Labor Market Dynamics

October 3, 2020

The intertemporal dimension of the labor market implies observing its evolution through time. In other words is the analysis of the labor market with respect to past and future events. It could be compared to the market monthly, in the short-run, within one year or it could be analyzed over longer periods of time across different time spans. The impact of the novel coronavirus (covid-19) on labor has been unprecedented as observed in "The Current Labor Market" article of October 2, 2020.

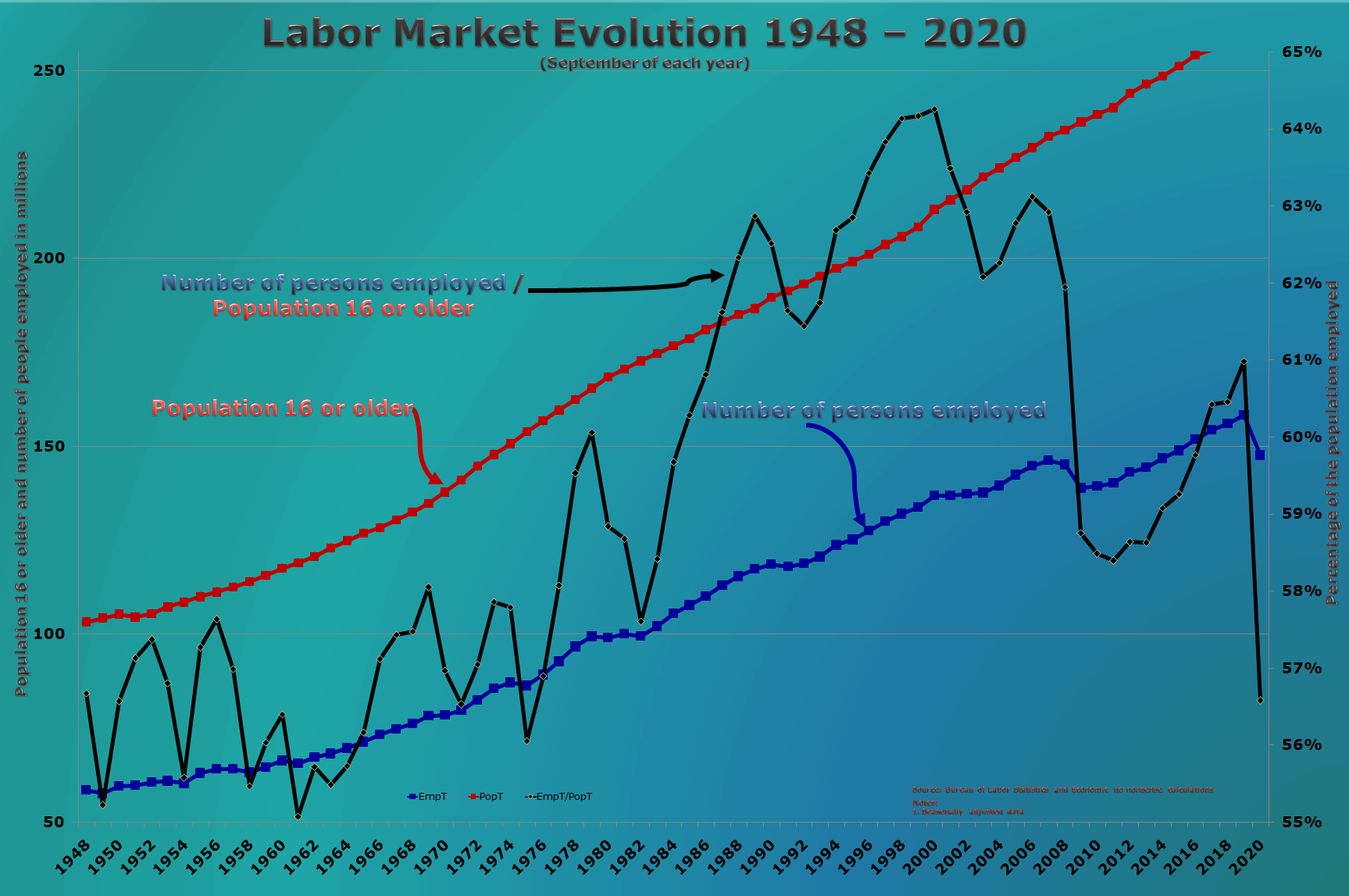

The percentage of the population 16 years old or older employed had an increasing trend until the year 2000 when it reached 64.3%. Since then the trend has been reversing. The 2009-2010 recession was particularly bad for employment (Graph 1) when the percentage declined to 58.5%. The expansionary monetary policy adopted by the Federal Reserve (FED) for at least a decade and other economic policies partially improved the situation helping employment climb to close to 61% in 2019. However, the situation in September of 2020 is even worse than in 2011 as the level employment declined to 56.6% for September and 56.1% on average for the whole of 2020.

Even with the generosity of the FED the labor market has not been able to come back to its best years. The question is whether, once covid-19 is tamed, other policies would help or if the shrinking trend will unavoidably continue.

Table 1 compares the labor statistics between 2019 and 2020 for the month of September on a seasonally adjusted basis. The population under scrutiny, that from which the labor force derives, corresponds to people at least sixteen years old or older. This group increased by 1.3 million people during the year at an annual rate of 0.48%.

| Table 1 | |||||

| Labor Market (Population 16 years or older) | |||||

| September (Numbers in thousands) | |||||

| Indicator | 2019 | 2020 | 2020 - 2019 | 2020 / 2019 | |

| Total Population 16 years or older | 259,574 | 260,819 | 1,245 | 0.48% | |

| Employed | 158,298 | 147,563 | -10,735 | -6.78% | |

| Unemployed | 5,753 | 12,580 | 6,827 | 118.67% | |

| Labor Force = Employed + Unemployed | 164,051 | 160,143 | -3,908 | -2.38% | |

| Not in Labor Force | 95,523 | 100,676 | 5,153 | 5.39% | |

| Unemployment Rate = Unemployed / Labor Force | 3.51% | 7.86% | 4.35% | 124.00% | |

| Number of Jobs Lost | 11,494 | ||||

| Source: Bureau of Labor Statistics, Current Population Survey and Economic no nonsense calculations. | Note 1: Data is seasonnally adjusted by the Bureau of Labor Statistics. | Note 2: Number of Jobs Lost and Population 16 years or older were calculated by Economic no nonsense. | |||

There are several problems observed in Table 1. First, the labor force decreased by 3.9 million people even as the population expanded, meaning that these people have forgone the possibility of obtaining employment on a permanent or temporary basis. Second, despite the large reduction of the labor force, the population unemployed more than doubled reaching almost 7 million. Third, there was a reduction of close to 11 million people employed between September of 2019 and the same month of 2020. Fourth, the two previous problems imply that if the participation rate of the population had remained stable between 2019 and 2020 there currently would be more than 17 million people "implicitly unemployed" in other words, displaced as either unemployed or removed from the labor force. Fifth, these statistics do not address the problem of underemployment, workers that are employed in jobs requiring less "ability" or "intensity" than they are able or willing to handle.

If the current situation is compared to the one observed at this time last year there is a loss of close to 11.5 million jobs. This calculation is conducted by assuming that if the participation and unemployment rates had remained stable while population grew 0.48%, then 159.1 million would be employed instead of the current 147.6 million. The question is whether this is a permanent or a temporary loss of jobs.

In addition to the loss of jobs the labor market situation is exceptionally complex at this juncture as the reason for the large contraction of the labor force is subject to debate. Many people may have "temporarily" left the labor force due to the fear of contracting covid-19 on the job, in other cases the pandemic may have forced them to stay at home to take care of children due to school or daycare closings and there may still be other explanations. The rest of the contraction may be a permanent one reflecting the situation of workers that have completely forgone the possibility of looking for a job due to a diversity of factors. Since the Great Depression U.S. workers had not faced a situation so difficult in terms of displacement, losses and decline.

The continued weakness of labor employment is surely going to have a consequent impact on economic growth. It is almost certain that 2020 third trimester data will show a recovery of economic growth with respect to the second trimester as the economy partially reopened. In fact, the average unemployment rate during the second trimester (April-June) was 13.0% while the one observed in the third trimester (July-September) was 8.8%. Nonetheless, the fourth quarter could see another Gross Domestic Product (GDP) contraction unless the number of people employed rises well above the previous (third trimester) average level of 146.1 million or another significant fiscal stimulus is provided or both. Personal income and consumption must have surely increased during the third trimester but this trend is unsustainable without the preconditions of employment and fiscal stimuli just described.

{kind=link}