America-

Trends is a quarterly online Newsletter

intended to inform readers about the

ensuing developments in some Latin

American economies. The global

recession has affected Latin America in

varying degrees, from Mexico where it

has been quite severe to Argentina and

Colombia where it has not been as hard

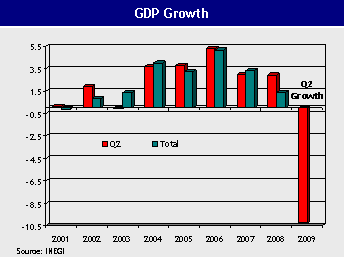

felt. There is no doubt that 2009 will

end up being one of the worst years of

the current decade for Latin America.

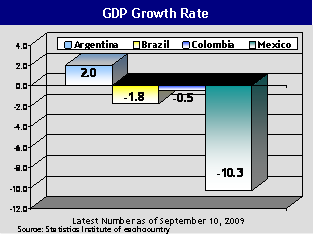

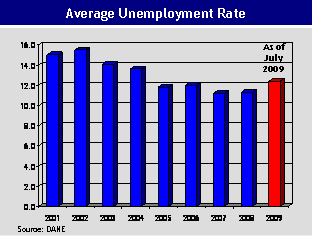

As the graph shows the largest

economies in the region are already

showing signs that there may be a

recession in the making.

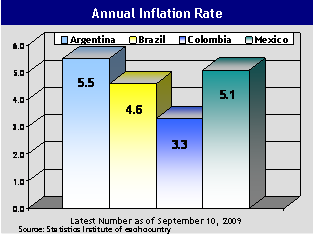

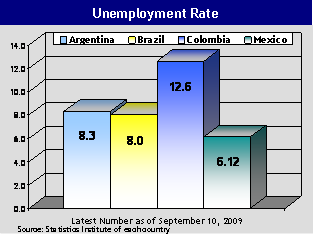

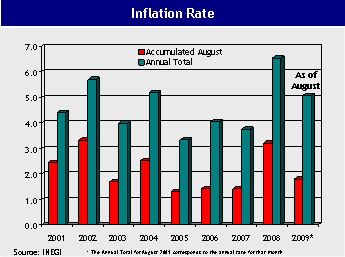

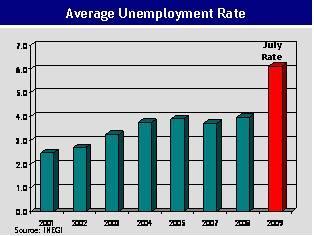

Given the situation, in 2009 we are

likely to observe increased fiscal

deficits, reduced inflation if not

deflation, low rates of economic growth

and increased unemployment throughout

the region. As a lagging

unemployment is likely to be higher at

the end of the year than the current

level. The downturn is also showing

some economic principles at work, such

as the trade-off between inflation and

unemployment and hoe the Phillips

Curve is well at work.

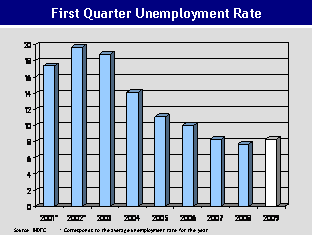

Argentina

Brazil

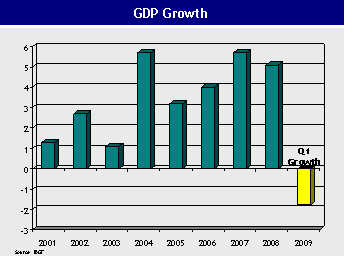

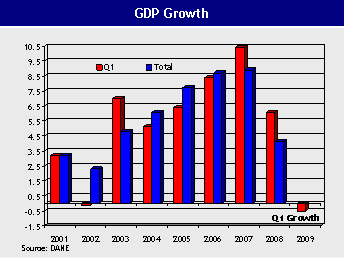

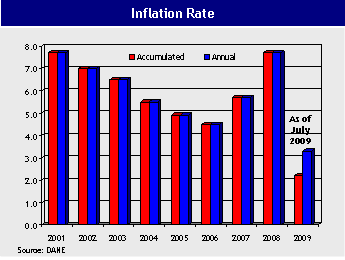

Probably Brazil's economy has been one of the most stable in Latin America over the past

eight years, showing declining

inflation and unemployment rates

and growing every year.

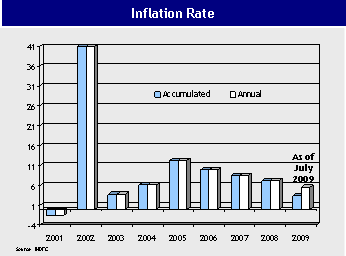

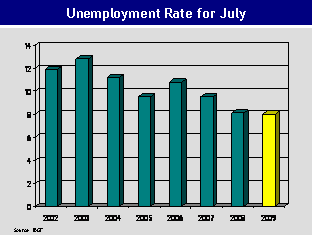

Colombia

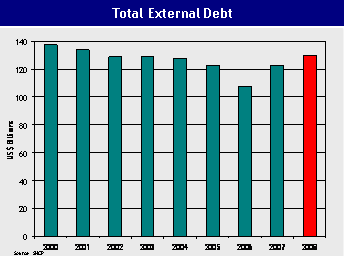

This section shows some general trends of the Colombian economy over the past few years.

"

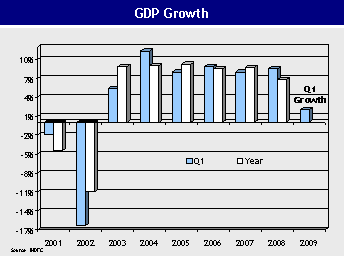

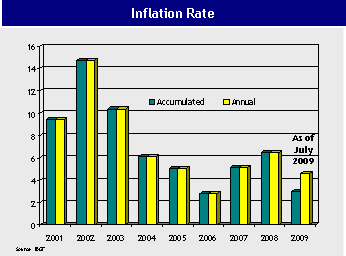

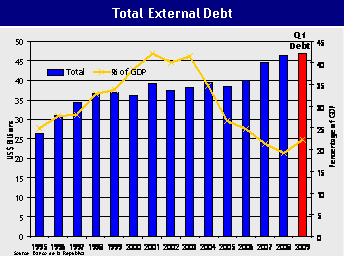

Mexico

In Latin America, Mexico has been the country most affected in terms of economic growth by

the global financial crisis and

recession.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}